Friday, December 21, 2012

Our Destructive Interconnectedness

Washington Turmoil Sends Stocks Off a Fiscal Cliff

Last night, when Speaker Boehner was unable to find enough votes to pass a tax bill, stocks had another flash crash and the S&P 500 index dropped 50 points for a few minutes. Some relatively benign news this morning on consumer spending and income has given stocks some buoyancy, but the Dow is still down about 150 points.

Wednesday, December 19, 2012

Economic Ennui -- and It's Only Going to Get Worse!

by Brandon Smith at Alt-Market.com

The markets, as most people reading this should now well know, no

longer reflect in any way the true economic health of our country. If

one was to measure the financial “recovery” of this nation by the

strength of global stocks alone, he would probably come to the

conclusion that the collapse of 2008 was a mere hiccup in the overall

success of the worldwide economic system. However, electronically

traded equities with little more to back their value than scraps of

receipt paper and numbers on a screen have no bearing on what is going

to happen to you, and to me, over the course of the coming year. The

stock market is a sideshow, a popcorn movie, a façade. The real drama

is going on behind the scenes and revealed in fundamentals that

mainstream analysts no longer discuss…

The only advantage of a

long drawn disintegration of the overall system is that as the years

pass, it becomes possible to discover a pattern through which we can

gauge where we really stand today and will stand tomorrow, giving us a

chance (a narrow chance) to limit the eventual damage. Unfortunately,

the pattern now in motion suggests that the next year will be exactly

what we have been predicting over the past several months: Dismal.

The

MSM refuses to discuss it at great length, but all signs show an epic

global slowdown in demand and production, especially in the final

quarter of 2012. This slowdown cannot be denied, nor can it be shrugged

off as inconsequential. This development is exactly as I predicted in

January of this year using the Baltic Dry Index as a guide. During that

first quarter, the BDI fell to record lows, indicating an extreme

decline in shipping demand around the world, which, in turn, indicated a

fall in demand for raw goods, which, in turn, indicated a fall in

demand for consumer goods. Mainstream pundits sought to distract the

public from this fact by claiming that the BDI was collapsing due to an

“oversupply of ships”, not rescinding demand. This disinformation was

proven incorrect in the beginning of the third quarter of this year,

when export nations from China, to Japan, to Germany all began reporting

abysmal manufacturing numbers and steep faltering in overseas

purchases.

Of course, we all know what happened next: The

markets began to tank when they caught the scent of a slowdown, losing a

thousand points within the span of a week. Not so unpredictably (since

I also predicted it at the beginning of the year) the Federal Reserve

leapt into action with its announcement of QE3 (QE Infinity).

QE3

has done little to change the problem of falling global demand, but it

has certainly defibrillated stocks. In fact, I think it is safe to say

that a majority of QE fiat funds are flowing (directly or indirectly)

into the DOW, and not much else. International trade and consumption is

starting to feel the pain, and respective countries are no longer able

to hide it. Keep in mind that this slowdown is occurring right at the

height of the Christmas season, when consumption is usually supposed to

reignite.

Despite the sugar coated claims of insane Keynesians

who only a few years ago were predicting a “resurgence” of American

industry and exports due to the Federal Reserve’s ongoing devaluation of

the dollar, production in the U.S. has remained pathetically weak, and

continues to decline:

http://www.nytimes.com/2012/12/12/business/economy/decline-in-exports-hurts-us-trade-deficit.html

This

is of course a direct result of slowing global demand, reducing

potential markets all over the world, which is something deflation fear

mongers apparently didn’t see coming. The reality is that demand is

faltering EVERYWHERE, not just in the U.S., and this begs a particular

question: In an interdependent economic system driven primarily by

consumption, who is going to fill the void when all nations are dry of

spending cash? That is to say, who is going to take up the slack, when

obviously no one has the wealth to do so? Without a cultural cash

engine, the globalized framework is destined to fail.

China’s

export growth fell far more than expected in November, something which

many Chinese economists are attributing to a complete lack of revival in

American markets:

http://www.reuters.com/article/2012/12/10/us-china-economy-idUSBRE8B80FL20121210

Manufacturing

in the UK went into steep decline almost simultaneously, showing that

sinking demand is striking both the Pacific and the Atlantic:

http://www.bloomberg.com/news/2012-12-07/u-k-manufacturing-drops-more-than-forecast-on-food-alcohol-1-.html

Germany,

the largest economy in the EU and the only country still holding the

absurd political entity together, has been shocked to discover that its

own Bundesbank is forecasting a contraction in growth to near zero in

2013:

http://www.actionforex.com/analysis/daily-forex-fundamentals/germany%27s-bundesbank-revise-lower-2013-outlook-20121207180090/

Japan’s

economy suffered an annualized decline in GDP in November greater than

that which occurred during the Fukushima disaster:

http://www.bloomberg.com/news/2012-11-11/japan-s-economy-shrinks-at-fastest-pace-since-earthquake.html

This

contraction has recently caused Japan to install a new revamped

government during elections this month, which unfortunately will be

instituting almost identical policies to the last regime.

