The Managing Director of the IMF, Christine Lagarde has warned politicians and policy makers from across the globe they must unite and take bold action to avoid a financial meltdown. Tough economic decisions such as tax hikes must not be delayed for the sake of electoral expediency, she said.

Showing posts with label taxation. Show all posts

Showing posts with label taxation. Show all posts

Friday, September 16, 2011

Monday, May 30, 2011

Taxes on Traders Almost Certain to Go Up

Traders Accounting just sent me this! There are at least FOUR new taxes in this. This will encourage capital flight to overseas. Bad news for the U.S. economy!

from Traders Accounting:

With lawmakers putting an increasing emphasis on the federal budget deficit, Bloomberg reports it is likely those day trading for a living could see a number of tax increase in 2013.

Unless Congress acts, the federal tax cuts extended last year are set to expire at the end of 2012. Once they expire, day traders will see taxes on incomes, capital gains and dividends all rise moving into 2013.

Compounding the issue, those in higher income brackets are also set to deal with higher unearned income taxes in 2013 to pay for the government's health insurance plans.

"The deficit is an issue," Bill Fleming, managing director at New York-based accounting and advisory firm PricewaterhouseCoopers, told the news source. He added many people "have already decided in their minds that something is going to happen and they're going to pay higher taxes."

Bloomberg says the White House has proposed to allow taxes on capital gains and dividends to jump from 15 to 20 percent. In addition, the tax rate for couples earning more than $250,000 or individuals earning more than $200,000 would jump from 35 percent to 39.6 percent.

Last year, a commission set up to brainstorm ways to reduce the deficit proposed dropping the overall income tax rate, but including capital gains taxes and dividends and standard income.

With these ongoing shifts and changes, traders may have trouble keeping up with their tax needs. Experts say some may be better off delegating that work in order to focus more on the heart of the business.

Monday, April 4, 2011

WSJ Explains How to Pull a "GE"

Wow! I wish I had known!!

from WSJ:

There's been a firestorm this week over the news that General Electric will pay no tax—at least, no federal corporate income tax—on last year's profits.

But if you're like a lot of people, your first reaction was probably: "Hmmm. How can I get that kind of deal?"

You'd be surprised. You might. And without being either a pauper or a major corporation.

I spoke to Gil Charney, principal tax researcher at H&R Block's Tax Institute, to see how a regular Joe could pull a GE. The verdict: It's more feasible than you think—especially if you're self-employed.

Let's say you set up business as a consultant or a contractor, something a lot of people have been doing these days. And, to make this a challenge on the tax front, let's say you do well and take in about $150,000 in your first year.

First off, says Mr. Charney, for 2010 you can write off up to $10,000 in start-up expenses. (In subsequent years it's only $5,000.)

Okay, let's say you claim $7,000. That takes your income down to $143,000.

You can also write off all legitimate business expenses. Mr. Charney emphasizes that this only applies to legitimate expenses.

He didn't say, but everyone seems to understand, that this can be quite a flexible term. Even if you buy a computer, a cellphone and a car primarily for business use, you can use them for personal purposes as well. If you happen to take a business trip to Florida in, say, January, no one is going to stop you from enjoying the sunshine or taking a dip in the pool.

So let's say you manage to write off another $10,000 a year in business expenses.

That brings your income, for tax purposes, down to $133,000.

You'll have to pay Medicare and Social Security taxes (just like GE). Because you're self-employed, you have to pay both sides: the employee and the employer. That will come to about $19,000.

However, you can deduct half of that, or $9,500, from your taxable income. So that brings your total down to $123,500 so far.

Now comes the creative bit. The self-employed have access to terrific tax breaks on their investment and retirement accounts. The best deal for many is going to be a self-employed 401(k), sometimes known as a Solo 401(k).

This will let you save $43,100 and write it off against your taxes. That money goes straight into a sheltered investment account, as with a regular 401(k).

Why $43,100? That's because with a Solo 401(k), you're both the employer and the employee. As the employee you get to contribute a maximum of $16,500, as with any regular 401(k). But as the employer you also get to lavish yourself with an incredibly generous company match of up to 20% of net income.

Yes, being the boss has its privileges. (And if you're 50 or over, your limit as an employee is raised from $16,500 each to $22,000.)

You can save another $10,000 by also contributing to individual retirement accounts—$5,000 for you, $5,000 for your spouse. If you use a traditional IRA, rather than a Roth, that reduces your taxable income as well. If you're 50 or over, the limit rises to $6,000 apiece.

If you contribute $43,100 to your Solo 401(k), and $10,000 to two IRAs, that brings your income for tax purposes down to just over $70,000.

We haven't stopped there either, says Mr. Charney.

Now come the usual itemized deductions. You can write off your state and local taxes. Let's say these come to $10,000.

You can write off interest on your mortgage. Call that another $10,000. That's enough to pay 5% interest on a $200,000 home loan.

That gets us down to about $50,000 And we're not done.

If you're self-employed, health insurance is probably a big headache. But the news isn't all bad. You can write off the premiums for yourself, your spouse, and your kids.

And if you use a qualifying high-deductible health insurance plan—there are a variety of rules to make sure a plan qualifies—you get another break. You can contribute $3,050 a year into a tax-sheltered Health Savings Account, or $6,150 for a family. You can write those contributions off against your taxable income. The investments grow sheltered from tax. And if you spend the money on qualifying health costs, the withdrawals are tax-free as well.

So call this $10,000 for the premiums and $6,150 for the HSA contributions. That gets your income, for tax purposes, all the way down to about $34,000.

If you have outstanding student loans, you can write off $2,500 in interest. And you can write off $4,000 of your kid's college tuition and fees.

Then there's a personal exemption: $3,650 per person. If you're married with one child, that's $10,950.

Taxable income: just under $17,000. That's on a gross take of $150,000. You'd owe less than $1,700 in federal income tax.

