Showing posts with label stock indexes. Show all posts

Showing posts with label stock indexes. Show all posts

Friday, February 18, 2011

Friday, November 26, 2010

Tuesday, October 19, 2010

Thursday, August 26, 2010

Monday, August 23, 2010

Economic Fears Weigh on Stocks

I thought that after Friday's bounce off support, we might see a rally, but stocks sagged into the close, ending down again. It's difficult to be optimistic in this environment. Very thin volume.

from WSJ:

NEW YORK—U.S. stocks finished in the red for a third straight day as continuing economic fears weighed on the market, overshadowing excitement over a string of acquisitions.

The Dow Jones Industrial Average finished down 39.21 points, or 0.38%, at 10174.41 after a session that saw the measure gain as many as 91 points. The Nasdaq Composite Index slipped 0.92% to 2159.63 while the Standard &Poor's 500-stock index fell 0.40% to 1067.36...

"We've kind of hit a brick wall here and everything's going sideways," said Daniel Morgan, portfolio manager at Synovus Securities. "Everybody's concerned about deflation."

Investors had little U.S. economic data to go on Monday, though the rest of the week includes key reports on the housing market as well as a revision to second-quarter economic growth. Economists are expecting the government's estimate of 2.4% economic growth for the second quarter to be cut to 1.3% when it is released Friday, which would represent a clear slowdown from earlier in the year.

The latest economic data from the euro zone was less than encouraging. Both the region's manufacturing and services purchasing managers indexes slid in August, despite pickups in Germany and France, suggesting that other countries that are implementing strict fiscal plans to narrow large budget deficits have seen a sharper slowdown in their economies...

Meanwhile, a report from Moody's Investors Service warned that growth throughout the euro zone may fall short of preventing credit-rating agencies from downgrading some member countries if their economies begin to suffer in the face of tight austerity budgets.

The euro fell to $1.2662 while the U.S. Dollar Index, which tracks the U.S. currency against a basket of six others, edged up 0.1%. Treasurys rose, pushing the yield on the 10-year note down to 2.61%, while crude-oil futures tumbled to around $73 a barrel and gold futures were off slightly.

Monday's stock-market movements came on one of the thinnest days for trading volume this year, with just over 3.3 billion shares changing hands in NYSE Composite volume. The only two weaker trading days have come on the two previous Mondays.