Finally,

Brazil, a developing export nation with very important significance as a

litmus test for world consumption, posted near zero growth in the third

quarter of 2012, far below expectations but in line with the bigger

picture. The global financial machine is grinding to a halt right under

our very noses…

http://www.reuters.com/article/2012/11/30/us-brazil-economy-gdp-idUSBRE8AT0KM20121130

At

the end of 2012, it is undeniable; the system is running out of steam,

and not even constant fiat injections by central banks are reversing our

current course.

In order to understand what is happening, I

want you to imagine a quickly diminishing cycle. Imagine that in 2008,

America was on the edge of a whirlpool, or a spinning vortex, and was

suddenly caught in the outermost current. Today, we have circled the

epicenter several times, each rotation becoming smaller and more

volatile than the last. Eventually, the whirlpool will reach an end,

and our economy will be sucked into the destructive funnel. One can see

clear evidence of this decline in the Baltic Dry Index:

Notice

how each year since 2008 there is a spike in shipping rates indicating a

rise in demand for materials at the onset of the Christmas season,

which is the natural progression of things. Yet, also notice that this

spike in demand grows smaller with each passing year. In 2012, the

increase has been almost nonexistent, meaning that we are likely very

close to going down the drain.

Some pundits may argue that

November’s Black Friday sales were tremendous, and this signals a

recovery in spending and consumption. I would point out that such

numbers are deceiving. High sales during the most discounted day of the

Christmas buying season is not necessarily a good thing. What it

really reveals is that a majority of shoppers were looking for the

lowest prices possible because of a lack of personal savings. It is a

sign of desperation, not revitalization. Full season numbers have not

yet been released, but when they are, I believe we will see a fantastic

spike in sales on Black Friday followed by a complete flatline for the

rest of the year. Obviously high consumption has not been sustained,

otherwise, worldwide manufacturing and shipping would be in much better

shape.

The issue here is one of priorities. With multiplying

distractions going on around the globe, including the fear of recent

mass murders at home, will the public be able to keep track of the

deadly financial tidal waves just off the coast, or will they even care

when distracted by so many sharks in the water? The next two months

will be very revealing. The so-called “fiscal cliff” is on the way, and

the question of whether or not the U.S. government should kick the can

down the road or take the sour medicine it needs and move on has arisen

once again. This debate is and always has been an illusion. Whether we

continue to increase government spending, taxation, and inflation, or

we cut all spending and shut down the fiat presses, there is still going

to be a collapse.

However, the “fiscal cliff” could be very dangerous in an entirely different respect…

The

coming collapse will not be due to the indecision or partisan bickering

of our politicians. They are in much closer agreement than the MSM

would like to admit. Instead, the monolithic Catch-22 of our age will

be the direct result of the actions of the private Federal Reserve and

the peripheral international banking cartel; the engineers who gave

birth to the toxic derivatives implosion in the first place. What I

fear most is that the results of the fiscal cliff negotiation along with

other triggers around the planet (Syria, Iran, the EU breakdown, etc.)

will be used to veil the true weaknesses of our already imploding

system, and eventually be exploited as scapegoat events for a disaster

that has been in the making for decades, not just a few years. The

omens are not good for 2013, and we can only circle the drain for so

long…

Tuesday, December 18, 2012

Risk Is Being Ignored, Amplified

Our biggest concern here on the cusp of 2013 is the current odd combination of extreme complacency about the risks presented by extend-and-pretend macro policy making and rapidly accelerating social tensions that could threaten political and eventually financial market stability. Before everyone labels us ‘doomers’ and pessimists, let us point out that, economically, we already have wartime financial conditions: the debt burden and fiscal deficits of the western world are at levels not seen since the end of World War II. We may not be fighting in the trenches, but we may soon be fighting in the streets. To continue with the current extend-and-pretend policies is to continue to disenfranchise wide swaths of our population - particularly the young - those who will be taking care of us as we are entering our doddering old age. We would not blame them if they felt a bit less than generous. The macro economy has no ammunition left for improving sentiment. We are all reduced to praying for a better day tomorrow, as we realise that the current macro policies are like pushing on a string because there is no true price discovery in the market anymore. We have all been reduced to a bunch of central bank watchers, only ever looking for the next liquidity fix, like some kind of horde of heroin addicts. We have a pro forma capitalism with de facto market totalitarianism. Can we have our free markets back please?

Potential Implications of Our Debt

In today's Outside the Box I bring you two pieces that, at first

glance, may not seem to have much to do with each other. First, Bill

Gross, PIMCO managing director, runs down the fierce structural

headwinds that our hard-pedaling global economy faces over the next

decade. I am going to deal at length with not only his GDP projections

for the rest of the decade but those of Grantham and others in the last

two Thoughts from the Frontline of this year. This is a

challenging environment for traditional portfolio construction, but it’s

par for the course as we slog through the secular bear market I was

first writing about in 1999.