And it doesn't stop there. Because now you can bring in some of the tax credits. Unlike deductions, these come off your tax liability, dollar for dollar.

GE got big write-offs related to green energy. There are some for you too, although on a small scale. You can claim credits for things like installing solar panels, heat pumps or energy-efficient windows or boilers in your home. Let's say you use a home equity loan to pay for the improvements and take the maximum $1,500 write-off.

That gets your tax liability down to $200.

Can we get rid of that? Sure, says Mr. Charney.

If your spouse spends, say, $1,000 on qualifying adult-education courses or training programs, you can claim $200, or 20% of the cost, in Lifetime Learning Credits. (The maximum is $2,000.)

That wipes out the remaining liability.

Congratulations. You've pulled a GE. You owe no federal income taxes at all.

OK, it's just an illustration. Few will be quite so fortunate. On the other hand, it's not comprehensive either. There are plenty of other deductions and credits we didn't mention. You could have written off up to $3,000 by selling loss-making investments. Your spouse may be able to use a 401(k) deduction as well. There are lots of ways to tweak the numbers.

In this case, you've paid no federal income tax, and meanwhile you've saved $19,000 toward your retirement through Social Security and Medicare, and $53,000 through your 401(k) and IRAs. You've paid most of your accommodation costs (that is, the interest and property taxes on your home), covered your health-care costs and quite a lot of personal expenses through your business account, paid $4,000 toward your child's college costs and had about $2,000 a month left over for cash costs.

Who says GE has all the fun?

Friday, August 20, 2010

Congress' New Mantra of Spend and Tax!

by David Asman at Fox Business:

The phrase used to be “tax and spend.” But now it's "spend and tax" -- spend money before you raise it, and then tax later to pay off the bills. That's not only irresponsible; it doesn't work.

The phrase used to be “tax and spend.” But now it's "spend and tax" -- spend money before you raise it, and then tax later to pay off the bills. That's not only irresponsible; it doesn't work. But still we have a lot of Democrats and some Republicans saying that we have to raise tax rates to pay off the deficit.

They usually cite Bill Clinton as an example of a president who balanced the budget by raising tax rates. But they never mention that Bill Clinton's surplus wasn't created by taxing more, but by spending less.

First off, he saved hundreds of billions of dollars by spending less on defense thanks to the end of the Cold War. The defense budget went from 4.4% of GDP when he took office down to 3% of the GDP when he left. That meant a savings of $145 billion dollars in 1997 alone!

He also saved billions by going along with a Republican plan to fundamentally restructure welfare, a genuine bipartisan reform that we're now in danger of undoing.

There were also the billions that came into the Treasury because of the dot com bubble that peaked just before Clinton left office. And ironically, a lot of this money flowed into the Treasury because of a tax rate cut in the capital gains tax.

In other words, Clinton didn't leave office with a surplus because of higher tax rates, but because of much less spending and a critical tax cut!

Democrats or Republicans who cite Bill Clinton to back up this phony idea that we need to raise tax rates to pay off the irresponsible spending of the past couple of years don't know their history.

They're giving big-government spenders an excuse not to cut back. And cutting back big government is the only way to cut the deficit.

Tuesday, August 3, 2010

Forbes Making the Case for Commodities

from Forbes mag:

It's been a frustrating and volatile year for stock market investors. Just when we thought we were out of the woods after the financial market crisis, trouble in the eurozone reintroduced the possibility of a global double-dip recession. Both the Dow Jones Industrial Average and the Standard & Poor's 500 fell into the red this summer. U.S. Treasuries and cash may be safe, but where do you find return?

Gold has historically served as a safe haven in times of economic distress and has performed extraordinarily well over the past decade. Gold prices have risen for nine straight years, including a 24% gain in 2009. This May the metal reached a nominal record high north of $1,200 per ounce. All told. gold is up 8% so far this year.

Investors can access gold by buying coins or bullion, gold exchange-traded funds, like

In Pictures: Seven Ways To Invest In Gold

While investors are familiar with gold, they may be missing an opportunity to participate in markets that offer similar diversification, including grains and energies. As with any asset class, investing in these commodities requires considering a number of issues and risk factors. Following are some of the most important ones.

Timing: In 1999, when the stock market was booming, commodities were a hard sell. Gold was trading below $300 an ounce. Crude oil was trading under $20 a barrel. Over the course of the following decade, gold rose 278% and crude oil 183%. Compare that with the "lost" decade for stocks.

One thing stocks and commodities have in common is that investors tend to buy them when they probably should be most cautious--when prices are near record highs. On the flipside, few investors were interested in buying crude oil contracts in 2009. Instead of going along with the crowd, however, ask yourself: What markets are over- or under-valued based on historical standards? And, how can I take advantage of that?

Pricing: When you buy or sell gold coins or jewelry, the price you pay or receive doesn't mirror the futures price due to the influence of retail demand and mark-ups. A coin or piece of jewelry is altered rather than a pure play on the commodity.

That's why many investors turn to ETFs or individual sector stocks to gain exposure to gold and other commodities, which are impractical to store and hold. Even when you invest in commodity-based stocks or ETFs, however, you aren't getting a perfect correlation to the price of the actual commodity. In fact, returns may vary significantly.

Investors who choose commodity futures get the purest play and are not subject to company-specific issues as they are when owning stocks or ETFs. Futures also enable investors to take positions on either side of the market and profit from a price decline as well as from a gain. If you feel the price of gold is going up, you can buy a gold futures contract (go long). If you feel it's going down, you can sell a contract (go short). Returns are not dependent on market direction, and unlike with ETFs and stocks, electronic futures markets are open nearly 24 hours a day.

Risk: The biggest risk with a stock or ETF is that it will become worthless and you'll lose your entire investment. Commodity futures, by contrast, are backed by tangible value that is unlikely to go to zero, but often they incorporate other risks. Often, investors buy them by putting down 10% or less of a full futures contract's value to hold a position. This is similar to using a down payment to buy a house. If you use leverage, both your gains and losses are magnified.

