Saturday, August 28, 2010

Must Double Taxes Overnight to Prevent DIsaster

In our attempts to simplify the comprehension of the ongoing serfdomization of the US population, we would like to present one of the more persuasive charts which the administration would likely be loath to demonstrate. Having collated monthly data from the FMS' Daily Treasury Statement on incremental tax revenues (individual, gross), and new debt issuance, we observe the following rather surprising pattern: since September 2008, or the month when capitalism collapsed, and the Fed, and ever other global Central Bank had to step in as a backstop of last recourse to the western way of life, the US government has undertaken the most peculiar matching program: simply said, for every dollar of individual tax revenue, the government has issued just over one dollar of incremental debt. In other words, in the past two years, tax revenues alone would have proven insufficient by over half to fill the budget gap. In yet other words, the US Treasury is now the functional equivalent of the entire US population and then some, when it comes to keeping the US economy afloat. From another perspective, with an average take down of roughly 50% of each recent auction by Indirect bidders, nearly a quarter (half of half) of US budget deficit needs is funded directly by foreigners. Should (in)formal trade wars escalate, and should the US see an embargo of foreign debt participation, then overnight a quarter of US spending will be unfundable: this includes such critical key expenditures as defense and social security spending. Also, it is important to recall, that of the $3.35 trillion in debt issued over the prior two year period, the Fed has directly (via UST purchases) and indirectly (via MBS purchases, and thus the forced rotation of MBS securities into UST securities for agency holders such as PIMCO) purchased the other half. Thus between foreigners, and the Fed, the US consumer's traditional contribution to funding the US economy has been diluted by half. And unfortunately, as the chart below shows, absent some dramatic deux ex machina, there is no chance this trend in which US debt issuance is the functional equivalent of taxpayer contributions, will ever end.

Another way of visualizing the incremental substitution of the US consumer with debt:

Some technical details:

- Total net debt issued since September 2008: $3,351 billion (from $10.025TR to $13.376TR)

- Gross tax receipts since September 2008: $3,185 billion. Note this is not net of refunds. Should one exclude the $660 billion in refunds issued over the same period, the net contribution by taxpayers is just over $2.5 trillion, meaning that the value of each dollar of debt issued is a quarter greater than each dollar in taxpayer revenues.

- This number would be somewhat offset by Corporate tax revenues, which over the same period amount to $440 billion gross and $230 billion net of corporate tax refunds.

(this analysis completely ignores the toxic debt spiral should interest rates ever increase in the future; Zero Hedge has previously discussed the liquidity horizon to default in various scenarios should prevailing debt interest rates beging to rise. And with average outstanding debt duration slowly but surely increasing, the second the Fed loses hold of Mid and Long-Term interest rates, it is all over - in other words QE will be a necessary staple until such time as the Fed is prepared to go the repudiation/hyperinflation route).

P.S., and a scary thought, if representation is somewhat equivalent to taxation, or, its modern equivalent, deficit funding, does this mean that the seven Fed Board Members have a greater right of representation than all of American society combined? It sure seems that way.

Friday, August 27, 2010

Quantitative Easing Must, Of Necessity, Lead to Dollar Collapse

A week ago, the Federal Reserve initiated a new program of "quantitative easing" (QE), with the Fed purchasing U.S. Treasury securities and paying for those securities by creating billions of dollars in new monetary base. Treasury bond prices surged on the action. With the U.S. economy predictably weakening, this second round of quantitative easing appears likely to continue. Unfortunately, the unintended side effect of this policy shift is likely to be an abrupt collapse in the foreign exchange value of the U.S. dollar.

How exchange rates are determined - a primer

To understand how currencies fluctuate, it's helpful to understand two forms of "parity" that operate in the foreign exchange markets.

1) Purchasing Power Parity (PPP): This describes the tendency for long-term exchange rate movements to reflect long-term changes in relative price levels between countries. Suppose for simplicity that a given basket of goods costs $10 in the U.S., and costs FC40 in some other country (where FC is simply a unit of foreign currency). If the goods are identical and can be transported costlessly without any barriers, one would expect that $10 = FC40, or that $1 = FC4. So the exchange rate would satisfy purchasing power parity if one dollar traded for 4 units of foreign currency.

Suppose the foreign country is highly inflationary, so that the price of that basket of goods increases to FC60, while the U.S. experiences no corresponding inflation. PPP suggests that the exchange rate should track the relative price levels between the two countries, resulting in a new exchange rate of $1 = FC6. This would be a "strengthening" or "appreciation" in the dollar, since each dollar would command a greater amount of foreign currency. Conversely, this would be a "weakening" or "depreciation" in the foreign currency, since each unit of FC would command fewer dollars.

More generally, goods and services are not identical across countries and cannot be moved costlessly, so PPP is only a long-term tendency, and is not enforced at every point in time. Still, there is a strong tendency for exchange rate movements, in the long run, to reflect relative inflation rates of inflation between countries. Countries with high rates of inflation tend to depreciate over time, relative to countries with lower rates of inflation, and this depreciation is in nearly direct proportion to the relative changes in price levels (particularly when one uses price indices of tradeable goods).

2) Interest Rate Parity: This describes the tendency for exchange rates to move in a way that offsets expected differences in interest rate returns. Suppose that interest rates in the U.S. are 2%, and interest rates in the foreign country are 5%. If the exchange rate was expected to remain perfectly constant, and there were no barriers to capital movements, investors would have a strong tendency to buy the foreign currency in order to earn the higher interest rate. Of course, the exchange rate would not remain constant, as investors would tend to bid up the foreign currency. In fact, there would be a tendency to bid up the foreign currency until it was sufficiently elevated today that a 3% annual depreciation would be expected in the future. At that point investors would be indifferent, since the 2% interest rate available in the U.S. would be equivalent to the 5% interest - 3% depreciation expected in the foreign currency. From a foreigners perspective, the 5% interest rate available in that country would be equivalent to the 2% interest + 3% appreciation expected in the U.S. dollar.