Then Charles Gave instructs us on the distortions in the

measurement of risk that have been introduced as the "plain, boring and

well-meaning economists working in the entrails of the world central

banks" have supplanted the Marxist avant garde in the world's shift

away from “scientific socialism” to "scientific capitalism."

However, when you think about it, these pieces dovetail in a

very convincing – and somewhat frightening – manner. Because what they

add up to – if the econocrats are yanking the rug out from under a

capitalist system that is already reeling, as Gross says, from debt and

deleveraging, a slowing of the locomotive of globalization,

and dislocations in technology and demographics – is a profound, ongoing

challenge to you and me as investors. Gross and Gave have their own

ideas about how we get through this. I don’t agree with all their

conclusions – this letter is not called Outside the Box for

nothing – but I offer these essays because they’ll make us think through

our own presuppositions. However you view their analysis, they do

reinforce the idea that we're all going to have to be not only careful

but very nimble.

I post this note from 35,000, feet flying back from Cleveland to

Dallas. American Airlines has now put internet on nearly all of their

domestic flights, and I find the time I spend read and respond without

interruption up here some of the more productive time I get. Which is

good, since the record shows that I have been on some 110-plus different

planes this year, most of which were AA. (Lately, when I am asked where

I live, I just say my closet is in Dallas.)

It is not just me but other “road warriors” who have noticed

that the staff of AA have markedly stepped up their personal service

levels (as opposed to United, when they were in similar financial

difficulties). More than a few of their employees have gone far out of

their way to make my difficult travel schedule a little bit easier and

smoother, from frontline staff to their back-office phone mavens, who

often perform a little bit of magic rearranging my schedule. And as they

add newer planes to their fleet, seat 5B has almost become my home

office. So here’s a tip of the hat to them and all the service people

who make life on the road better. And may your own road be a little

smoother these holidays.

I spent last night at Dr. Mike Roizen’s home before seeing a few

doctors at the Cleveland Clinic. I rode in a limo with him to a speech

in Youngstown, Ohio, and we had time to visit at length. Mike has become

one of my dearest friends, and our times together are easy ones, deeply

treasured. Without this peripatetic life I would not have so many good

friends, far and wide. It is the best perk of traveling.

Mike is on the board of the Cleveland Clinic, and he is deeply

worried about the fiscal cliff. Even assuming the “doc fix” is passed,

as it always is, without an alteration or repeal of the current law, the

Cleveland Clinic will be faced with an almost 9% budget cut on January

1. They will lose money on every Medicare and Medicaid patient they see.

There are no good solutions other than deep budgets cuts. And since the

largest portion of their budget is salaries?...

The CC is held up (rightly so) as one of the most efficient

medical organizations in the world. They have no fat to cut. I met the

lady, in my walking around at the clinic, who cut $24 million in energy

costs and another $2 million in trash-removal costs, at some

considerable effort and investment. They leave no dollar stone unturned

in the pursuit of efficiency.

Mike and I talked deep into the night and much of the next day,

when we could, about our healthcare system. It fills me with deep

concern. I have asked Mike to give us an outline of his speech today for

an Outside the Box. His five-step “solution” has lowered

healthcare costs for the 43,000 CC staff and all firms that have adopted

their plan. When you look at his numbers, you understand why the US

spends more money on healthcare than Europe. We are indeed that much

less healthy. The CC has found out that paying each staff member $2,000

to adopt a healthier lifestyle lowers overall costs by even more than

that.

Smoking cigarettes may be your personal choice and God-given

right, but it costs the American healthcare system and taxpayers

multiple tens of billions. And the same goes for four other lifestyle

habits. Want to live long and prosper? And be smarter and have better

sex? Just eat right, exercise and avoid a few items. I hope Mike gets me

that essay soon, as I want all my closest friends (that would be you!)

to stay around with me for a long, long time.

Have a good week. I am looking forward to the holidays and home

and family. And while I try to get exercise on the road, my home gym is

still the best.

Your ready for a few good nights’ sleep in my own bed analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

Strawberry Fields – Forever?

Bill Gross, Managing Director, PIMCO

Living is easy with eyes closed

Misunderstanding all you see

I think I know I mean a yes

But it’s all wrong

That is I think I disagree

Misunderstanding all you see

I think I know I mean a yes

But it’s all wrong

That is I think I disagree

Strawberry Fields Forever

The Beatles

You didn’t build that............... 332I built that ................................... 206

Well, I guess that settles it: you didn’t build that after all. Or maybe you did, but not all of it. Or maybe like the convoluted John Lennon above “you think you know a yes, but it’s all wrong. That is you think you disagree.” Whatever. Rather than an economic mandate, November’s election was more of social commentary on the Republicans’ habit of living with eyes closed. Their positions on what Conan O’Brien labeled “female body parts” – immigration, gay rights and student loans – proved to be big losers, and they will have to amend rather than defend those views if they expect to compete in 2016. I suspect they will. Political parties are living social organisms that mutate in order to survive. We will see straight talking Chris Christie or Hispanic flavored Marco Rubio leading the Republican charge four years from now versus a reenergized Hillary Clinton. It should be quite a show with a “No C ountry for Old (White) Men” caste to it.