Sunday, August 22, 2010

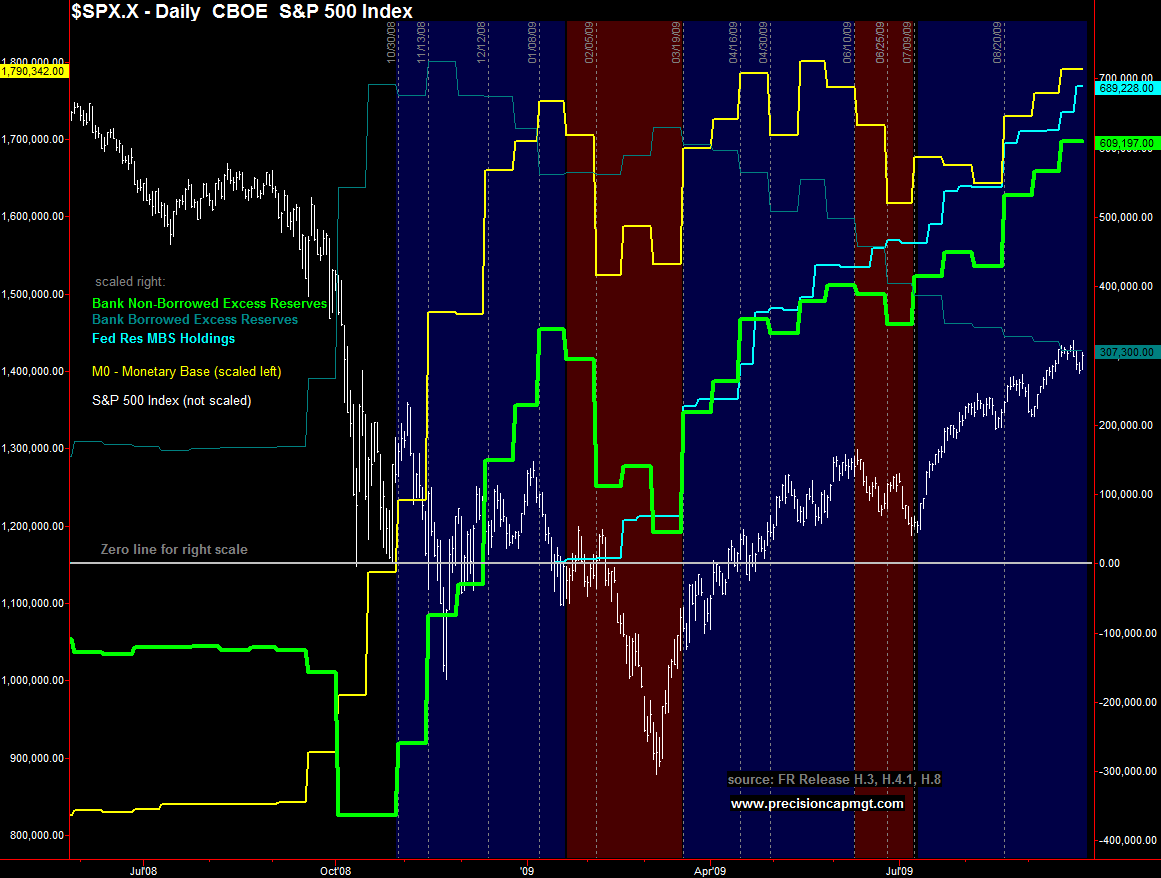

How the Fed Props Up the Stock Market Through Permanent Open Market Operations

The Financial Times recently reported on the Fed’s latest exit strategy to eventually contain the inflation zombie:

During the crisis, the Fed created roughly $800bn of additional bank reserves to finance asset purchases and loans. This total is likely to rise in the coming months as the central bank completes its asset purchases and the Treasury unwinds financing it provided to the Fed. Fed officials think they could raise interest rates even with this excess supply of reserves by offering to pay banks to deposit their surplus funds with it rather than lend them out. However, they also want to use reverse repos in tandem to soak up some of the excess reserves. Policymakers call this a “belt and braces approach”. [The latter, clearly a nod to the great Gekko.]

Tyler Durden touched on this last Thursday, and we will expand upon it here as it is particularly relevant to our ongoing theory that it is the proceeds from permanent open market operations (POMOs) and their close cousins that are driving equities. Though this may be received wisdom to Zero Hedge readers, the Fed has done us the favor of providing additional evidence through the FT story. A bit of background, as we are new contributors to this forum:

Tyler Durden touched on this last Thursday, and we will expand upon it here as it is particularly relevant to our ongoing theory that it is the proceeds from permanent open market operations (POMOs) and their close cousins that are driving equities. Though this may be received wisdom to Zero Hedge readers, the Fed has done us the favor of providing additional evidence through the FT story. A bit of background, as we are new contributors to this forum:Money Supply: Based on our previous research on the effects of swings in M2 non-seasonally adjusted money supply (M2) on the stock market, we were a bit surprised in July 09 by the resiliency of the rally, which continued in the face of such a dramatic contraction in M2. The dismal Durable Goods report from last Friday confirms that the capital goods sector is still under significant pressure as a result of a lack of money in the general economy. With banks not lending to normal businesses and consumer credit contracting equally as violently, what is the basis for this rally and from where does the never-ending flow of equities juice flow?