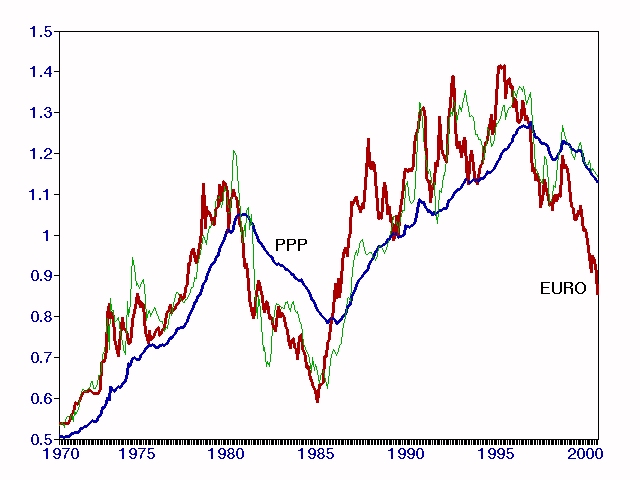

The key idea is that purchasing power parity holds in the long-run in order to align the prices of internationally traded goods and services, while interest rate parity tends to maintain shorter-term equilibrium in the capital markets. Both are important determinants of currency fluctuations because currencies are both a means of payment and a store of value. You can find a practical example of how PPP and interest rate parity combine to determine exchange rates in Valuing Foreign Currencies, published in September 2000. At the time, I argued that the euro, then at $0.85, was deeply undervalued - and included the following chart. The volatile red line is the $/euro exchange rate (data for the German mark is used prior to 1999), the blue line is PPP, and the thin line is our calculation of the value of the euro implied by interest rates as well as price levels.

Since inflation rates as well as nominal interest rates are important in determining exchange rates, one would expect that real, after-inflation rates are also important. Indeed, this is true - and with a little bit of algebra, one can show that a currency should deviate PPP by an amount that reflects the difference in real interest rates expected between the two countries over time. Currencies with relatively high real interest rates will tend to trade well above PPP, while currencies with low or negative real interest rates will tend to trade below their PPP values.

Why quantitative easing is likely to trigger a collapse of the U.S. dollar

Consider a situation in which there is zero anticipated inflation in both the U.S. and in a given foreign country. In this situation, PPP implies a flat long-term profile for exchange rates, because there is no pressure in the goods market for currency values to change over time. Meanwhile, suppose that interest rates (say, on 10-year government notes) in the U.S. and the foreign country are both at 4%. In this situation, an investor in the U.S. expects a 4% return from domestic Treasury notes, and with no expected currency appreciation, also expects a 4% return from investing in the foreign country. In this situation, both PPP and interest rate parity can be satisfied with an exchange rate that simply remains constant.

In contrast, quantitative easing can be expected to create a remarkably different situation. The Fed's purchase of Treasury securities and creation of base money is occurring in an environment where fiscal deficits are already out of control, while two-thirds of the Fed's balance sheet already represents Fannie and Freddie Mac securities that need to be bailed out by the Treasury. This makes it enormously difficult to reverse the Fed's transactions - because the Fed is not simply determining whether a given stock of government liabilities will take the form of Treasury bonds or currency. It is instead effectively printing new money to finance ongoing spending for fiscal deficits and the bailout of the GSEs. At the same time, the fact that it is operating in a weak economy and a near-term deflationary environment means that nominal interest rates are being pressed down at the same time that long-term inflationary prospects are escalating.

From the standpoint of the two parity conditions, the very long-term implication of quantitative easing is a gradual devaluation of the U.S. dollar (an increase in the dollar price $/FC of foreign currency). If this increased inflation risk was reflected in interest rates (so that real interest rates were held constant), the U.S. dollar would simply move along that gradually sloped PPP line, and likewise, foreign currencies would gradually appreciate against the dollar.

However, because of economic weakness and credit strains, coupled with the demand for Treasuries by the Fed, quantitative easing instead moves U.S. interest rates in the opposite direction, falling rather than rising. From the standpoint of interest rate parity, capital market equilibrium then requires the U.S. dollar to depreciate immediately, by a sufficient amount to set up the expectation of future appreciation in order to offset the shortfall of U.S. interest rate returns.

In short, quantitative easing is likely to induce what the late MIT economist Rudiger Dornbusch described as "exchange rate overshooting" - a large and abrupt shift in the spot exchange rate that occurs in order to align long-term equilibrium in the market for goods and services with short-term equilibrium in the capital markets.

This adjustment is depicted in the diagram below. In response to the monetary shock, a modest but long-term depreciation in the dollar (a rise in the U.S. dollar price of foreign currency) is required, depicted by the blue line. However, since nominal interest rates in the U.S. actually decline, ongoing equilibrium in the capital market requires that the U.S. dollar must be expected to appreciate over time by enough to offset the lost interest. As a result, quantitative easing is likely to result in an abrupt "jump depreciation" of the U.S. dollar (that is, a spike in the value of foreign currencies).

Frankly, I've always thought Dornbush's use of the word "overshooting" was unfortunate, because it implies that the exchange rate move is an overreaction, when that is not at all the case. Overshooting refers to the tendency of the spot exchange rate to move beyond its long-term PPP value, but this move is in fact approprate, efficient, and required in order to align the returns that investors can expect in each currency. So it is important to avoid misinterpretation - the policy of quantitative easing is likely to force a large adjustment on the U.S. dollar because the Federal Reserve is choosing to lay a heavier hand on the Treasury bond market than would result from economic conditions alone. The resulting shift in interest rates and long-term inflation prospects combine to dramatically reduce the attractiveness of the U.S. dollar. A significant and relatively abrupt devaluation is then required, in an amount sufficient to set up expectations of a U.S. dollar appreciation over time.