Success with futures involves a degree of skill, market knowledge and good timing. You need to be able to monitor your positions closely, and apply appropriate risk-controls. If you don't favor the do-it-yourself approach, work with a professional broker who can act as an advisor.

You can also access commodity futures though a managed account, which is even more hands-off. Managed accounts are akin to mutual funds; you pick the commodity fund or manager and he or she makes the trading decisions.

Taxes: ETFs are typically taxed like stocks, based on your holding period. That's fine if you are a buy-and-hold investor. If you're a more active trader, short-term capital gains can take a big hit out of your returns.

In the U.S., futures are lumped together and reported on a single Form 1099 at year-end. Profits, if any, are taxed regardless of the holding period at a 60/40 rate--60% at the favorable long-term capital gains rate and 40% at the short-term capital gains rate.

Gold coins or bullion can be taxed as "collectibles" subject to the 28% tax rate. ETFs backed by gold or silver can also be subject to this collectible rate. Higher rates and/or penalties may be applied if investments deemed "collectibles" are included in an independent retirement account or other self-directed retirement account. Consult with an accountant when making your investment choice.

Mark Sachs is president of Lind-Waldock, a Chicago-based futures brokerage division of MF Global.

Thursday, July 22, 2010

The Tax Man Cometh Jan 1

Fiscal Policy: Many voters are looking forward to 2011, hoping a new Congress will put the country back on the right track. But unless something's done soon, the new year will also come with a raft of tax hikes — including a return of the death tax — that will be real killers.

Through the end of this year, the federal estate tax rate is zero — thanks to the package of broad-based tax cuts that President Bush pushed through to get the economy going earlier in the decade.

But as of midnight Dec. 31, the death tax returns — at a rate of 55% on estates of $1 million or more. The effect this will have on hospital life-support systems is already a matter of conjecture.

Resurrection of the death tax, however, isn't the only tax problem that will be ushered in Jan. 1. Many other cuts from the Bush administration are set to disappear and a new set of taxes will materialize. And it's not just the rich who will pay.

The lowest bracket for the personal income tax, for instance, moves up 50% — to 15% from 10%. The next lowest bracket — 25% — will rise to 28%, and the old 28% bracket will be 31%. At the higher end, the 33% bracket is pushed to 36% and the 35% bracket becomes 39.6%.

But the damage doesn't stop there.

The marriage penalty also makes a comeback, and the capital gains tax will jump 33% — to 20% from 15%. The tax on dividends will go all the way from 15% to 39.6% — a 164% increase.

Both the cap-gains and dividend taxes will go up further in 2013 as the health care reform adds a 3.8% Medicare levy for individuals making more than $200,000 a year and joint filers making more than $250,000. Other tax hikes include: halving the child tax credit to $500 from $1,000 and fixing the standard deduction for couples at the same level as it is for single filers.

Letting the Bush cuts expire will cost taxpayers $115 billion next year alone, according to the Congressional Budget Office, and $2.6 trillion through 2020.

But even more tax headaches lie ahead. This "second wave" of hikes, as Americans for Tax Reform puts it, are designed to pay for ObamaCare and include:

The Medicine Cabinet Tax

The HSA Withdrawal Tax Hike. "This provision of ObamaCare," according to ATR, "increases the additional tax on nonmedical early withdrawals from an HSA from 10% to 20%, disadvantaging them relative to IRAs and other tax-advantaged accounts, which remain at 10%."

Brand Name Drug Tax. Makers and importers of brand-name drugs will be liable for a tax of $2.5 billion in 2011. The tax goes to $3 billion a year from 2012 to 2016, then $3.5 billion in 2017 and $4.2 billion in 2018. Beginning in 2019 it falls to $2.8 billion and stays there. And who pays the new drug tax? Patients, in the form of higher prices.

Economic Substance Doctrine. ATR reports that "The IRS is now empowered to disallow perfectly legal tax deductions and maneuvers merely because it judges that the deduction or action lacks 'economic substance.'"

A third and final (for now) wave, says ATR, consists of the alternative minimum tax's widening net, tax hikes on employers and the loss of deductions for tuition:

• The Tax Policy Center, no right-wing group, says that the failure to index the AMT will subject 28.5 million families to the tax when they file next year, up from 4 million this year.

• "Small businesses can normally expense (rather than slowly deduct, or 'depreciate') equipment purchases up to $250,000," says ATR. "This will be cut all the way down to $25,000. Larger businesses can expense half of their purchases of equipment. In January of 2011, all of it will have to be 'depreciated.'"

• According to ATR, there are "literally scores of tax hikes on business that will take place," plus the loss of some tax credits. The research and experimentation tax credit will be the biggest loss, "but there are many, many others. Combining high marginal tax rates with the loss of this tax relief will cost jobs."

• The deduction for tuition and fees will no longer be available and there will be limits placed on education tax credits. Teachers won't be able to deduct their classroom expenses and employer-provided educational aid will be restricted. Thousands of families will no longer be allowed to deduct student loan interest.

Then there's the tax on Americans who decline to buy health care insurance (the tax the administration initially said wasn't a tax but now argues in court that it is) plus a 3.8% Medicare tax beginning in 2013 on profits made in real estate transactions by wealthier Americans.

Not all Americans may fully realize what's in store come Jan. 1. But they should have a pretty good idea by the mid-term elections, and members of Congress might take note of our latest IBD/TIPP Poll (summarized above).

Fifty-one percent of respondents favored making the Bush cuts permanent vs. 28% who didn't. Republicans were more than 4 to 1 and Independents more than 2 to 1 in favor. Only Democrats were opposed, but only by 40%-38%.

The cuts also proved popular among all income groups — despite the Democrats' oft-heard assertion that Bush merely provided "tax breaks for the wealthy." Fact is, Bush cut taxes for everyone who paid them, and the cuts helped the nation recover from a recession and the worst stock-market crash since 1929.