Bank Non-Borrowed Excess Reserves: The Fed statistic that most closely correlates with the 2009 equities run-up appears to be bank non-borrowed excess reserves (bank NBER), which is a component of the monetary base (M0). As explained by the Fed, bank NBER is simply total bank excess reserves minus bank borrowed excess reserves (bank BER). This resulted in bank NBER going negative throughout much of 2008 because banks acquired most of their excess reserves through participation in Fed lending programs. As the Fed has wound down these programs in 2009, bank BER has steadily declined and has been a drag on M0. Concurrently, though, bank NBER has advanced since late March 09 with only one brief material pause in June, and reflects those excess reserves that need not be repaid as part of any Fed lending program. The Fed purchases of MBS, Agency and Treasury securities netted $990 trillion since March 09. The distinction between borrowed and non-borrowed excess reserves is critical because the latter would be ideally suited for leveraging and lending out to hedge funds and the like to “invest” in the high beta stocks that have led the rally.

The primary conclusion is simple - the stock juice flows from steadily increasing Bank NBER, which is hidden to even astute observers that focus on only M0 or M2. Though we previously found no historical correlation between M0 (or its constituent components) and the stock market, we have witnessed an historically unprecedented set of circumstances. Now that the Fed has become the world’s largest hedge fund, we are prepared to accept unorthodox conclusions.

So why not inflate both equities and the general economy simultaneously? It was most likely a race against time. The administration and Fed needed to replace the incredible evaporation of wealth that occurred in late 2008/early 2009 to quell the voting and investing masses. They could not reflate the entire economy this quickly without jeopardizing their ability to borrow cheaply and restart the housing bubble. To keep long term yields low, they reflated the stock market only, with the hope that the general economy would eventually catch up in 2010 and be able to sustain the stock market gains. The problem with rising yields has not been solved, but was postponed.

As we noted in previous research, we are toward the end of a seasonal drain on M2. Once over the October hump, it should be easier for the holiday season to carry the market into March 2010, especially with the help of another $834 billion in MBS and Agency POMO into next March (not to mention the possible Treasury SFP wind-down effect to the tune of $114 to 185 billion). The Fed must be perfect, however, as any new panic will quickly feed on itself and likely lead to another mass exodus from equities. This is quite simply because currently, there is absolutely nothing else to back up this rally in the general economy if the Fed funny money cannot do its trick.

Back to Money Market Funds: If bank NBER is materially tied up in equities, then the Fed cannot drain from this source to mitigate inflation, or it risks the resulting cascade of sell orders that accompany the typical panic. According to the FT article:

The obvious counterparties for reverse repo deals are the Wall Street primary dealers. However, the Fed thinks they would only have balance sheet capacity to refinance about $100bn of assets. By contrast, the money-market funds have $2,500bn in assets, which means they could plausibly refinance as much as $500bn in Fed assets. Officials think there would be appetite on the part of the funds, which are under pressure [at gunpoint] from regulators and investors to stick to low-risk liquid investments.The Fed Helps Build Our Case: As of September 17 09, bank NBER had increased by $563 billion since the March 09 rally began. With M2 net flat during this period, the $563 billion has not made its way into the general economy by any stretch. Perhaps it is sitting idle; however, the Fed says only $100 billion would be available from primary dealers in the future? As the vast bulk of bank NBER is concentrated in primary dealers, this begs the obvious question of what will be tying up the remaining $463 billion (and we are not including the expected increases in bank NBER into next March, which could double this amount)? Given a conservative lending leverage ratio of 10 to 1, there is potentially $4.63 trillion already sloshing around. Even if we are much more conservative, given the roughly $2 trillion increase in the US stock market since Mar 09, it is not only easily conceivable, but probable, that a substantial portion was courtesy of the Fed ATM machine.

As Gekko closed his famous speech in Wall Street, “Greed – you mark my words – will save Teldar, and that other malfunctioning corporation, the U.S.A.” While we have focused here only on coercive greed, it will be interesting nonetheless to see how this works out.

Thursday, August 19, 2010

Saturday, August 14, 2010

WSJ Asks "Is a Crash Coming?"

by Brett Arends at WSJ:

Could Wall Street be about to crash again?

This week's bone-rattlers may be making you wonder.

