Between ECB head Draghi's comments and the endless money-printing by the Fed, no one dares short the market, even though the economic news is lackluster. We just keep buying the dips!

Between ECB head Draghi's comments and the endless money-printing by the Fed, no one dares short the market, even though the economic news is lackluster. We just keep buying the dips!

About as expected! However, the trend appears to have turned modestly lower, since this is the fourth week in a row that claims have been higher than expected.

from Zero Hedge:

Initial claims came, saw and missed for the

4th week in a row, printing at 371K, on expectations of a decline from

372K to 365K. As happens at the end of every year when employers turn

on the pink sheet machine, the not seasonally adjusted number soared

from 490K to 552K in the week ending January 5, a difference to the

seasonally adjusted print of 181K. This is to be expected. What was

unexpected is that the last week print saw its first downward adjustment

in what seems years (it actually is years), with the December 29 week

claims number declining from 372K to 367K, probably as a result of all

the year end guessing that goes on to assist the other guessing that

goes into the seasonal adjustment guessing.

What a surprise! Despite that stocks were rising sharply this morning, reaching what appears to be a fresh five-year high for stocks, a revised Philly Fed survey shocked the financial markets back to reality. This is just one indicator, so it is likely it will once again be shrugged off as anecdotal, despite that there is a growing trend toward more economic ennui and slower global activity.

Today's chart thus far:

We haven't hit bottom yet for today, but the news will be shrugged off by traders on Wall St as irrelevant to the U.S. markets.

Even under the most optimistic assumptions, taxes on the rich will still not cover a large fraction of the costs of a European-style welfare state.To be in our political center today, you have to deny both these truths and pretend that if we sharpen our pencils and make a bunch of wildly optimistic assumptions, we can close a few tax loopholes, cut some waste from spending, and maybe nudge upper-income tax rates up a little, and continue merrily on the same big-and-growing-bigger government path without unfortunate consequences. This is a “balanced approach,” as it ignores both mathematical truths equally, but the denial of clear reality means this approach is doomed to fail.

What we cannot have is the Life of Julia at no additional burden to 99 out of 100 of us.In a similar vein, Jared Bernstein, a senior fellow at the Center on Budget and Policy Priorities and a former economist for Vice President Biden, writes, "It's perfectly reasonable for the White House to begin collecting more revenue from folks who have done by far the best in pretax terms." But wait a moment for it — he then adds, "But ultimately we can't raise the revenue we need only on the top 2 percent."

Surprisingly, many progressive pundits are moving away from their traditional complaint that America’s tax code is too regressive, favoring the rich.So what happens if we continue down the current path, with perhaps some small amount of revenue raised from some additional taxes on the rich? Remember, the only way to finance a big European-style state is to have it paid for by massive taxation of everyone, mostly the middle class. Right now we are avoiding honest debate on this fact, perhaps because those desirous of this change know the middle class would rebel if it saw the future bill it will have to pay. Instead, large government benefits are being continued and increased, and still new ones introduced, with little accurate discussion of who will ultimately pay.

As Congress and the President wallow in finger pointing and fiscal

gridlock, Federal Reserve Chairman Ben Bernanke plows ahead with his

plan to disguise the country's economic ills by carpet-bombing us with

freshly printed money. Aided and abetted by the gnomes in the Bureau of

Labor Statistics -- who are doing their best to convince us that

inflation remains at historic lows -- Ben has promised to conjure up $1 trillion a year out of thin air until unemployment returns to a politically acceptable 6.5 percent.

Where is all that new fiat currency going, and why haven't we seen it

show up in double digit inflation? The answer should frighten you.

The narrative being promoted in Washington is that Helicopter Ben's

money is being loaned to businesses so they can expand and hire more

people. Oh yeah, and it's also supposed to finance cut-rate mortgages to

help stabilize the housing market. Achieving both of these goals will

supposedly goose up "aggregate demand," the magic elixir that

purportedly makes economies grow. Mainstream journalists, who blithely

call a reduction in the rate of growth of government spending a "budget

cut," dutifully parrot the party line.

It's a great story except for one problem: There is no evidence it is true.