Maybe, just maybe, Americans remember that — and will not forget come Nov. 2.

Friday, July 16, 2010

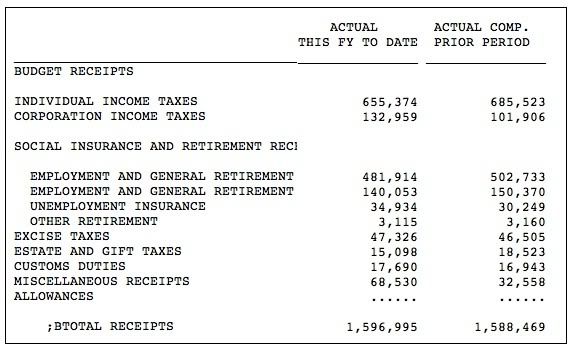

Federal Income Tax Recepts Still Falling

from Bizzy Blog:

It’s bad enough the federal government’s official budget deficit has topped $1 trillion for the second year in a row, according to the just-released June 2010 Monthly Treasury Statement. But, focusing only on receipts for the moment, a closer look makes it obvious that the situation is even worse than it appears. Don’t expect the establishment press to take any interest in the annoying but revealing details that follow.

Here is what Martin Crutsinger of the Associated Press wrote about federal collections in his Tuesday report on Uncle Sam’s current month and fiscal year deficit:

Through the first nine months of the current budget year, government revenues have totaled $1.6 trillion, up 0.5 percent from the same period a year ago.True enough, but look at the components:

Answer: Over $54 billion of it is from the Federal Reserve. As best I can tell, it represents dividends and interest on TARP lending and investments. This component of miscellaneous receipts is up by a factor of about 2.7 from fiscal 2009’s comparable year-to-date amount of $19.9 billion.

So the only reason receipts are up is that the Fed got into the direct lending and investment business. Tax collections that are indicators of the health of the overall economy are still down over last year, which was in turn down about 18% from the same period in fiscal 2008.

That’s not much comfort, is it?

Tuesday, May 18, 2010

State Tax Collections Continue to Flounder

April tax collections are falling short of forecasts and even dropping below last year's depressed levels in a number of states, complicating budget troubles and prompting some governors to dip into rainy-day funds.

Following several months of modest improvement, the weak April revenue numbers are disappointing for states that hoped for economic recovery soon.

Based on reports from more than a dozen states, the figures suggest the recession may have taken a heavier-than-expected toll on employment last year, cutting into income taxes.

The shortfalls also are punching fresh holes in state budgets. Widening state deficits could in turn put pressure on the federal government to issue new stimulus funding; a 2009 cash injection from Washington has helped shore up battered state finances, but much of that will dry up by the end of this year.

April is the biggest revenue month for many states because it is when they collect a large portion of income taxes. The month's collections came up short of expectations in California by 26.4%, or $3.6 billion; in Pennsylvania by 11.8%, or $390.1 million; and in Kansas by 10.2%, or $65.3 million. More states will report in the next few weeks.

In some states—including a few where April tax collections fell short of forecasts—revenue actually increased slightly from the same month a year ago.

But even if the results topped last year's, states that received lower-than-expected income in April still may need to reduce spending to balance budgets. All states except Vermont have at least a limited requirement to balance their budgets, so must adjust to revenue shortfalls.

The weak tax revenue also could mask good news, such as improving sales-tax collections, said Donald Boyd, a senior fellow at the Nelson A. Rockefeller Institute of Government at the State University of New York. Sales taxes better reflect current economic conditions than some other revenue categories.

Friday, February 5, 2010

“I am really worried about the United States … more worried than I’ve ever been in my career” Bob McDonald, CEO, Proctor and Gamble

John J. Castellani, president of the Business Roundtable, an association of chief executive officers of large U.S. companies, had this to say in May when Obama first proposed the changes: “President Obama’s plan today to increase taxes on American corporations is the wrong idea at the wrong time for the wrong reasons. This plan will reduce the ability of U.S. companies to compete in foreign markets, which will not only reduce jobs, but will also cripple economic growth here in the United States. It couldn’t come at a worse time.”

"I worry a lot about the United States," McDonald told Reuters in an interview from his company's Cincinnati headquarters. "I worry about the deficit, I worry about an uncertain future."

McDonald said he has told government officials that they must "create greater certainty for business." The shift in tax policy toward multinational companies "would be a dumb thing to do" as it would make U.S. companies less competitive versus foreign ones.

Wednesday, December 16, 2009

Home Buyer Tax Credit Is a Failure

As the CHART OF THE DAY shows, the National Association of Home Builders/Wells Fargo Housing Market Index and a Standard & Poor’s index of homebuilding shares dropped after Obama signed the legislation on Nov. 6. The chart tracks these indicators since 2000.

Homebuyers received another five months, until April 30, to take advantage of the government’s $8,000 credit. They also became eligible for an additional $6,500 credit if they owned their previous residence for at least five years.

“The extension has not materially helped traffic or sales despite the program’s expansion,” Carl Reichardt, a Wells Fargo analyst, wrote yesterday in a report.

The NAHB/Wells Fargo index, an indicator of builders’ confidence, fell to 16 this month from 17 in November. None of the 47 economists in a Bloomberg News survey expected the decline. Readings below 50 show that most participants are pessimistic.

Monday, December 7, 2009

To Roth or Not to Roth?

from WSJ:

By ANNE TERGESEN

Roth IRAs are currently off-limits to a whole group of people. Individuals with modified adjusted gross income of $120,000 or more can't contribute to one of these accounts. For married couples, the threshold is $176,000. And individuals with modified adjusted gross income of more than $100,000 and married taxpayers who file separate returns are barred from moving assets held in traditional IRAs into Roth IRAs.