I don't make predictions. That's a sucker's game. And I'm certainly not doing so now.

But way too many people are way too complacent this summer. Here are 10 reasons to watch out.

1. The market is already expensive. Stocks are about 20 times cyclically-adjusted earnings, according to data compiled by Yale University economics professor Robert Shiller. That's well above average, which, historically, has been about 16. This ratio has been a powerful predictor of long-term returns. Valuation is by far the most important issue for investors. If you're getting paid well to take risks, they may make sense. But what if you're not?

2. The Fed is getting nervous. This week it warned that the economy had weakened, and it unveiled its latest weapon in the war against deflation: using the proceeds from the sale of mortgages to buy Treasury bonds. That should drive down long-term interest rates. Great news for mortgage borrowers. But hardly something one wants to hear when the Dow Jones Industrial Average is already north of 10000.

3. Too many people are too bullish. Active money managers are expecting the market to go higher, according to the latest survey by the National Association of Active Investment Managers. So are financial advisers, reports the weekly survey by Investors Intelligence. And that's reason to be cautious. The time to buy is when everyone else is gloomy. The reverse may also be true.

4. Deflation is already here. Consumer prices have fallen for three months in a row. And, most ominously, it's affecting wages too. The Bureau of Labor Statistics reports that, last quarter, workers earned 0.7% less in real terms per hour than they did a year ago. No wonder the Fed is worried. In deflation, wages, company revenues, and the value of your home and your investments may shrink in dollar terms. But your debts stay the same size. That makes deflation a vicious trap, especially if people owe way too much money.

5. People still owe way too much money. Households, corporations, states, local governments and, of course, Uncle Sam. It's the debt, stupid. According to the Federal Reserve, total U.S. debt—even excluding the financial sector—is basically twice what it was 10 years ago: $35 trillion compared to $18 trillion. Households have barely made a dent in their debt burden; it's fallen a mere 3% from last year's all-time peak, leaving it twice the level of a decade ago.

6. The jobs picture is much worse than they're telling you. Forget the "official" unemployment rate of 9.5%. Alternative measures? Try this: Just 61% of the adult population, age 20 or over, has any kind of job right now. That's the lowest since the early 1980s—when many women stayed at home through choice, driving the numbers down. Among men today, it's 66.9%. Back in the '50s, incidentally, that figure was around 85%, though allowances should be made for the higher number of elderly people alive today. And many of those still working right now can only find part-time work, so just 59% of men age 20 or over currently have a full-time job. This is bullish?

(Today's bonus question: If a laid-off contractor with two kids, a mortgage and a car loan is working three night shifts a week at his local gas station, how many iPads can he buy for Christmas?)

7. Housing remains a disaster. Foreclosures rose again last month. Banks took over another 93,000 homes in July, says foreclosure specialist RealtyTrac. That's a rise of 9% from June and just shy of May's record. We're heading for 1 million foreclosures this year, RealtyTrac says. And naturally the ripple effects hurt all those homeowners not in foreclosure, by driving down prices. See deflation (No. 4) above.

8. Labor Day is approaching. Ouch. It always seems to be in September-October when the wheels come off Wall Street. Think 2008. Think 1987. Think 1929. Statistically, there actually is a "September effect." The market, on average, has done worse in that month than any other. No one really knows why. Some have even blamed the psychological effect of shortening days. But it becomes self-reinforcing: People fear it, so they sell.

9. We're looking at gridlock in Washington. Election season has already begun. And the Democrats are expected to lose seats in both houses in November. (Betting at InTrade, a bookmaker in Dublin, Ireland, gives the GOP a 62% chance of taking control of the House.) As our political dialogue seems to have collapsed beyond all possible hope of repair, let's not hope for any "bipartisan" agreements on anything of substance. Do you think this is a good thing? As Davis Rosenberg at investment firm Gluskin Sheff pointed out this week, gridlock is only a good thing for investors "when nothing needs fixing." Today, he notes, we need strong leadership. Not gonna happen.