Just to avoid misinterpretation, I am not suggesting that there is a near-term risk of inflation, nor am I suggesting that quantitative easing is inflationary per se. The primary driver of long-term inflation pressure has always been, and continues to be, growth in the total quantity of government liabilities (both monetary base and government debt) for purposes that do not expand the productive capacity of the economy. This total quantity is determined by fiscal policy, and the form of those liabilities hardly matters because currency and government debt are close substitutes in the portfolios of individuals. So the argument here is not that quantitative easing will create inflation which will hurt the dollar. The argument is more subtle. It is that we are running a fiscal policy that is long run (though not short-run) inflationary, and that the monetary policy of quantitative easing prevents longer term interest rates from acting as an adjustment variable, since the Fed is essentially announcing that it will lean on the Treasury bond market. By suppressing Treasury yields, the Fed forces the exchange rate to bear the full weight of the adjustment.

Importantly, the Fed's policy need not suppress real interest rates by more than a percent or two to create dramatic pressure on the dollar. One way to think about the price jump required by exchange rate overshooting is to think about a long-term bond. If a 10-year zero-coupon bond with a $100 face is priced to deliver 0% annually, it will have a price of $100. If investors suddenly demand the bond to be priced to deliver 2% annually, the bond must experience an immediate drop in price to $82. Once that price drop occurs, the selling pressure on the bond will abate, since it will now be expected to appreciate at a 2% annual rate.

My impression is that Ben Bernanke has little sense of the damage he is about to provoke. A central banker who talks about throwing money from helicopters is not only arrogant but foolish. Nearly a century ago, the great economist Ludwig von Mises observed that massive central bank easing is invariably a form of cowardice that attempts to avoid the need to restructure debt or correct fiscal deficits, avoiding wiser but more difficult choices by instead destroying the value of the currency.

Von Mises wrote, "A government always finds itself obliged to resort to inflationary measures when it cannot negotiate loans and dare not levy taxes, because it has reason to fear that it will forfeit approval of the policy it is following if it reveals too soon the financial and general economic consequences of that policy. Thus inflation becomes the most important psychological resource of any economic policy whose consequences have to be concealed; and so in this sense it can be called an instrument of unpopular, that is, of antidemocratic policy, since by misleading public opinion it makes possible the continued existence of a system of government that would have no hope of the consent of the people if the circumstances were clearly laid before them. That is the political function of inflation. When governments do not think it necessary to accommodate their expenditure and arrogate to themselves the right of making up the deficit by issuing notes, their ideology is merely a disguised absolutism."

As a side note, von Mises also cautioned against the misconception that destroying the value of a currency would have a sustainable benefit for the economy, writing "If the depreciation is desired in order to 'stimulate production' and to make exportation easier and importation more difficult in relation to other countries, then it must be borne in mind that the 'beneficial effects' on trade of the depreciation of money only last so long as the depreciation has not affected all commodities and services. Once the adjustment is completed, then these 'beneficial effects' disappear. If it is desired to retain them permanently, continual resort must be had to fresh diminutions of the purchasing power of money."

Market Climate

As of last week, the Market Climate for stocks was characterized by unfavorable valuations, unfavorable market action, and unfavorable economic pressures. I've noted for weeks that the damage to market action was not quite to the level that would create urgent downside concerns. However, the deterioration we observed last week suggests a more urgent shift to defensive positioning. For our part, the Strategic Growth Fund remains fully hedged at present.

In bonds, the Market Climate was characterized last week by unfavorable yield levels but favorable yield pressures. Treasury securities have advanced sharply on the initial quantitative easing purchases by the Fed. Meanwhile, the jump in unemployment claims to 500,000 and the surprising drop in the Philadelphia Fed index are both consistent with the weakening economic conditions that are clearly implied by leading measures. If anything, those deteriorations appear to be early, not late-stage observations. As I've noted regularly in recent commentaries, normal lead-times would suggest a deterioration in the ISM Purchasing Managers Index in the August-September data, while new claims for unemployment typically have an even longer lag, which would normally make us expect strains closer to October. Suffice it to say that the much earlier deterioration in economic measures is not encouraging, but it also opens up the possibility that we may see some misleading "improvement" in the data in the next few weeks before we get into the more typical window of deterioration.

As one might infer from the content of this week's remarks, my view is that the quick initiation of quantitative easing by the Federal Reserve has significantly changed the prospects for foreign currencies and by extension, precious metals. For the past couple of months, I've observed that deflation risks in response to fresh economic weakness were likely to provoke weakness in the commodity area, even if long-term inflationary concerns were accurate. However, my impression is that the Fed's immediate initiation of quantitative easing may cause investors to take deflation concerns "off the table." This is important, because even as we observe economic deterioration, the potential for a "deflationary scare" is likely to be more muted than we might have expected without explicit quantitative easing actions.

This doesn't entirely remove those risks, of course, particularly if we begin to observe a spike in credit spreads (which would be associated with default concerns and a likely drop in monetary velocity), but it clearly changes the environment. Gold stocks and the XAU have essentially gone nowhere since May. Last week, in response to a favorable shift in the Market Climate for precious metals and currencies (largely resulting from the shift in Fed policy and interest rates), we increased our exposure to precious metals in the Strategic Total Return Fund toward 10% of assets, and raised our exposure to foreign currencies to about 5% of assets. This is still not an aggressive stance, and we would prefer the opportunity to accumulate a larger exposure on substantial price weakness, if it occurs. But as this week's comment makes clear, the Federal Reserve has begun to play with fire, the effects of which I doubt Bernanke fully appreciates.

Good policy is not rocket science. It begins with the refusal to make people pay for mistakes that are not their own. This economy continues to struggle with a fundamental problem, which is that debt obligations exceed the ability to service them. While policy makers have done everything to preserve the patterns of spending and consumption that created the problem in the first place, we have done nothing to restructure those obligations.