![[Tim foley]](http://s.wsj.net/public/resources/images/OB-FA482_sun120_DV_20091204180756.jpg) Tim Foley

Tim Foley Money When You Want It

Under the new rules, high-income taxpayers who wish to contribute to a Roth IRA are still out of luck: Income limitations on funding these accounts will remain in effect. However, Uncle Sam's decision to allow high earners to convert will give these individuals a back-door way to fund a Roth on a continual basis.How so? Each year, these taxpayers can open a traditional IRA (which has no income limits) and contribute the maximum (currently, $6,000 for individuals age 50 and older) on a pretax or aftertax basis. Then, they can convert the assets to a Roth IRA.

Why bother with a conversion? Roths have several advantages over traditional IRAs.

Perhaps the biggest one concerns taxes -- or a lack thereof. For the most part, withdrawals from Roth IRAs are tax-free as long as an account holder meets the rules for minimum holding periods. If you convert assets to a Roth from other IRAs or retirement plans, you have to hold those assets in a Roth for five years, or until you turn age 59½, whichever comes first, to make penalty-free withdrawals on your converted amounts. Each conversion has its own five-year clock.

Another benefit: no required distributions. With a traditional IRA, individuals are required to begin tapping their accounts -- and to pay taxes on those withdrawals -- after reaching age 70½. Roth accounts aren't subject to mandatory distributions, so the money in a Roth can grow tax-free for a longer period of time.

![[Lede]](http://s.wsj.net/public/resources/images/SJ-AD994_LEDECH_NS_20091204190020.gif)

Tax Bill Upfront

Still, there is a cost to converting to a Roth -- namely, the income-tax bill. When you withdraw money from your traditional IRA, you will have to pay income tax on the withdrawal, or, more precisely, on the portion of it that represents pretax contributions and earnings.In 2010, Uncle Sam is offering taxpayers who convert a special deal: They can choose to report the amount they convert on their 2010 tax returns, or they can spread it equally across their 2011 and 2012 returns. (If you are worried that Congress may raise tax rates, consider paying the tax bill in 2010.)

To determine whether it makes financial sense for you to convert, it's important to consider various factors. For example, converting may be the right move if you expect to pay higher future tax rates or if the value of your IRA account is temporarily depressed, says Ed Slott, an IRA consultant in Rockville Centre, N.Y. In either case, by converting to a Roth today you'll lock in a lower tax bill than you would otherwise pay.

To estimate your potential tax bill, first calculate your "basis." Expressed as a percentage, this is the ratio of two numbers: aftertax contributions you have made to your IRAs (if any), and the total balance in all your IRAs.

For example, if you contributed $40,000 aftertax to your IRAs and have a total of $250,000 in those accounts, your basis would be 16% (or $40,000 divided by $250,000). As a result, if you plan to convert $100,000 to a Roth, 16% of that $100,000 (or $16,000) could be transferred tax-free.

Another factor is how long you can afford to leave the money in a Roth. Because the Roth's major advantage lies in its ability to deliver tax-free growth from age 70½, the longer you can afford to forego withdrawals, "the more converting plays to your advantage," says Aimee DeCamillo, head of personal retirement solutions at Merrill Lynch Wealth Management.

Before pulling the trigger, speak to a financial adviser. You also can crunch the numbers using online calculators at sites including RothRetirement.com and Fidelity.com/rothevaluator.

Maximize the Benefit

If you determine that it pays to convert, the following strategies can help you maximize the benefit:Financial experts say it's ideal to have money to pay the taxes due upon conversion from a source other than your IRA. That allows you to retain a bigger sum in your tax-sheltered retirement plan.

Keep in mind that you don't have to convert your entire IRA. It might make sense to do it piecemeal, as you can afford it, over a number of years.

Put converted holdings into a new account, rather than an existing Roth. That way, if the value falls after you've paid the tax bill, you can change your mind, "recharacterize" the account (meaning you move the money back into a traditional IRA) and wipe out your income-tax liability.

You have until Oct. 15 of the year following the year of conversion to recharacterize. For example, if you were to convert your IRA to a Roth in 2010, you would have until Oct. 15, 2011 to recharacterize it. Later on, you could choose to convert the assets to a Roth again.

Better still: Consider opening a separate Roth for each type of investment you hold. That way, you can recharacterize the ones that perform poorly and leave the winners alone.

Tuesday, August 4, 2009

Revenue Reversal

from AP:

WASHINGTON – The recession is starving the government of tax revenue, just as the president and Congress are piling a major expansion of health care and other programs on the nation's plate and struggling to find money to pay the tab.

The numbers could hardly be more stark: Tax receipts are on pace to drop 18 percent this year, the biggest single-year decline since the Great Depression, while the federal deficit balloons to a record $1.8 trillion.

Other figures in an Associated Press analysis underscore the recession's impact: Individual income tax receipts are down 22 percent from a year ago. Corporate income taxes are down 57 percent. Social Security tax receipts could drop for only the second time since 1940, and Medicare taxes are on pace to drop for only the third time ever.

The last time the government's revenues were this bleak, the year was 1932 in the midst of the Depression.

"Our tax system is already inadequate to support the promises our government has made," said Eugene Steuerle, a former Treasury Department official in the Reagan administration who is now vice president of the Peter G. Peterson Foundation.

"This just adds to the problem."

While much of Washington is focused on how to pay for new programs such as overhauling health care — at a cost of $1 trillion over the next decade — existing programs are feeling the pinch, too.

Social Security is in danger of running out of money earlier than the government projected just a few month ago. Highway, mass transit and airport projects are at risk because fuel and industry taxes are declining.

The national debt already exceeds $11 trillion. And bills just completed by the House would boost domestic agencies' spending by 11 percent in 2010 and military spending by 4 percent.

For this report, the AP analyzed annual tax receipts dating back to the inception of the federal income tax in 1913. Tax receipts for the 2009 budget year were available through June. They were compared to the same period last year. The budget year runs from October to September, meaning there will be three more months of receipts this year.

