Wow! This one nails it on the head!

By Charles Hugh Smith, Of Two Minds blog!

It's one or the other, Ben: you either push the real economy over the edge or you push stocks and the risk trade off the cliff.

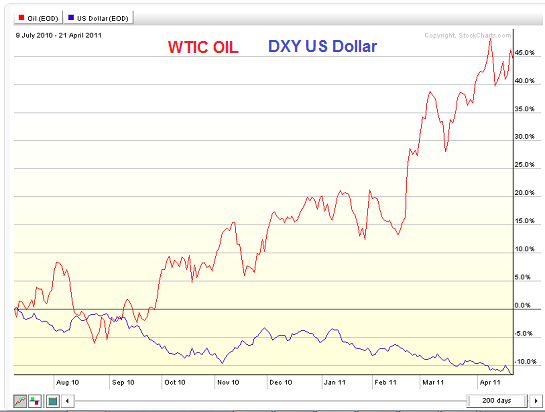

Now that you've pushed the dollar down, Ben, it's your pick on what to push off the cliff: your beloved risk trade or the real economy. Here's a chart of the U.S. dollar and crude oil. Notice they're on a see-saw: when the dollar tanks, oil skyrockets. When the dollar recovers a bit, oil declines.

Ben Bernanke and the Fed are replaying their 2008 game plan: drive the dollar down to goose the risk trade in stocks. But a funny thing happened on the way to blowing another equity bubble: oil bubbled up, too, and that killed the real economy.

For the past three years, Ben has been trying to resuscitate the real economy via "the wealth effect": if your portfolio of stocks is rising, then you'll feel richer and your "animal spirits" of borrowing and spending will be aroused. The only proven way to goose stocks is to crush the dollar so overseas corporate earnings will be boosted by the currency depreciation (when transferred back into dollars, even flat profits look like they're rising), and U.S. exports will be cheaper to our trading partners.

Flooding the U.S. market with liquidity and keeping interest rates at zero had another consequence, one adamantly denied by the Ministry of Truth: it sparked a carry trade in which cheap dollars could be borrowed for next to nothing and exported around the world to seek higher returns.

Unsurprisingly, much of this free money flowed into commodities, which retained their value as the Fed pushed the dollar down. Also unsurprisingly, oil exporters raised the price of their oil in dollars as the dollar tanked.

Ben and his motley crew at the Fed reckoned that the financialized U.S. economy would respond positively to the lower dollar and the goosing of the risk trade in stocks. But the guys and gals seem to have forgotten that the real economy is dependent on oil. All the folks at the cocktail parties attended by Yellen et al. may be gushing over their hefty stock gains, but in the kitchen and carpark the workers are grousing about the rising prices of food and gasoline.

Now the cost of oil--the lifeblood of the real economy--is close to the point that it will push the real economy into recession. This sets up a difficult choice for Ben: if he pushes the dollar down to new lows, then oil leaps up and pushes the real economy off the cliff.

Alternatively, Ben renounces QE3 and "surprises" the markets with a rate increase, thus rescuing the dollar from freefall and pushing oil down. But that will send his precious risk trade and equity Bull off the cliff.

The politicos won't like either choice, but sacrificing the real economy will cost them their seat. All the fatcats who've raked in tens of billions from the risk trade Bull will be demanding that Ben "save" the financialized economy, but the politicos will see their political obituaries being written. Yes, the fatcats will shower them with millions in campaign contributions, but even those millions won't change the fact that Americans reliably vote their pocketbooks.

If rising oil pushes the real economy over the cliff, voters will not be re-electing incumbents in 2012.

Welcome to reality, Ben. Your "let's pretend the recovery is real" game is nearing an end. If you push the dollar down any more, then oil will go up and tip the real economy into a recession that QE3 will only make worse as you send the dollar into freefall. If the dollar rises, then your beloved "wealth effect" dies a horrible death on the rocks below.

Take your pick, but choose wisely.

President Barack Obama’s budget speech was delivered at George Washington University Law School on April 13, 2011. What is most notable about the speech was not the predictable and partisan reaction to it. Rather, it was the president’s deft use of rhetorical tropes to pull off his increasingly transparent maneuver of talking right while moving left.

As is par for the course, the speech contains enough platitudes to make it appear that the president is a fair-minded man—a man who understands the difficult trade-offs that must be made in order to balance the imperatives of market growth with the just provision of government resources to all individuals. In the end, however, this presidential straddle will fall to ruins because of its implicit assumption that transfer payments will do no harm to total production, even as they redress the inequality of fortunes in this country. Not so. But rather than jump ahead in the story, it is best to track Obama’s argument as if it were an exercise not of partisan politics, but of political theory.

Illustration by Barbara Kelley

Without a doubt, this point has some real power. The provision of classical sorts of public goods—police protection, sanitation, public highways and infrastructure —often requires government support. There is, for example, no way that the government can provide protection against foreign aggression for some individuals unless it provides that protection for all. The nonexclusive nature of classical public goods means that the nation can no longer rely on the voluntary coordination of individuals, or even of states, to deliver these services. What’s more, the government must impose national taxes to overcome this failure.

Levy taxes in ways that mimic market transactions.

Ideally, we would like to levy these taxes in ways that mimic market transactions. In other words, we hope that these taxes will, to the extent that human institutions can make it happen, provide each person with benefits that he or she values more than the taxes paid to fund them. Indeed, the distinctive feature of classical liberalism is that it defends this generalized use of state coercion only when this condition is satisfied. It is the set of return benefits to the parties who are taxed that prevents taxation from becoming a massive taking from A to B through state intervention.Obama neither mentions nor rejects these limitations on the public good arguments. Instead, he skillfully turns this classical liberal argument to deeply collectivist ends. The president’s broad conception of public goods quickly gives way to the wholly different image of all Americans as part of one giant family—with the attendant obligations of reciprocal support. "Part of this American belief that we are all connected also expresses itself in a conviction that each one of us deserves some basic measure of security."