To the extent that we observe fresh credit problems, we should not pursue the same policies. Instead, we should focus on restructuring debt. Let the bank bondholders fail, and defend depositors and customers through the standard procedures that the FDIC has followed for decades. Deal with the debt of Fannie Mae and Freddie Mac by asserting that there is no explicit government guarantee, and let the holders of the mortgage pools receive precisely what they are entitled to receive without public funds. At the same time, expand the role of the FHA to provide explicit government guarantees for future mortgages in return for actuarily fair risk-based premiums, and require mortgage originators to retain a piece of the mortgage loan, along with appropriate capital requirements, and the stipulation that this retained portion bears the first loss if the mortgage goes bad. Finally, refuse to trot self-interested bank and Wall Street executives in front of the public to extort the nation through fear of the word "failure." Banks fail all the time and customers don't lose a cent. The only implication of failure is that stock and bondholders of reckless institutions aren't rewarded for their malinvestment at public expense.

Chairman of Joint Chiefs: #1 Threat to National Seecurity is Nation's Debt

The national debt is the single biggest threat to national security, according to Adm. Mike Mullen, chairman of the Joint Chiefs of Staff. Tax payers will be paying around $600 billion in interest on the national debt by 2012, the chairman told students and local leaders in Detroit.

“That’s one year’s worth of defense budget,” he said, adding that the Pentagon needs to cut back on spending.

“We’re going to have to do that if it’s going to survive at all,” Mullen said, “and do it in a way that is predictable.”

He also called on the defense industry to hire veterans and become more robust in the future.

“I need the defense industry, in particular, to be robust,” he said. “My procurement budget is over $100 billion, [and] I need to be able to leverage that as much as possible with those [companies] who reach out [to veterans].”

Mullen highlighted the unity of purpose between the government and industry as well, in working to solve national security issues.

“I have found that universally, [private-sector workers] care every bit as much about our country, are every bit as patriotic and wanting to make a difference … as those who wear the uniform and are in harm’s way,” he said.

ECRI Continues to Signal Recession

The ECRI Weekly came in at an annualized -9.9%, once again straddling the critical -10% boundary. Of course with two previous downward revisions, it appears the index' creators have taken up the government's favorite data fudging ploy of downward revising prior data, as the past week's -10% now ends up being -10.1%. No doubt next week this week's -9.9% will be revised to a worse number. But by then all the beneficial impact of the better number will be long forgotten.

Univ of Michigan Consumer Sentiment Disappoints

Slightly lower than expected reading of 68.9 vs. 69.6 expected.

The Bernanke Put

"The Federal Open Market Committee will strongly resist deviations from price stability in the downward direction," Bernanke said in a speech opening the Fed's annual summer policy retreat.

Bernanke downplayed concern that the economy would fall back into another downturn, or a double-dip recession.

He said the economy would continue to grow at a slow pace in the last four months of the year and the pace of growth would pick-up in 2011. See related story on second-quarter growth.

Bernanke said there was only a low risk of deflation. But he acknowledged that inflation has dropped to a level slightly below that which FOMC participants view "as most conducive to a healthy economy in the long run."

But he spoke at length about the tools left in his toolkit to fight deflation and promised to use them if the outlook deteriorated significantly.

Responding almost directly to an op-ed published Thursday by ex-Fed vice chairman Alan Blinder saying the Fed was running low on ammo, Bernanke said: "The issue at this stage is not whether we have the tools to help support economic activity and guard against disinflation. We do. As I will discuss next, the issue is instead whether, at any given juncture, the benefits of each tool, in terms of additional stimulus, outweigh the associated costs or risks of using the tool."

At the top of his list of options -- more purchases of Treasurys by the Fed. Bernanke said these purchases would ease financial market conditions.

He said the central bankers thought that buying Treasurys was the proper course of action but noted "we do not rule out changing the reinvestment strategy if circumstances warrant."

Prior to the speech, economists were hoping that Bernanke would spell out the criteria for further extraordinary policy moves. Bernanke's helicopter could move to new altitude

Bernanke said the FOMC "has not agreed on specific criteria or triggers for further action."

In early August, the Federal Open Market Committee took a baby step toward further quantitative easing by deciding to hold the size of the Fed's balance sheet constant through reinvesting principal repayments from mortgage securities into Treasurys

A slowing economy has caused the Fed to swiftly reconsider its policy stance - shifting away from an exit strategy towards consideration of further easing.

The economy is slowing at a time when the Fed has already cut interest rates to close to zero. Since March 2009, the Fed has promised to keep rates low for an "extended period."

Bernanke said the FOMC would consider modifying the language to communicate to investors that it plans to keep the federal funds rate low for a longer period than is currently priced in markets.

He also said the Fed could lower the rate of interest the Fed pays banks on the reserves they park at the central bank, though he stressed that the effect in isolation would likely be relatively small.

One policy option Bernanke rebuffed was to increase medium-term inflation goals above levels consistent with price stability. "I see no support for this option on the FOMC," the central bank chief said.

Bernanke Punts!

He vowed strong resistance. Whatever it takes! This is NOT a good sign!

JACKSON HOLE, WYOMING (MarketWatch) - Federal Reserve Board chairman Ben Bernanke said Friday that the central bank would not sit idly and let the U.S. economy sink into a period of deflation. "The Federal Open Market Committee will strongly resist deviations from price stability in the downward direction," Bernanke said in a speech opening the Fed's annual summer policy retreat. Bernanke downplayed concern that the economy would fall back into another downturn, or a double-dip recession. He said the economy would continue to grow at a slow pace in the last four months of the year and the pace of growth would pick-up in 2011. Bernanke said the Fed had not agreed on specific criteria or triggers for further easing.

"The Real Financial Crisis May Have Not Even Started Yet"

Economist Nassim Taleb says the worse is still likely ahead! This guy is not just an academic. He is a trader, so he has a more realistic prespective on events than any academic would ever comprehend.

Billionaire Gets Gold Fever

from Businessweek:

"I'm not a goldbug, but there are times when I feel like an evangelist for it," says Thomas Kaplan, an Oxford-educated historian and chairman of Manhattan-based Tigris Financial Group. "To my amazement, it's a hard sell. The conventional wisdom is that gold is for primitives. That derision shows me that contrary to the notion we're in a bubble, we haven't yet begun the real bull market."