Is there a way out of the financial mess?

A key factor is the economy's health. The future of current programs — not to mention the new ones Obama is proposing — will depend largely on how fast the economy recovers from the recession, said William Gale, co-director of the Tax Policy Center.

"The numbers for 2009 are striking, head-snapping. But what really matters is what happens next," said Gale, who previously taught economics at UCLA and was an adviser to President George H. W. Bush's Council of Economic Advisers.

"If it's just one year, then it's a remarkable thing, but it's totally manageable. If the economy doesn't recover soon, it doesn't matter what your social, economic and political agenda is. There's not going to be any revenue to pay for it."

Tuesday, July 7, 2009

Still More Taxes to Steal from the Rich

I have never reached the income level required to pay this level of taxes, but I'm opposed to it because it violates the "equal treatment" clause of the Constitution and because it violates two of the Ten Commandments: 1) Thou shalt not covet, and 2) Thou shalt not steal.

Stealing is still stealing, whether we do it with our hands, or with our votes through a shameless politician. Either way, it is the same! The Founders understood this:

"The moment the idea is admitted into society that property is not as sacred as the laws of God, and that there is not a force of law and public justice to protect it, anarchy and tyranny commence. If `Thou shalt not covet' and `Thou shalt not steal' were not commandments of Heaven, they must be made inviolable precepts in every society before it can be civilized or made free." -- John Adams (A Defense of the American Constitutions, 1787)

Anarchy and tyranny are our legacy as we engage in wealth transfers. God will not stand by us!

from Bloomberg:

House Ways and Means Committee members are likely to propose a surtax on high-income Americans to help pay for an overhaul of the health-care system, according to people familiar with the plan.

The tax would be similar to, yet much smaller than, a surtax proposed in 2007 by Ways and Means Committee Chairman Charles Rangel, a person familiar with the committee’s talks said. That plan would have added at least a 4 percent levy on incomes exceeding $200,000, and was projected to reap as much as $832 billion over 10 years.

Two people familiar with closed-door talks by committee Democrats said a House bill probably will include a surtax on incomes exceeding $250,000, as Congress seeks ways to pay for changes to a health-care system that accounts for almost 18 percent of the U.S. economy. By targeting wealthier Americans, a surtax may hold more appeal for House Democrats than a Senate proposal to tax some employer-provided health benefits.

“The surtax is obviously more attractive to Democrats in the House because it’s more progressive, which they find attractive in and of itself,” said Paul Van de Water, a senior fellow at the Washington-based Center on Budget and Policy Priorities, a research group focused on policies affecting low- and moderate-income families.

Supporters on the Ways and Means Committee include Representative Lloyd Doggett, a Texas Democrat who backs including a surtax among revenue-raising measures in a health- care package, Doggett spokeswoman Sarah Dohl said.

Republicans in Congress, and some Senate Democrats, are likely to fight moves to increase tax rates, said Clinton Stretch, who analyzes tax legislation at Deloitte Tax LLP, a Washington consulting firm.

Republican Opposition

“This will be a point of discomfort for moderate or conservative Democrats” in the Senate, he said. “It will be an anathema for Republicans.”

The possibility of raising taxes on top earners surfaced last month as a revenue option for members of Rangel’s committee, and the people familiar with the talks cautioned that no agreement has been reached. A Senate plan to tax the value of employee benefits that exceed coverage for federal workers may generate as much as $418.5 billion over 10 years, though talks are focused on proposals that would raise considerably less.

Rangel’s 2007 plan would have added a 4 percent tax on incomes exceeding $200,000 and an extra 0.6 percent levy on those making more than $500,000. A House plan this year may include lower rates and higher income thresholds, a person familiar with the plan said.

Tax Increase

A surtax proposal would force President Barack Obama to decide whether he is willing to add the levy on top of higher income-tax rates for top earners that he wants to take effect in 2011. Obama has promised that he won’t increase taxes on Americans earning less than $250,000 and said he will delay increases for high-income earners until 2011.

Obama hasn’t commented on the possibility of a surtax, and the White House had no comment on specific proposals. The president has proposed limiting itemized deductions for high- income taxpayers.

Obama has said he doesn’t want to tax health-insurance benefits, while refusing to rule out that possibility if it helps seal approval for an overall health package.

Congressional Democrats have said they may need to raise taxes by at least half a trillion dollars to pay for the health- care revamp, in addition to savings of almost as much through steps such as reducing Medicare subsidies and cutting prices the elderly pay for medications.

‘Everything’ on Table

Matthew Beck, a spokesman for the Ways and Means Committee, declined to comment about the surtax option, saying only that “everything’s on the table.”

Michael Steel, a spokesman for House Minority Leader John Boehner of Ohio, the chamber’s top-ranking Republican, said his party would oppose a surtax because it would “disproportionately” affect small businesses, whose owners often include business income in amounts taxed on their individual returns.

“With unemployment nearing double digits, we need to help small businesses grow and create jobs, not squeeze the life out of them with even higher taxes,” Steel said.

According to the Tax Policy Center, a Washington research group, about 4.3 million of 150 million U.S. households filing tax returns will earn more than $200,000 this year.

A surtax would be levied on adjusted gross income, before deductions for items such as mortgage interest and charitable gifts. Regular income taxes are assessed after such write-offs.

Different Objectives

Eugene Steuerle, vice president of the Peter G. Peterson Foundation, a non-profit federal budget watchdog group, said the surtax and a levy on benefits reflect “very different objectives.” A surtax would make the tax code more progressive, and cutting tax incentives for employer-provided insurance is intended to discourage unnecessary use of medical services, he said.

Mark Weinberger, vice chairman of New York-based Ernst & Young LLP, said that while Republicans won’t back higher tax rates, House Democrats at this point don’t need bipartisan support.