But whoever succeeds President Obama, the next four years will likely face structural economic headwinds that will frustrate the American public. “Happy days are here again” was the refrain of FDR in the Depression, but the theme song from 2012 and beyond may more closely resemble Strawberry Fields Forever, as Lennon laments “It’s getting hard to be someone but it all works out.” Why is it so hard to be someone these days, to pay for college, get a good-paying job and retire comfortably? That really was the economic question of the 2012 election towards which very few specifics were applied from either side. “There’s a better life out there for us,” Governor Romney bellowed to a crowd of thousands in

Des Moines, Iowa just days before the election, but in truth he never told us how we were going to achieve it or, importantly, why we weren’t realizing it in the first place. The president’s political mantra of “Forward” was even more vague.

Their words were mum if only because the real cause of slower economic growth lies hidden in a number of structural as opposed to cyclical headwinds that may be hard to reverse. While there are growth potions that undoubtedly can reduce the fever, there may be no miracle policy drugs this time around to provide the inevitable cures of prior decades. These structural headwinds cannot just be wished away as we move “forward” whether it be to the right, the left or dead center. Last month in a major policy speech at the New York Economic Club, Fed Chairman Ben Bernanke concurred that the U.S. economy’s growth potential had been reduced “at least for a time.” He in effect confirmed PIMCO’s New Normal which has been in place for three years now, laying the blame in part on the financial crisis, diminished productivity gains, and investment uncertainty due to the near-term fiscal cliff. We do not disagree. However, there are numerous oth er structural headwinds that may reduce real growth even below the New Normal 2% rate that Bernanke has just confirmed, not only in the U.S. but in developed economies everywhere.

They are:

1) Debt/Delevering

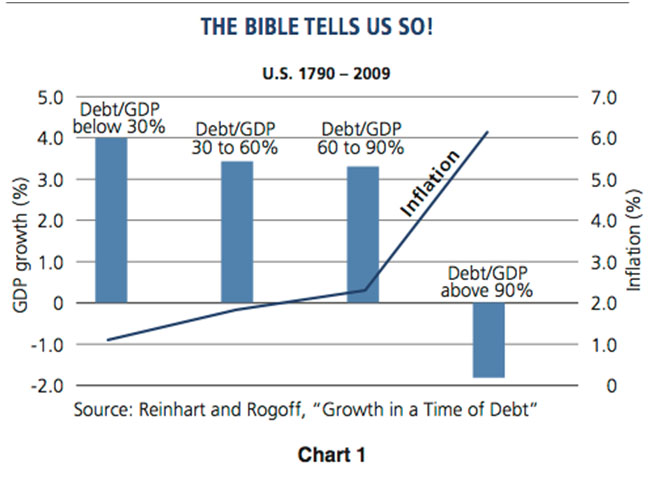

Developed global economies have too much debt – pure and simple – and as we attempt to resolve the dilemma, the resultant austerity should lower real growth for years to come. There are those that believe in the “Brylcreem” approach to budget balancing – “a little dab‘ll do ya.” Just knock a few percentage points off the deficit/GDP ratio, they claim, and the private sector will miraculously reappear to fill the gap. No such luck after 2–3 years of austerity in Euroland, however. Most of those countries are mired in recession and/ or depression. Political leaders there should have studied the historical evidence presented by Carmen Reinhart and Ken Rogoff in a critically important paper titled, “Growth in a Time of Debt.” They conclude that for the past 200 years, once a country exceeded a 90% debt/GDP ratio, economic growth slowed by nearly 2% for both developed and developing nations for an average d uration of nearly a decade. Their work displayed below in Chart 1 shows the result in the United States from 1790–2009. The average annual U.S. GDP rate growth, while clearly influenced by the Great Depression, was -1.8% once the 90% barrier was exceeded. The U.S., by the way, is now at a 100% debt/GDP ratio on the basis of the authors’ standard measuring yardstick. (Note as well the 5_% average inflation rate during the same periods.)

In addition to sovereign debt levels which were the primary focus of the Reinhart/Rogoff studies, it is clear that financial institutions and households face similar growth headwinds. The former needs to raise equity via retained earnings and the latter to increase savings in order to stabilize family balance sheets. The combined need to increase our “net national savings rate” highlighted in last month’s Investment Outlook is a long-term solution to the debt crisis, but a near/ intermediate-term growth inhibitor. The biblical metaphor of seven years of fat leading to seven years of lean may be quite apropos in the current case with the observation that the developed world’s growth binge has been decades in the making. We may need at least a decade for the healing.