The 47-year-old New York-born billionaire is a bundle of eccentricities, from his unplaceable but alien accent to his three-piece suits and his decidedly un-Wall Street way of talking ("as the thesis is confirmed, well-founded conviction gives way to the calm of metaphysical certitude"). Sitting in a windowless conference room decorated with lavish photographs of panthers, jaguars, and tigers—preserving big-cat habitats is his other major passion—he explains his training as an investor. "I'm much more qualitative than quantitative in my approach," Kaplan says. "It would have been an alien concept for me to think about an MBA."

His conviction about gold puts him in the company of such celebrated figures as George Soros and John Paulson, both of whom have been betting heavily on the yellow metal (and have invested alongside Kaplan in Vancouver-based mining company NovaGold Resources (NG)). At the moment, the wager looks inspired: The price of gold has risen for nine straight years, hitting an all-time high of $1,256.30 an ounce on June 21. While the price has fallen about 2 percent since then, Kaplan says the big rally is still to come. It's not riots in the streets he envisions, but a more fundamental case of demand outstripping supply as gold becomes a currency in its own right.

Variations on this view have become so popular in recent years that gold has gone from being an obsession of conspiracy theorists and kooks to a fully respectable investment idea that gets promoted at PTA meetings. Kaplan is not content to merely run with this crowd. To maximize his returns, he has engaged in the much trickier task of digging fresh gold out of the ground. But mining is a double risk—there's the cost, hassle, and uncertainty of extraction, and then there's the volatility of the market. The financial risks of mining show up in their stocks, especially compared with gold prices. While gold rose 13 percent this year, the Bloomberg World Mining Index dropped 9.7 percent. And gold is no more of a certainty than anything else. Before its recent ascent, it was stuck in a bear market for two decades. What if the threat of hyperinflation never materializes? A mere uptick in confidence about global growth could put gold right back in the doldrums.

Kaplan doesn't see that happening, and that's why he has fallen in love with the leafy green hills of Transylvania in central Romania. He owns an 18 percent stake in a Canadian company called Gabriel Resources that is attempting to reopen what is widely believed to be Europe's largest gold deposit, an estimated 10 million ounces, worth more than $12 billion at today's price, as well as 47.7 million ounces of silver. There's one problem: Some residents of the economically ravaged area, where unemployment is 80 percent, are fiercely contesting the project on environmental grounds.

Despite the opposition, the potential windfall has attracted investors, including Paulson, of whom Kaplan is an unabashed admirer. "If he sticks to his conviction on gold, he may yet become the richest man in America," Kaplan says, "and I'd love to see it happen." Kaplan would do well, too, though he brings his own particular dilemma—striking a balance between an urge to expand his mining empire and what he insists is an even greater desire to save the planet from environmental harm.

In 1988, Kaplan was completing his dissertation at Oxford—on the Malayan counterinsurgency and the way commodities influence strategic planning—and earning extra money analyzing Israeli companies listed on U.S. stock exchanges. The work involved traveling to Israel, and while there Kaplan connected with two people who would shape the rest of his life. First was Daphne Recanati, who had attended the same boarding school Kaplan had and was then just beginning her compulsory military service. She would eventually become his wife, mother of his three children—and his "reality check" for new investment ideas. "Her instincts are pretty much perfect," he says.

Through Recanati's mother, Kaplan was introduced to Avi Tiomkin, a well-known Israeli investor with whom he established a close bond. "There was immediate chemistry," says Tiomkin, now 62. "His views, his conviction were impressive." Kaplan sealed his standing with his mentor by predicting the invasion of Kuwait by Saddam Hussein several years before it happened, contradicting widely held wisdom that one Arab country would never attack another. "It was against all forecasts," Tiomkin remembers. "It was a huge surprise."

Kaplan commuted between Oxford and Tel Aviv until Recanati was accepted to New York University in 1991, and they moved back to the U.S. Tiomkin hired him as a junior partner, a position he held until 1993, when Tiomkin decided to focus on his Israeli investments and Kaplan left to execute his own big ideas, including major bets on silver, natural gas, and, eventually, gold.

He and Tiomkin kept in close touch. "We could've not seen each other for a few months and then continued the conversation where we left off," says Tiomkin. Like Kaplan, Tiomkin eschews his office most of the time, preferring to work from home or elsewhere. "It's in our genes, it's how we were born. It keeps us away from being too much under the influence of conventional wisdom." The two men have reunited and are now avoiding the same office. After working for various hedge funds including Caxton Associates, Tiomkin joined Tigris in 2008 as chief macro strategist, the same year he wrote an article for Forbes predicting the "demise of the euro."

Kaplan credits Marc Faber, the notoriously bearish Hong Kong-based publisher of the Gloom, Boom & Doom Report, with inspiring his move into natural resources investing in 1993. Faber has long argued that precious metals represent vital protection against the monetary foolishness of central governments. That year marked Kaplan's first defining deal, the launching of Apex Silver Mines to dig for silver in San Cristóbal, Bolivia. Among the early backers of Apex was Soros Fund Management.

With Apex, Kaplan pursued a strategy he is now trying to replicate in Romania: relocating villagers and buildings in the path of his mining plans to a new town nearby. Apex spent $12 million to move about 200 people as well as a cemetery and a colonial church, which was completely restored and rebuilt "brick by brick," Kaplan says. "San Cristóbal was transformed, and we established a foundation to create new, sustainable enterprises. To be from the new San Cristóbal became a badge of prosperity." Kaplan served as chief executive officer of Denver-based Apex and later its chairman. He resigned in 2004, and the company went bankrupt four years later, reemerging from bankruptcy protection in 2009.

Although he's fixated on gold these days, Kaplan hasn't abandoned silver. Through Silver Opportunity Partners, an affiliate of Kaplan's Electrum exploration group of companies, he bought key assets of Sterling Mining Co.—which include the Sunshine Mine, nestled in the heart of the "Silver Valley" of Idaho—out of bankruptcy earlier this year. Well known in mining circles, Kaplan and his team worked hard to keep a low profile leading up to the bankruptcy auction so as not to tip their hand and drive up the bidding. The Sunshine transition team was headed by Mark Wallace, president of Tigris.