10. All sorts of other indicators are flashing amber. The Institute for Supply Management's manufacturing index, while still positive, weakened again in July. So did ISM's new-orders indicator. The trade deficit has widened, and second-quarter GDP growth was much lower than first thought. ECRI's Weekly Leading Index has been flashing warning lights for weeks (though the most recent signals have looked somewhat better). Europe's industrial production in June turned out considerably worse than expected. Even China's steamroller economy is slowing down. Tech bellwether Cisco Systems has signaled caution ahead. Individually, each of these might mean little. Collectively, they make me wonder. In this environment, I might be happy to buy shares if they were cheap. But not so much if they're expensive. See No. 1 above.

Wednesday, August 11, 2010

Tuesday, August 10, 2010

Choppy Pre-Fed Announcement Trading, Stocks Down

Friday, August 6, 2010

Thursday, August 5, 2010

Jobless Claims Send Stocks Into Freefall

AP excerpt:

In a reminder of how weak the job market is, the government said Thursday that first-time claims for unemployment benefits rose last week to their highest level in four months.

Claims rose by 19,000 to a seasonally adjusted 479,000. Analysts had expected a small drop. Claims have now risen twice in the past three weeks.

Economists closely watch initial jobless claims because they are considered a gauge of the pace of layoffs and an indication of employers' willingness to hire. And even at a time when profits are coming back, businesses aren't very willing.

Pierre Ellis, an economist at Decision Economics, wrote in a note to clients that an "unyielding flow of layoffs" suggests employers are still not comfortable with the size of their staffs.

And with the job market still looking shaky, Americans are in no mood to spend freely.

Monday, August 2, 2010

Rally Time!

NEW YORK (AP) - The stock market began August with a huge rally after economic and earnings reports from around the world revived investors' faith in the global recovery. The Dow Jones industrial average jumped 163 points in afternoon trading. Major stock indexes all rose more than 1 percent.

The market rallied at the opening bell on upbeat economic news from China and earnings reports from European banks. Then, shortly after trading began, investors got a surprisingly good report on U.S. manufacturing. The Institute for Supply Management said its manufacturing index slipped to 55.5 in July from 56.2 a month earlier.

The results showed a modest slowdown in growth, but traders were pleased because the index came in higher than the 54.1 forecast by economists polled by Thomson Reuters. And any reading above 50 indicates expansion.

The market was encouraged by several key components of the index. Production and new orders both improved, as did companies' willingness to hire new employees.

"Every component in ISM was greater than 50," said Cort Gwon, director of trading strategies and research at FBN Securities. "To have all of them up is a good sign."

Stock trading has been erratic for months because of signs the recovery was weakening. Strong earnings in July helped drive stocks to their best month in a year, but the rally was fading at the end of the month on new worries about the economy. The ISM report is significant because it is the first major reading of the economy from July and investors are trying to determine just how strong the recovery will be in the second half of the year.

Thursday, July 29, 2010

Stocks Plunge from Grace

Tuesday, July 27, 2010

All the Volume Is On the Sell Side

In our day and age, when implied correlation is approaching 1 with each passing day, and when nuanced relationships are ignored, as every correlation somehow immediately becomes causation only to be invalidated, chewed out and left for dead, there is one certain and virtually guaranteed statistical relationship left, that not only persists day after day but has now become its own self-fulfilling prophecy. We speak of course of the (inverse) correlation between stock prices and volume: i.e., "volume up, stocks down; volume down, stocks up." Rinse, repeat, over and over and over. Rarely has this correlation been as pronounced (although we have been discussing it for well over a year) as over the past 12 weeks. Behold.

What this means is that any distributions only occur to the downside, and that the second retail gets suckered into stocks once again, for whatever reason, the selling pressure will again materialize as the algo decides to take advantage of the "sidelined" money and be a better seller into every bid.

Thursday, July 22, 2010

Stocks: BUY!

Wednesday, July 21, 2010

Stocks: SELL!

Subscribe to:

Posts (Atom)