2) Globalization

Globalization has been an historical growth stimulant, but if it slows, then the caffeine may wear off. The fall of the Iron Curtain in the late 1980s and the emergence of capitalistic China at nearly the same time was a locomotive of significant proportions. Adding two billion consumers to the menu made for a prosperous restaurant, increasing profits and growth in developed economies despite the negative internal effects on employment and wages. Now, however, these tailwinds are diminishing, producing an airspeed which inexorably slows relative to the standards of prior decades. Is it any wonder that markets now move up or down as much on the basis of policy changes coming out of China as opposed to the U.S. or Euroland? If China and the accompanying benefits of globalization slow, so too may developed economy growth rates.

3) Technology

Technology has been a boon to productivity and therefore real economic growth, but it has its shady side. In the past decade, machines and robotics have rather silently replaced humans, as the U.S. and other advanced economies have sought to counter the influence of cheap Asian labor. Almost a century ago, Keynes alerted the economic community to a “new disease,” what he called “technological unemployment” where jobs couldn’t be replaced as fast as they were being destroyed by automation. Recently, Erik Brynjolfsson and Andrew McAfee at MIT have affirmed that workers are losing the race against the machine. Accountants, machinists, medical technicians, even software writers that write the software for “machines” are being displaced without upscaled replacement jobs. Retrain, rehire into higher paying and value-added jobs? That may be the political myth of the modern era. There aren’t enough of those jobs. A structurally higher unemployment rate of 7% or more is the feared “whisper” number in Fed circles. Technology may be leading to slower, not faster economic growth despite its productive benefits.

4) Demographics

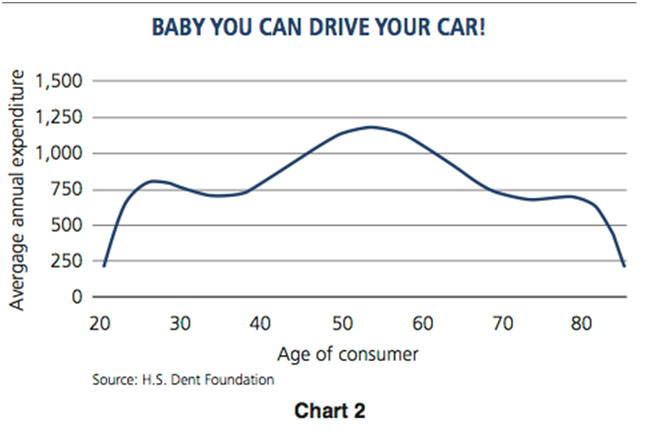

Demography is destiny, and like cancer, demographic population changes are becoming a silent growth killer. Numerous studies and common sense logic point to the inevitable conclusion that when an economic society exceeds a certain average “age” then demand slows. Typically the dynamic cohort of an economy is its 20 to 55-year-old age group. They are the ones who form households, have families and gain increasing experience and knowhow in their jobs. Now, however, almost all developed economies, including the U.S., are gradually aging and witnessing a larger and larger percentage of their adult population move past the critical 55-year-old mark. This means several things for economic growth: First of all from the supply side, it means productivity and employment growth rates will slow. From the demand side, it suggests a greater emphasis on savings and reduced consumption. Those approaching their seventh decade need fewer cars and new homes as shown in Cha rt 2. Almost none of them have babies (thank goodness!). Such low birth rates and a significant reduction in demand have imperiled Japan for several lost decades now. A similar experience will likely turn many developed economy “boomers” into “busters” within the next several years.

Investment Conclusions

I’m fond of reminding PIMCO’s Investment Committee that you can’t buy GDP futures – at least not yet. Hypotheses about real growth rates, no matter how accurate, must be translated into investment decisions in order to justify the discussion. Before doing so, let me acknowledge that these structural headwinds can and will likely be somewhat countered by positive thrusts. Cheaper natural gas and the possibility of reversing or even containing the 40-year upward trend of energy costs may be a boon to productivity and therefore growth. There is talk of the U.S. being energy independent within a decade’s time. Housing as well may be experiencing a multiyear revival. In addition, unforeseen productivity breakthroughs may be just over the horizon. How many gloomsters could have forecast the Internet or any other technical breakthrough before it actually happened? Jules Verne we are not.

But if a 2% or lower real growth forecast holds for most of the developed world over the foreseeable future, then it is clear that there will be investment consequences. Shown below, as recently published in a TIME Magazine article by Rana Foroohar, is a PIMCO list of future Picks and Pans based upon these ongoing structural changes:

Picks

· Commodities like Oil and Gold

· U.S. Inflation-Protected Bonds

· High-Quality Municipal Bonds

· Non-Dollar Emerging-Market Stocks

Pans

· Long-Dated Developed-Country Bonds in the U.S., U.K. and Germany

· High-Yield Bonds

· Financial Stocks of Banks and Insurance Companies

The list to a considerable extent reflects the view that emerging economy growth will continue to be higher than that of developed countries. Their debt on average will remain much lower, and their demographic age much younger. In addition, the inevitable policy response of developed economies to slower growth will be to reflate in order to minimize the impact of the aforementioned structural headwinds. If successful, reflationary policies will gradually move 10 to 30-year yields higher over the next several years. The 30-year Treasury hit its secular low of 2.50% in July and such a yield may seem ludicrous a decade hence. Investors should expect future annualized bond returns of 3–4% at best and equity returns only a few percentage points higher.