Sunshine is among the most notorious mines in the world. First discovered in 1884, Sunshine produced an estimated 360 million ounces of silver. It closed in 2001, then reopened in 2007 before going broke less than a year later. Its checkered history includes a 1972 fire that killed 91 miners, one of the worst disasters of its kind in the U.S. A 12-foot-tall, painted-steel sculpture of a silver miner with a rock drill stands along I-90 between Kellogg and Wallace, Idaho, in memorial to the dead workers.

Now, Silver Opportunity is studying the economic and environmental issues surrounding restarting the mine. Wallace says the deal was a case study for Kaplan's investment approach. "It was no doubt a complicated and risky transaction," Wallace says. "Through our expertise, we were able to minimize the risk involved, resolve litigation, and reunite the patchwork and fractured ownership interests that inhibited the mine and limited its value over the last decade."

While Wallace sorts out the Sunshine mess, Kaplan pursues other interests: In 2006 he created a nonprofit called Panthera to focus on saving big cats. Among its projects is a collaboration with the Wildlife Conservation Society to boost the tiger population in certain countries, including India, Myanmar, and China, by 50 percent over the next decade. After a long and involved courtship, he persuaded Alan Rabinowitz, a zoologist with a specialty in big cats, to become president of Panthera. When he was first approached by Kaplan, Rabinowitz, who had spent his career at WCS, was close to retirement and was torn about taking a new job. Kaplan kept the position open for a full year while Rabinowitz debated whether to accept it. On Apr. 1, 2008, he and five other WCS employees joined Panthera, with ambitious goals. "We have realized that you have to fight for them as a species everywhere they exist on earth," Rabinowitz, now 56, says. To that end, Panthera is negotiating with governments across the globe to create "genetic corridors" so cats can move freely without being constrained by man-made borders. Kaplan and Rabinowitz have developed a deep friendship; they are "BB" and "LB" to each other; Rabinowitz is the big brother, Kaplan the little brother.

"When I met Alan, I realized he'd been doing what I'd wanted to do with my own life," says Kaplan. "Nonetheless, I'd always harbored this dream that I'd be able to return to my true love."

Kaplan acknowledges the paradox of promoting conservation while investing in an industry long associated with extreme environmental degradation, but he says any conflict between the two is easy for him to resolve. "If I'm given a choice between conservation and business, conservation wins, always," he says. "I've conserved a great multiple more than I've disturbed." His geologists apply what he calls the Tom Rule to their decisions about what land to acquire for mining. "If it looks like we shouldn't build a mine here, either take it and I'll hold the land to stop others from building on it, or skip it," he says. "I tell them: 'Use your common and aesthetic sense.' It sounds crazy to refer to aesthetics, but ultimately the morality of the endeavor should win out."

This was on his mind when he arrived in Transylvania in 2009 to get a gut check on Rosia Montana. He had alerted no one there about his visit, flying into the tiny Romanian city of Saibu with several colleagues from Tigris' London office and enduring a three-hour drive through the mountains. They explored the back roads around the mine, witnessing a degree of ecological damage that left Kaplan to theorize that the pollution dated to the time when the Roman Emperor Trajan conquered the region, marking the beginning of Rosia Montana's mining heritage.

Community and environmental activists have been fighting Gabriel Resources' plans for a decade, arguing that the use of cyanide in the mine threatens nearby villages and that a spill could contaminate the countryside extending into neighboring Hungary, where officials have joined the opposition. Kaplan counters that the area already has been devastated by centuries of mining—"the river literally runs red from sulfides"&mdashand that digging the mine would in fact help the county of Alba by repairing some of the damage of past mining projects.

Leading the resistance to the mine is a nongovernmental organization called Alburnus Maior, which was started in 2000 and is based at Rosia Montana. The group contends that Gabriel's plans will destroy historical sites and force resettlement of 740 farms and 140 apartments. The group also says that 40 Romanian NGOs and institutions support its "Save Rosia Montana" campaign, which proposes to boost the local economy through tourism, agribusiness, and small industries, including crafts. "We will continue to use all legal means at our disposal to stop this proposal from ever being realized," Alburnus Maior's Stephanie Roth said in an e-mail. Roth, a former environmental journalist, was instrumental in persuading the European Parliament to publicly oppose the mine. She said the fact that some residents will ultimately refuse to sell their properties to Gabriel means the mine won't ever get under way because the company needs all of the land to secure a construction permit. "I don't think that Gabriel's project will ever go ahead, and in contrast to Gabriel, the locals have all the time in the world," Roth said.

Rozalia Drumus, a 79-year-old retired schoolteacher, lives in Rosia Montana with her unemployed daughter and subsists on a 1,159 lei ($337) monthly pension. She has planted a sign on her gate: This property is NOT for sale. "We had a small happy village, but people's greed for money was too much," she says. "Gold is a bastard."

Kaplan ardently defends Gabriel's efforts, arguing that mining is the best way to help the economy of Romania. "Those who say a scarred landscape should be preserved at the expense of a truly exciting economic future for a poor community are being unjust," he says. "This is telling the local people to bootstrap their way to progress when they don't have the means to procure boots."

In June, Romania's environment minister said the government probably will resume a review of the project, which likely means months more of public debate. Even if Romanian government approval is obtained, it will take at least a year before gold can be pulled out of the ground. Meanwhile, as gold prices swing wildly and talk of a double-dip recession ripples across the markets, Kaplan retains his karmic calm. "People view gold as emotional, but when they demythologize it, when they look at it for what it is and the opportunity it represents, they're going to say, 'We really should own some of that.' The question will then change to 'Where do we get the gold?' "

More Dollar Dissolution Planned

The beginning of the end of the dollar? Banks Back Switch to Renminbi for Trade - A number of the world’s biggest banks have launched international roadshows promoting the use of the renminbi to corporate customers instead of the dollar for trade deals with China. HSBC, which recently moved its chief executive from London to Hong Kong, and Standard Chartered, are offering discounted transaction fees and other financial incentives to companies that choose to settle trade in the Chinese currency.