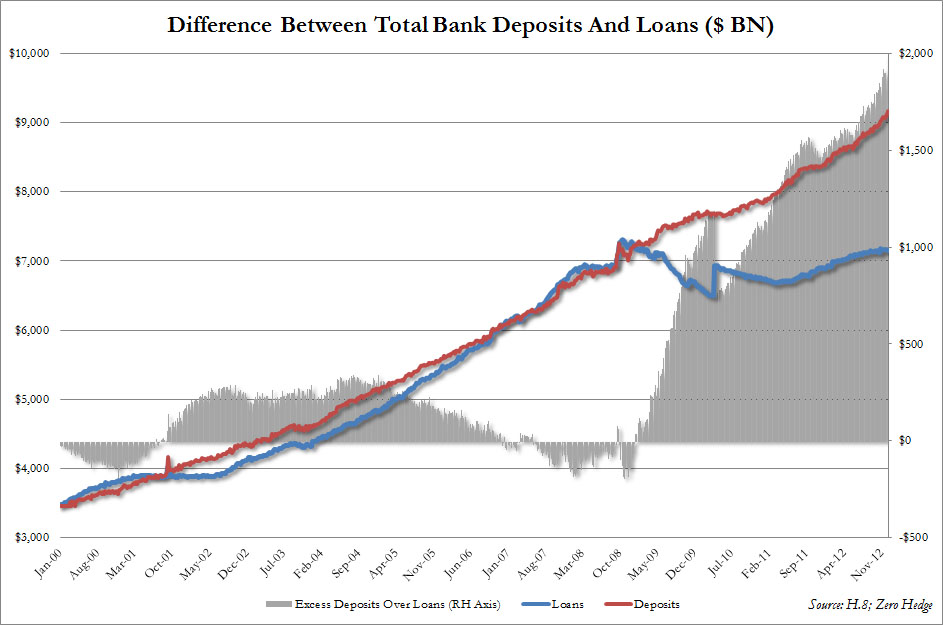

According to the astute number crunchers at Zero Hedge, total issuance of commercial loans since September of 2008 has gone down

by $120 billion. Think about it -- who wants to lend money when the

government artificially sets inflation-adjusted interest rates below

zero? Spend two minutes in the real world and you can see the

consequences for yourself. At a recent meeting between a local banker

and a client of mine the banker complained that, "There are now 10

pecker-checkers for every pecker in the loan department!" Compliance

paperwork has become so burdensome, and risk aversion so high, that only

corporations that don't need loans can get them. As a result, small

businesses, the classic engine for job growth, go begging while Fortune

500 companies park record levels of cash on the sidelines.

Yes, mortgage rates have hit rock bottom. But underwriting standards

have gone through the roof. My wife and I -- she's a doctor; I'm a

venture capitalist -- recently refinanced the mortgage on our condo. It

took three months to get approval, despite the fact that the loan

amount was for less than 30 percent of the condo's appraised value and

we have perfect credit scores and no other debt -- and this only after

we provided every bit of documentation short of proctology exams. What

chance does a first-time home buyer have in a market like this?

So, where is Ben's money actually going? The data show that it is

being stuffed onto the balance sheets of the Too-Big-To-Fail (TBTF)

banks, some of which only became "banks" overnight when their brokerage

businesses faced imminent collapse. Recapitalizing these "banks" after

their housing market malinvestments and the crash of their derivatives

casino -- the inevitable outcome of Alan Greenspan's money printing to

fuel Fannie Mae's doomsday machine -- has been the principal goal of

both the Bush and Obama administrations.

With the boundaries between Goldman Sachs, Treasury, the Fed and the

administration virtually disappearing; the big banks' Democratic and

Republican handmaidens running interference; and the media distracted

while pursuing pissant stories about debit card fees, consumer

protection rules, and shareholder gadfly proxy access; all is hunky dory

in TBTF land.

But what happens to all that freshly printed money after it gets

parked on bank balance sheets if it's not loaned to businesses and

consumers? Perhaps we could sleep at night if it just sat there, as a

cushion against the recession that lies ahead. But unfortunately, the

"banks" appear to have flocked back to the derivatives casino, confident

that as officially recognized TBTF institutions they are free to

privatize gains, gorging on bonuses while the sun shines, knowing they

can socialize their inevitable losses.

To see how much of your money they are playing with, take a look at the scariest economic chart of 2012.