As John Lennon forewarned, it is getting harder to be someone, and harder to maintain the economic growth that investors have become accustomed to. The New Normal, like Strawberry Fields will “take you down” and lower your expectation of future asset returns. It may not last “forever” but it will be with us for a long, long time.

The Control Engineers and the Notion of Risk

Charles Gave, GaveKalThere is a great movie scene where Harpo and Groucho Marx meet in the “socialist restaurant.” Groucho says, “this food is disgusting and inedible!” To which Harpo replies, “and on top of that, the portions are far too small!” So by the late 1930s and the golden era of the Marx Brothers, it was already obvious that socialism was bad fare in high demand. Yet it took another half century for “scientific socialism” to be finally discredited in rivers of blood, murder and poverty. With the economic disasters wrought by socialism, one might have assumed that policymakers would accept that the future cannot be forecasted. The role of economists, governments and central banks is to promote a stable monetary and legal framework for the risk-takers (entrepreneurs, money managers etc.) to make their decisions as rationally as they could.

Unfortunately this has not happened. Instead, in a new and improved declination of Friedrich Hayek’s "fatal conceit," we seem to be moving away from “scientific socialism” to "scientific capitalism" – where the overconfident and overeducated control-engineers are no longer members of the avant garde of the proletariat, but plain, boring and well-meaning economists working in the entrails of the world central banks. My intent is not to show why these economists will fail (bigger and brighter minds such as Hayek, Mises, Friedman, etc. have already done this) – but rather to review the impact that the misguided manipulation of the price of money (exchange and interest rates) is having on the notion of risk.

In standard financial theory, most practitioners use the volatility of underlying assets as a measure of risk. To some extent, quantitative easing policies have had their biggest impact on this measure. Not only are prices totally artificial for a number of assets (government debt chief amongst them), but the volatility of these prices is also completely meaningless. Volatility no longer indicates the risks involved in holding certain assets, but instead measures the amount of the manipulation that the poor prices are enduring. For example, no-one today could say with a straight face that there is any information in the volatility of the euro-swiss exchange rate, or that this zero volatility adequately measures the risks that a Swiss based investor takes in buying euro-denominated assets.

So as a direct consequence of the manipulations of our well-meaning "control engineers" of market prices, today’s volatility readings have absolutely nothing to do with the underlying risks. From here, it is hard to escape the following conclusions:

· This will lead to the next disaster, for major financial accidents typically find their source in a misconception of risks, rather than a misconception of returns (e.g., Greek bonds are just as risky as German bonds, levered US mortgage bonds are as safe as houses, etc).

· Building a rational portfolio, where risks can be properly hedged, is almost impossible when market signals have disappeared (explaining the recent difficulties of so many macro and CTA hedge funds?).

Staying with the above ideas, consider that all the quantitative models and statistical techniques like “value at risk” will prove to be hopelessly wrong when true volatilities re-emerge (as they always do!). And when that occurs, who doubts that many financial institutions will, once again, find themselves in the line of fire. After all, as Karl Popper explained: "In an economic system, if the goal of the authorities is to reduce some particular risks, then the sum of all these suppressed risks will reappear one day through a massive increase in the systemic risk and this will happen because the future is unknowable". The sum of the risks in an economic system over time is a constant and the only question confronting economists is whether we should prefer to take our risk in small doses, or in a massive injection (as occurs when a fixed exchange rate system breaks down, or when a debt restructuring happens etc...)?

So in a world of “suppressed volatility,” the only smart thing a long-term investor can do is to buy the assets which have been sold because of their higher volatilities. This obviously is equities, and in particular, the very long duration equities of companies in technology, healthcare, energy, etc. A well-diversified portfolio of such shares will be volatile, but investors will likely see their money back over time and then some.

In fact, strange as it may seem, the only way to reduce the risk today is to own assets that still sport a "market price" – which will thus automatically have a very high volatility compared to the other assets exhibiting a very low, but artificial volatility. To reduce risk today, one has to build a very volatile portfolio! This is partly because a lot of non-volatile assets are extraordinarily risky. For example, I cannot think of more dangerous assets to own today than French or Japanese government bonds. I could easily imagine Groucho looking at a menu of JGBs and OATs and exclaiming, “these assets are terrible and have no yield”, only for Harpo to reply, “and their aren’t enough for everybody.” This last line will change rapidly when reality hits. Because economic history teaches us that no policymaker can control volatility for ever. The real hedge for portfolios today no longer is government fixed income, or even gold, but is instead volatility strategies.

Monday, December 17, 2012

Hussman: Destined for Economic Malaise

Roach Motel Monetary Policy

John P. Hussman, Ph.D.