Thursday, August 26, 2010

Obama Picks Trade War With China

This is amazing! Trade wars and retaliations were one of the factors that worsened the Great Depression. Now, Obama is making the same mistake again!

from Bloomberg:

The Obama administration plans to step up enforcement of trade laws against nations, such as China and Vietnam, that help subsidize companies exporting cheap goods to the U.S.

The U.S. Commerce Department developed 14 proposals to crack down on illegal import practices and require parties to pay the full amount of any duties, according to a statement today. The process to adopt the plan, which the department said is especially aimed at countries where the government has control over markets, will begin later this year.

"Generally, this is targeted at China, and China will see it as such," said David Spooner, a former Bush administration official now a trade lawyer with Squire Sanders in Washington who represented Chinese companies in a tariffs disputes. "The aim is to raise the price of goods from China."

The plan is part of the administration's effort to double exports in the next five years to spur job growth, a goal President Barack Obama set in his State of the Union speech in January. Doubling exports would help support 2 million new jobs, the administration said.

"This is a very important move on the part of the administration," said Dan DiMicco, chief executive officer of Nucor Corp., the largest U.S. steelmaker. He said the U.S. also needs to resolve issues tied to the yuan because China's currency is undervalued by as much as 60 percent.

"Before American manufacturers get out of bed in the morning, they're already at a 40 to 60 percent disadvantage," DiMicco said in a telephone interview. "As long as we continue to let them get away with it, they'll keep doing it."

China Meets Obligations

DiMicco, a member of an administration advisory panel on manufacturing issues, said the today's proposals are consistent with recommendations from the group.

"China is now a market economy country and the Chinese enterprises conduct business with foreign enterprises in accordance with its obligation upon joining" the World Trade Organization, said Wang Baodong, a spokesman for the Chinese Embassy in Washington. "Foreign countries should not in any way set up obstacles to normal economic cooperation and trade between China and foreign enterprises."

The proposals would end the practice of letting individual foreign companies seek an exemption from extra duties if they show they weren't dumping or receiving subsidies during a certain period. Under the plan, companies would have to wait for the normal country-wide expiration of the duties.

Cash Vs. Bond

Also, importers would have pay a cash deposit to continue bringing products into the U.S. during an investigation, instead of being able to post a bond for the estimated duties owed. The department said that, in the past, that estimate was too low.

The measures will give U.S. companies "a more certain sense that the injury they believe they've had because of unfair trade practices can be addressed," said Ronald Lorentzen, deputy assistant secretary for import administration, which enforces laws tied to unfair trade acts.

Some changes will align the U.S. with practices followed by other countries and deal with issues the department has seen in past cases, he said. Comment from the public will be sought before the changes take effect.

Another proposal would alter how the department determines a country's wage rate, which is used to calculate whether products are being sold in the U.S. at artificially low prices.

ITA Effectiveness

The proposals are designed to improve the effectiveness of the International Trade Administration, which investigates whether foreign companies exporting products to the U.S. are receiving unfair subsidies from their home countries or flooding U.S. markets to undercut American businesses.

The Commerce Department estimated that American exports accounted for 7 percent of employment and one in three manufacturing jobs in 2008. Exports increased 17 percent in the first four months of 2010 from the same year-ago period, the department said.

Last year, the ITA's Import Administration began 34 anti- dumping and countervailing duty investigations, compared with 19 in 2008, the department said.

Senator Charles Schumer, a New York Democrat, and 14 colleagues in February said Chinese exporters should face stiffer U.S. tariffs to compensate for the advantage they get from the undervalued yuan, an issue that's part of a dispute over glossy paper imports from China. Spooner said that the department probably will avoid the currency issue.

Currency Dispute

"Commerce will almost surely refuse to investigate Chinese currency as a subsidy and this announcement today is meant to take the political sting out of that," Spooner said.

DiMicco said the administration has gone further than its two predecessors in addressing some of the issues with China and needs to go further.

"They recognize there's a massive manipulation going on, but they're doing the same things the Bush and Clinton administrations did -- try to negotiate," DiMicco said. "Billions and trillions of dollars worth of damage has been done. They need to enforce the rules and make sure people play by the rules or we will not be able to turn this around."

Morgan Stanley Says Debt Crisis Is Just Beginning

This spring's bond market tussle in Europe was just a warm-up, Morgan Stanley says.

The investment bank warns in a report Wednesday that the sovereign debt crisis is far from over -- and won't end till deeply indebted rich country governments give holders of their bonds a good soaking.

The remarks amount to the latest warning issued to investors who have herded into government bonds this month, following a downturn in U.S. economic indicators and a series of anxious-sounding comments from Federal Reserve officials. The yield on the 10-year Treasury bond has plunged to a recent 2.45% from the already low level of 3% at the end of last month.

That rally surely has been driven in part by fear that the world is in for a long period of subpar growth. But it has been aided, the report contends, by the observation that holders of government bonds (and bonds issued by too big to fail banks) have received what amounts to preferential treatment during three years of crisis.

That can't go on forever, analyst Arnaud Mares writes in the firm's first Sovereign Subjects report.

"The question is not whether they will renege on their promises," he writes of rich country governments, "but rather upon which of their promises they will renege, and what form this default will take."

While Morgan Stanley said it doesn't expect the biggest governments to stop making payments outright – currency issuers such as the United States and United Kingdom can, after all, simply print money if the need arises – it does believe buyers at current prices leave themselves scant defense against other tools policymakers might use to chip away at the their burdens, such as inflation, tax increases and regulatory restrictions.

"Outright sovereign default in large advanced economies remains an extremely unlikely outcome, in our view," Manes writes. "But current yields and break-even inflation rates provide very little protection against the credible threat of financial oppression in any form it might take."

Mares writes that while there has been much discussion of rising debt levels in rich country governments, even those scary-looking numbers understate the scale of the problem.

"Debt/GDP ratios are too backward-looking and considerably underestimate the fiscal challenge faced by advanced economies' governments," Mares writes.