At this point, ambiguity in the idea of "security" turns the social contract theory of John Locke and David Hume on its head. By Locke and Hume’s conception, every person was required to renounce force in order to increase his own security from the aggression of other individuals. It is hard to think that anyone, no matter how powerful, is left worse off by this one trade-off.

Under Obama’s more aggressive agenda, however, security includes "Social Security" so that each person has to undertake to support his fellow citizens who are not able to support themselves, even if unthreatened by others. Put otherwise, no longer is a successful individual just under a duty not to take advantage of the less fortunate by use of force and fraud; now that duty extends to supplying financial support to all individuals against the vicissitudes of life—without offering any explanation as to why they are unable to undertake that task for themselves.

By this point in the speech, the opening riff on free markets is a distant and shadowy object in the rearview mirror. Later in his speech, all of Obama’s focus is on the exceptions to free markets, rather than its benefits.

On the matter of taxes, the president said: "As a country that values fairness, wealthier individuals have traditionally born a greater share of this burden than the middle class or those less fortunate." That statement is, of course, as true of a flat tax on income as it is of a progressive tax. But at no point does Obama point out the difference between them or explain why a progressive tax is the better way to handle the inequities that arise as he perceives them.

So now we have a new villain, which is the undeserved tax cuts "that went to every millionaire and billionaire in the country" and which drive the current deficits. On his cramped view of economics, these revenues were well spent on "a series of emergency steps that saved millions of jobs, kept credit flowing, and provided working families extra money in their pockets."

If income redistribution is the be-all and end-all of all politics, why not simply adopt a policy of equal incomes? That's a question Obama left unanswered.

It is here that Obama’s argument runs into fatal complications. The first is his untested assertion that his emergency steps and stimulus programs actually kept the economic ship afloat in stormy seas. But the more accurate account is that the high tax levels reduced the type of initiatives that only private investments of capital can yield. The government expenditures on what Obama formerly (and falsely) referred to as "shovel-ready" projects only produce short-term bubbles that do more to block growth than to create it. Unemployment rates remain high, growth rates remain low, and budget deficits double because the president now thinks that income redistribution is the be-all and end-all of all politics.Here is what he said on this matter:

The top 1% saw their income rise by an average of more than a quarter of a million dollars each. And that’s who needs to pay less taxes? They want to give people like me a two hundred thousand dollar tax cut that’s paid for by asking thirty three seniors to each pay six thousand dollars more in health costs? That’s not right, and it’s not going to happen as long as I’m President.At this point, the implicit assumption is that all government intervention is a zero-sum game, where the losses in dollars on the one side (taxes) are precisely offset by the gains in dollars on the other (social services). Since—and this is a true assumption—the utility of money is, in general, higher in the hands of the poor than the rich, 30 individuals should have their health care benefits extended and the rich should be denied their tax cuts.

Yet, this is a game that can be played countless times no matter how steep the current tax rate structure is. Indeed, it could be played even if the rich pay a larger fraction of the overall tax bill when taxes fall, which could well happen if their incomes increase in response to any new tax cuts. Under the president’s vision, however, no matter how high the marginal taxes on the rich, they could always be raised. After all, if we squeeze the lemon a bit drier, we can fund health care benefits for even more people. President Obama is incapable of asking candidly whether high taxation can ever reduce the level of output. In his world, the efforts of the rich and of the poor remain constant, regardless of the return guaranteed to labor.

Hence, no matter what the current marginal tax rates, it is perfectly all right to push them higher. There is never a case where productive losses exceed distributive gains. In the end, the president offers no good reason why this nation should not adopt a tax structure that drives it to a policy of equal incomes.

But really, can this be so? The president never bothers to mention that as of today, the top 1 percent earns about 20 percent of the wealth but pays close to 40 percent of the taxes. Does he really believe that there would be no wealth distribution from rich to poor under a flat tax, given that a huge fraction of public revenues goes to a range of transfer programs from which the rich derive little or no benefit? Nor does he ever contemplate the possibility that lower tax rates could generate additional revenues for the entire system.

And why does the president take this view taxation and income policy? Because, at root, the president is an egalitarian, not a marketeer. He has no theory of what a system of optimal taxation would look like. To lawyers and economists in the classical liberal tradition, it is a good thing, not a bad thing, if the richest person in society gets richer—so long as no one else is made poorer. But to the committed egalitarian, that supposed social improvement in fact poses a real threat because it increases the amount of inequality of wealth in society.

So the president blissfully advocates programs that reduce overall social wealth in order to soften these wealth differences. But it’s a mug’s game. In the end, it is growth, and only growth, that can cure the national malaise. And that means letting the rich get richer so that they can bring the rest of us along with them. But just as King Canute could not stop the tides, so it is that President Obama cannot draw blood out of a stone. What the president thinks are zero-sum policies are in fact no such thing. Given how they distort market incentives and increase political strife, Obama’s progressive policies translate into a profoundly negative-sum game, which, when replicated over time, will strip this nation of the entrepreneurial spirit that accounted for its past greatness.

Richard Epstein is the Peter and Kirsten Bedford Senior Fellow at Hoover. He is also the Laurence A. Tisch Professor of Law at New York University. His areas of expertise include constitutional law, intellectual property, and property rights. His most recent books are The Case Against the Employee Free Choice Act (Hoover Press, 2009) and Supreme Neglect: How to Revive the Constitutional Protection for Private Property (Oxford Press, 2008).