All rights reserved and actively enforced.

Reprint Policy

While we continue to observe some noise and

dispersion in various month-to-month economic reports, the growth

courses of production, consumption, sales, income and new order

activity remain relatively indistinguishable from what we observed at

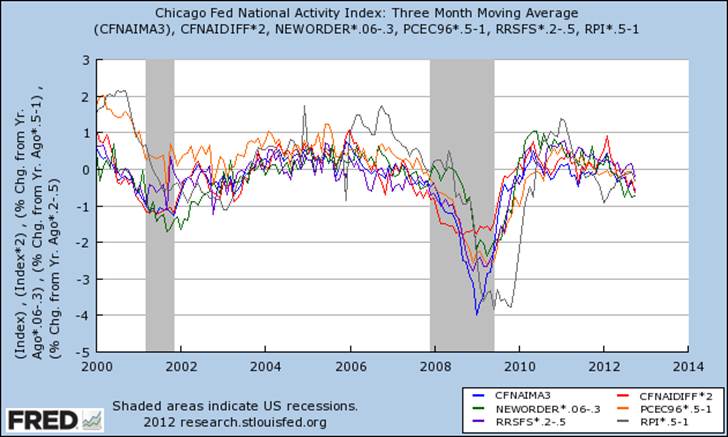

the start of the past two recessions. The chart below presents the

Chicago Fed National Activity Index (3 month average), the CFNAI

Diffusion Index (the percentage of respondents reporting improvement in

conditions, less those reporting deterioration, plus half of those

reporting unchanged conditions), and the year-over-year growth rates of

new orders for capital goods excluding aircraft, real personal

consumption, real retail and food service sales, and real personal

income. All values are scaled in order to compare them on a single

axis.

Strong leading indicators such as the

CFNAI and the Philly Fed Index have been weak for many months, and the

deterioration in new orders has moved from a slowing of growth to

outright contraction in recent months. In the order of events, a slowing

in real sales, personal income, and personal consumption expenditure

typically follows – these are called coincident indicators.

These growth rates generally only weaken materially once a recession is

in progress, and reach their highest correlation with recession about

6-months into the downturn. That’s what we’ve begun to observe over the

past few months, adding to our impression that the U.S. joined a global

(developed economy) recession during the third quarter of this year.

The most lagging set of economic indicators includes

employment measures, where I’ve frequently noted that the

year-over-year growth rate of payroll employment lags the year-over-year

growth rate of real consumption with a lag of about 5 months. As a

result, the year-over-year growth rate in payroll employment reaches

its highest correlation with recession nearly a year after a recession

has started – another way of saying that it is among the last

indicators to examine for confirmation of an economic downturn.

All of that said, our concern about recession

emphatically is not what drives our concern about the stock market

here. In early March, our measures of prospective return/risk moved to

the lowest 1% of historical data based on a broad ensemble of

indicators and consistent evidence of market weakness following similar

conditions in numerous subsets of historical data. Those conditions

remain largely in place today.

There’s no question that massive fiscal and

monetary interventions have played havoc with the time-lag between

unfavorable conditions and unfavorable outcomes in recent years, which

prompted us back in April to introduce various restrictions to our

hedging criteria (see below). Still, present conditions remain strongly

negative on our estimates. Meanwhile, the stock market is not “running

away” – at best, these interventions have allowed the market to churn

at elevated levels. Only a month ago, the S&P 500 Index was below

its level of March 2012, when our estimates shifted to the most negative

1% of the data, and was within about 11% of its April 2010 levels,

which is the last time that our present ensemble approach would have

encouraged a significant exposure to market risk. Notably, as of last

week, an upward spike in long-term Treasury yields took market

conditions to an overvalued, overbought, overbullish, rising yields

syndrome – which has tended to be anathema to the stock market, even

prior to the more limited downward bouts of recent years.

Beyond that, a natural question is – if recession

concerns don’t factor into our present defensiveness in the first

place, why should we be concerned about recession at all, and devote so

much analysis to this issue in the weekly comments? The first answer

is that the foundation of this particular cyclical bull market has

rested on the continuation of massive fiscal and monetary

interventions, and a new recession would stretch those interventions to

untenable limits (and to some extent already have), which should be of

concern regardless of one’s stock market views. The second answer is

that much of Wall Street’s overbullish sentiment, as well as its

“valuation” case for stocks, rests on the continuation of record high

profit margins that are largely an artifact of extreme government

deficits and depressed personal savings (see Too Little To Lock In).

A contraction in sales, coupled with a contraction in profit margins –

which is what we presently expect – is likely to devastate the

“forward operating earnings” case for stocks, and I continue to expect

Wall Street to be blindsided by this fairly predictable outcome (as it

was in 2001-2002, as it was in 2008-2009).