“Strategically, what Democrats have to do is just move the ball forward,” Weinberger said. “Whatever revenue raisers they have in the House or Senate bills will change throughout the process.”

Monday, June 8, 2009

Fed's Hoenig: Inflation Is the Most "Regressive", "Corrosive" Tax

from Thomas Hoenig, President, Federal Reserve Bank of Kansas City:

"...I often emphasize that inflation is the least fair, most regressive and most corrosive tax we can impose upon ourselves. It is particularly harsh for low- to moderate-income citizens." (delivered Jun3, 2009, Sheriday, Wyoming)

Sunday, June 7, 2009

Still More Taxes and Compulsory Insurance

from Bloomberg:

President Barack Obama wants Congress to consider taxing the wealthy instead of workers to pay for a health-care overhaul, as House Democrats discuss a plan to require health insurance for most Americans.

The Obama administration stepped up efforts to influence health-care legislation today as advisers David Axelrod and Austan Goolsbee appeared on television talk shows to discuss the issue.

The president is trying to avoid broad-based levies such as a Senate proposal to tax some employer-provided health benefits Axelrod said. Instead he is urging lawmakers to reconsider limiting all tax deductions for Americans in the highest tax brackets.

“He made a very strong case for the proposal that he put on the table, which was to cap deductions for high-income Americans, and he urged them to go back and look at that,” Axelrod said on the CNN’s “State of the Union.” Goolsbee, appearing on “Fox News Sunday,” said Obama is “mindful” about how “ordinary Americans are able to foot the bills” and never proposed taxing employee benefits.

House Democrats are weighing a new proposal in response to Obama’s call for legislation to be enacted by August. An outline of the plan obtained by Bloomberg News would require Americans to have insurance with some exceptions.

Friday, June 5, 2009

State Tax Revenue Shortfalls Rising

from New York Times:

DENVER — The carnage in state budgets is getting worse, a report said Thursday, with places like Arizona being hurt by falling revenue on multiple fronts, like personal income and sales taxes. Other states are having mixed experiences, with some tax categories stable, or even rising, even as others fall off the map.

The report, by the National Conference of State Legislatures, also provided a scorecard for how well drafters of state budgets read the recession’s economic tea-leaves — and the short answer is, not very well.

Thirty-one states said estimates about personal income taxes had been overly optimistic, and 25 said that all three major tax categories — sales taxes, personal income taxes and corporate taxes — were not keeping up with projections.

Even gloomy-Gus states that saw the recession coming and low-balled their tax estimates had little room for celebration, the report said. “The handful of states that have weathered the economic decline reasonably well are starting to report adverse revenue developments,” it said. “The news is alarming.”

Wednesday, May 27, 2009

National Sales Tax Being Considered

from the Washington Post:

Note that the headline says it was "once considered unthinkable"!

With budget deficits soaring and President Obama pushing a trillion-dollar-plus expansion of health coverage, some Washington policymakers are taking a fresh look at a money-making idea long considered politically taboo: a national sales tax.

Common around the world, including in Europe, such a tax -- called a value-added tax, or VAT -- has not been seriously considered in the United States. But advocates say few other options can generate the kind of money the nation will need to avert fiscal calamity.

Deficit to Balloon -- IRS Revenue Plunges 34%

from USA Today:

Federal tax revenue plunged $138 billion, or 34%, in April vs. a year ago — the biggest April drop since 1981, a study released Tuesday by the American Institute for Economic Research says.

When the economy slumps, so does tax revenue, and this recession has been no different, says Kerry Lynch, senior fellow at the AIER and author of the study. "It illustrates how severe the recession has been."

For example, 6 million people lost jobs in the 12 months ended in April — and that means far fewer dollars from income taxes. Income tax revenue dropped 44% from a year ago.

"These are staggering numbers," Lynch says.

Big revenue losses mean that the U.S. budget deficit may be larger than predicted this year and in future years.

Tuesday, May 26, 2009

Soak-the-Rich Policies Lead to Lower Tax Revenues

from the WSJ:

Here's a two-minute drill in soak-the-rich economics:

Maryland couldn't balance its budget last year, so the state tried to close the shortfall by fleecing the wealthy. Politicians in Annapolis created a millionaire tax bracket, raising the top marginal income-tax rate to 6.25%. And because cities such as Baltimore and Bethesda also impose income taxes, the state-local tax rate can go as high as 9.45%. Governor Martin O'Malley, a dedicated class warrior, declared that these richest 0.3% of filers were "willing and able to pay their fair share." The Baltimore Sun predicted the rich would "grin and bear it."

One year later, nobody's grinning. One-third of the millionaires have disappeared from Maryland tax rolls. In 2008 roughly 3,000 million-dollar income tax returns were filed by the end of April. This year there were 2,000, which the state comptroller's office concedes is a "substantial decline." On those missing returns, the government collects 6.25% of nothing. Instead of the state coffers gaining the extra $106 million the politicians predicted, millionaires paid $100 million less in taxes than they did last year -- even at higher rates.

No doubt the majority of that loss in millionaire filings results from the recession. However, this is one reason that depending on the rich to finance government is so ill-advised: Progressive tax rates create mountains of cash during good times that vanish during recessions. For evidence, consult California, New York and New Jersey..Saturday, May 16, 2009

81% Tax Increase to Fund Entitlements

from Forbes:

This week, the federal government published two important reports on long-term budgetary trends. They both show that we are on an unsustainable path that will almost certainly result in massively higher taxes.

The first report is from the trustees of the Social Security system. News reports emphasized that the date when its trust fund will be exhausted is now four years earlier than estimated last year. But in truth, this is an utterly meaningless fact because the trust fund itself is economically meaningless.

The 2010 budget, which was finally released this week, confirms this fact. As it explains in Chapter 21, government trust funds bear no meaningful comparison to those in the private sector. Whereas the beneficiary of a private trust fund legally owns the income from it, the same is not true of a government trust fund, which is really nothing but an accounting device.

Most Americans believe that the Social Security trust fund contains a pot of money that is sitting somewhere earning interest to pay their benefits when they retire. On paper this is true; somewhere in a Treasury Department ledger there are $2.4 trillion worth of assets labeled "Social Security trust fund."

The problem is that by law 100% of these "assets" are invested in Treasury securities. Therefore, the trust fund does not have any actual resources with which to pay Social Security benefits. It's as if you wrote an IOU to yourself; no matter how large the IOU is it doesn't increase your net worth.

This fact is documented in the budget, which says on page 345: "The existence of large trust fund balances … does not, by itself, increase the government's ability to pay benefits. Put differently, these trust fund balances are assets of the program agencies and corresponding liabilities of the Treasury, netting to zero for the government as a whole."

Consequently, whether there is $2.4 trillion in the Social Security trust fund or $240 trillion has no bearing on the federal government's ability to pay benefits that have been promised. In a very technical sense, it would lose the ability to pay benefits in excess of current tax revenues once the trust fund is exhausted. But long before that date Congress would simply change the law to explicitly allow general revenues to be used to pay Social Security benefits, something it could easily do in a day.

The trust fund is better thought of as budget authority giving the federal government legal permission to use general revenues to pay Social Security benefits when current Social Security taxes are insufficient to pay current benefits--something that will happen in 2016. Effectively, general revenues will finance Social Security when the trust fund redeems its Treasury bonds for cash to pay benefits.

What really matters is not how much money is in the Social Security trust fund or when it is exhausted, but how much Social Security benefits have been promised and how much total revenue the government will need to pay them.

The answer to this question can be found on page 63 of the trustees report. It says that the payroll tax rate would have to rise 1.9% immediately and permanently to pay all the benefits that have been promised over the next 75 years for Social Security and disability insurance.

But this really understates the problem because there are many people alive today who will be drawing Social Security benefits more than 75 years from now. Economists generally believe that the appropriate way of calculating the program's long-term cost is to do so in perpetuity, adjusted for the rate of interest, something called discounting or present value.

Social Security's actuaries make such a calculation on page 64. It says that Social Security's unfunded liability in perpetuity is $17.5 trillion (treating the trust fund as meaningless). The program would need that much money today in a real trust fund outside the government earning a true return to pay for all the benefits that have been promised over and above future Social Security taxes. In effect, the capital stock of the nation would have to be $17.5 trillion larger than it is right now. Alternatively, the payroll tax rate would have to rise by 4%.

To put it another way, Social Security's unfunded liability equals 1.3% of the gross domestic product. So if we were to fund its deficit with general revenues, income taxes would have to rise by 1.3% of GDP immediately and forever. With the personal income tax raising about 10% of GDP in coming years, according to the Congressional Budget Office, this means that every taxpayer would have to pay 13% more just to make sure that all Social Security benefits currently promised will be paid.

As bad as that is, however, Social Security's problems are trivial compared to Medicare's. Its trustees also issued a report this week. On page 69 we see that just part A of that program, which pays for hospital care, has an unfunded liability of $36.4 trillion in perpetuity. The payroll tax rate would have to rise by 6.5% immediately to cover that shortfall or 2.8% of GDP forever. Thus every taxpayer would face a 28% increase in their income taxes if general revenues were used to pay future Medicare part A benefits that have been promised over and above revenues from the Medicare tax.

But this is just the beginning of Medicare's problems, because it also has two other programs: part B, which covers doctor's visits, and part D, which pays for prescription drugs.

The unfunded portion of Medicare part B is already covered by general revenues under current law. The present value of that is $37 trillion or 2.8% of GDP in perpetuity according to the trustees report (p. 111). The unfunded portion of Medicare part D, which was rammed into law by George W. Bush and a Republican Congress in 2003, is also covered by general revenues under current law and has a present value of $15.5 trillion or 1.2% of GDP forever (p. 127).

To summarize, we see that taxpayers are on the hook for Social Security and Medicare by these amounts: Social Security, 1.3% of GDP; Medicare part A, 2.8% of GDP; Medicare part B, 2.8% of GDP; and Medicare part D, 1.2% of GDP. This adds up to 8.1% of GDP. Thus federal income taxes for every taxpayer would have to rise by roughly 81% to pay all of the benefits promised by these programs under current law over and above the payroll tax.

Since many taxpayers have just paid their income taxes for 2008 they may have their federal returns close at hand. They all should look up the total amount they paid and multiply that figure by 1.81 to find out what they should be paying right now to finance Social Security and Medicare.

To put it another way, the total unfunded indebtedness of Social Security and Medicare comes to $106.4 trillion. That is how much larger the nation's capital stock would have to be today, all of it owned by the Social Security and Medicare trust funds, to generate enough income to pay all the benefits that have been promised over and above future payroll taxes. But the nation's total private net worth is only $51.5 trillion, according to the Federal Reserve. In effect, we have promised the elderly benefits equal to more than twice the nation's total wealth on top of the payroll tax.

Of course, theoretically, benefits could be cut to prevent the necessity of a massive tax increase. But how likely is that? The percentage of the population that benefits from Social Security and Medicare is growing daily as the baby boom generation ages and longevity increases. And the elderly vote in the highest percentage of any age group, so their political influence is even greater than their numbers.

The reality, which absolutely no one in either party wishes to face, is that benefits are never going to be cut enough to prevent the necessity of a massive tax increase in the not-too-distant future. Those who think otherwise are either grossly ignorant of the fiscal facts, in denial, or living in a fantasy world.

Bruce Bartlett is a former Treasury Department economist and the author of Reaganomics: Supply-Side Economics in Action and Impostor: How George W. Bush Bankrupted America and Betrayed the Reagan Legacy. He writes a weekly column for Forbes.

Subscribe to:

Comments (Atom)