The distortions we presently observe in the

economy will have significant long-term costs, but it is entirely naïve

to believe that these costs should be evident precisely at the point

where the wildest distortions are taking place. Federal deficits

presently support about 10% of economic activity, and the primary

driver of improvement in the unemployment rate has not been job

creation but a plunge in labor participation, as millions of workers

drop out of the labor force. In a post-credit crisis environment, and

particularly with Europe’s sovereign debt in question, it should be no

surprise that the world has been willing to accumulate U.S. currency and

Treasury debt at near-zero interest rates. That makes debt seem benign

and money creation seem without consequence. But it is absurd to point

at that happy short-term outcome and dance under the illusion that

escalating debt won’t matter in the longer term, or that massive money

creation will be easily reversed, or that strong inflation will be

avoided if it is not reversed.

We have already accumulated enough government debt

to place a broad range of current and future government services under

a cloud. Given that most of the publicly held U.S. government debt is

of short maturity, there is no way of inflating away its real value

over time, because interest rates would adjust at each rollover of that

debt. In the event that the sheer size of the U.S. debt results in a

loss of confidence (which is a 5-10 year proposition, though not yet a

present one), there is no reason that we could not expect the same

short-term funding strains that many European countries are facing in

fits and starts today.

Meanwhile, last week, Ben Bernanke announced that

the current “Twist” program (where the Fed buys long-term Treasuries

and sells an equal amount of shorter-dated Treasuries) will be replaced

with outright “unsterilized” bond purchases. In doing so, Ben Bernanke

has put the economy on course to choke down 27 cents of

monetary base for every dollar of nominal GDP by the end of next year –

in an economy where even the slightest normalization to interest rates

of just 2% would require the monetary base to be cut to just 9 cents

per dollar of GDP to avoid inflationary outcomes. The chart below is a

reminder of where we are already.

Understand that Fed policy now requires

interest rates to remain near zero indefinitely, because competition

from non-zero interest rates would reduce the willingness to hold

zero-interest currency, provoking inflationary outcomes unless the

monetary base was quickly reduced. Given an economy perpetually at the

edge of recession, so far, so good. But as interest rates essentially

measure the value that an economy places on time, Ben Bernanke's message to the U.S. economy is clear: time is worthless.

Monetary policy has become a roach motel – easy

enough to get into, but impossible to exit. Bernanke seems pleased to

note that inflation presently remains low, but why shouldn’t it? In a

structurally weak economy, velocity drops in exact proportion to new

monetary base, with zero effect on real output or inflation.

The problem is that Bernanke seems incapable of running thought

experiments. Suppose the economy eventually strengthens at some point

past 2013. At that point, the Fed would have to sell nearly $3 trillion

of U.S. debt into public hands in order to reabsorb the money creation

he claims “is only a temporary matter.” These sales would add to the

stock of U.S. debt already held by the public, very likely while a

significant government deficit is still in place. Such a sale would be,

by two orders of magnitude, the largest monetary tightening in U.S.

history. Is that possible to achieve without disruption? I doubt it.

So instead, the Fed must rely on the economy

remaining weak indefinitely, so it will never be forced to materially

contract its balance sheet. To normalize the Fed’s balance sheet

without contraction and get from 27 cents back to 9 cents of base money

per dollar of GDP without rapid inflation, we would require over 22 years

of suppressed interest rates below 2%, assuming GDP growth at a 5%

nominal rate. Indeed, Japan is on course for precisely that outcome,

having tied its fate 13 years ago to Bernanke’s experimental prescription

(stumbling along at real GDP growth of less than 1% annually since

then). Bernanke now sees fit to inject the same bad medicine into the

veins of the U.S. economy. Of course, a tripling in the consumer price

index would also do the job of bringing the monetary base back from 27

cents to 9 cents per dollar of nominal GDP. One wonders which of these

options Bernanke anticipates. Psychotic.

Big picture – my perspective remains unchanged:

the long-term viability of the global economy is being increasingly

wrecked by short-sighted policies focused on avoiding short-term

economic adjustments, and at bottom, on avoiding the restructuring of

unserviceable sovereign, mortgage and financial debt. Yet only that

restructuring is capable of unchaining the economy from reckless past

misallocations; only that restructuring is capable of unleashing robust

new demand that would form the basis for sustainable economic activity

and job creation. You either pull the bad tooth, or you provide every

kind of pain killer and symptom reliever, and let the problem rot

indefinitely.

From an investment perspective, we know that the

impact of quantitative easing both in the U.S. and abroad has generally

been limited to a rally in stocks toward the highs of the prior

6-month period, in some cases moving as high as the monthly Bollinger

band (2 standard deviations above the 20-month average). Given that the

S&P 500 is within a few percent of its highs, and that conditions

have already established an overvalued, overbought, overbullish,

rising-yields conformation, much of the “benefit” of QE on stocks

appears already priced in, as it has been since October when Bernanke

effectively announced the present policy. The downside risk overwhelms

the upside potential, in my view, but we can’t confidently rule out

some amount of upside potential – which would still seem dependent on

the avoidance of negative economic surprises.

Subscribe to:

Posts (Atom)