The rating agencies have made similar points in recent weeks, contending that the biggest problem for policymakers is not the debt they have on the books now but the borrowing they will have to do in coming years to make good on promises coming due in the future.

Just to drive the point home, however, Mares likens the deteriorating fiscal situation in countries like the United States and Japan to the fix many bubble-era Sun Belt house buyers now find themselves in. To extend the analogy, bondholders are like the banks the lent to these poor saps when the housing bubble was whipped into a frothy peak.

"On the basis of current policies," Mares writes, "most governments are deep in negative equity."

The big question now, he continues, is what form this exciting new round of walking-away will take. For bondholders, he concludes, "History is not so reassuring after all."

The investment bank warns in a report Wednesday that the sovereign debt crisis is far from over -- and won't end till deeply indebted rich country governments give holders of their bonds a good soaking.

Default comes in many flavors

That rally surely has been driven in part by fear that the world is in for a long period of subpar growth. But it has been aided, the report contends, by the observation that holders of government bonds (and bonds issued by too big to fail banks) have received what amounts to preferential treatment during three years of crisis.

That can't go on forever, analyst Arnaud Mares writes in the firm's first Sovereign Subjects report.

"The question is not whether they will renege on their promises," he writes of rich country governments, "but rather upon which of their promises they will renege, and what form this default will take."

While Morgan Stanley said it doesn't expect the biggest governments to stop making payments outright – currency issuers such as the United States and United Kingdom can, after all, simply print money if the need arises – it does believe buyers at current prices leave themselves scant defense against other tools policymakers might use to chip away at the their burdens, such as inflation, tax increases and regulatory restrictions.

"Outright sovereign default in large advanced economies remains an extremely unlikely outcome, in our view," Manes writes. "But current yields and break-even inflation rates provide very little protection against the credible threat of financial oppression in any form it might take."

Mares writes that while there has been much discussion of rising debt levels in rich country governments, even those scary-looking numbers understate the scale of the problem.

"Debt/GDP ratios are too backward-looking and considerably underestimate the fiscal challenge faced by advanced economies' governments," Mares writes.

The rating agencies have made similar points in recent weeks, contending that the biggest problem for policymakers is not the debt they have on the books now but the borrowing they will have to do in coming years to make good on promises coming due in the future.

Just to drive the point home, however, Mares likens the deteriorating fiscal situation in countries like the United States and Japan to the fix many bubble-era Sun Belt house buyers now find themselves in. To extend the analogy, bondholders are like the banks the lent to these poor saps when the housing bubble was whipped into a frothy peak.

"On the basis of current policies," Mares writes, "most governments are deep in negative equity."

The big question now, he continues, is what form this exciting new round of walking-away will take. For bondholders, he concludes, "History is not so reassuring after all."

Hyperinflation Explanation II

by Gonzalo Lira:

I usually don’t do follow-up pieces to any of my posts. But my recent longish piece, describing how hyperinflation might happen in the United States, clearly struck a nerve.

It was a long, boring, snowy piece of macro-economic policy speculation, discussing Treasury yields, Federal Reserve Board monetary reaction, and the difference between inflation and hyperinflation—but considering the traffic it generated, I might as well been discussing relative breast size in the porn industry. With pictures.

The disproportionate attention my post garnered is indicative of people’s current fears. As I’ve said before, people aren’t blind or stupid, even if they often act that way. People are worried—they’re worried about the current state of affairs: Massive quantitative easing, toxic assets replaced by the full faith and credit of the U.S. government in the shape of Treasuries, fiscal debt which cannot possibly be repaid, a second leg down in the Global Depression that seems endless and only getting worse—people are scared. Many readers gave me quite a bit of useful feedback, critiques, suggestions and comments on the piece—clearly, what I was discussing touched on a deeply felt concern.

However, there were two issues that many readers had a hard time wrapping their minds around, with regards to a hyperinflationary event:

The first was, Where does all the money come from, for hyperinflation to happen? The question wasn’t put as baldly as that—it was wrapped up in sophisticated discussions about M1, M2 and M3 money supply, as well as clever talk about the velocity of money—the acceleration of money—the anti-lock brakes on money. There were even equations thrown around, for good measure.

But stripped of all the high-falutin’ language, the question was, “Where’s all the dough gonna come from?” After all, as we know from our history books, hyperinflation involves people hoisting bundles and bundles of high-denomination bills which aren’t worth a damn, and tossing them into the chimney—’cause the bundles of cash are cheaper than firewood. If the dollar were to crash, where would all these bundles of $100 bills come from?

The second question was, Why will commodities rise, while equities, real estate and other assets fall? In other words, if there is an old fashioned run on a currency—in this case, the dollar, the world’s reserve currency—why would people get out of the dollar into commodities only, rather than into equities and real estate and other assets?

In this post, I’m going to address both of these issues.

Apart from what happened with the Weimar Republic in the 1920’s, advanced Western economies have no experience with hyperinflation. (I actually think that the high inflation that struck the dollar in the 1970’s, and which was successfully choked off by Paul Volcker, was in fact an incipient bout of commodity-driven hyperinflation—but that’s for some other time.) Though there were plenty of hyperinflationary events in the XIX century and before, after the Weimar experience, the advanced economies learned their lesson—and learned it so well, in fact, that it’s been forgotten.

However, my personal history gives me a slight edge in this discussion: During the period 1970–’73, Chile experienced hyperinflation, brought about by the failed and corrupt policies of Salvador Allende and his Popular Unity Government. Though I was too young to experience it first hand, my family and some of my older friends have vivid memories of the Allende period—vivid memories that are actually closer to nightmares.

However, there were two issues that many readers had a hard time wrapping their minds around, with regards to a hyperinflationary event:

The first was, Where does all the money come from, for hyperinflation to happen? The question wasn’t put as baldly as that—it was wrapped up in sophisticated discussions about M1, M2 and M3 money supply, as well as clever talk about the velocity of money—the acceleration of money—the anti-lock brakes on money. There were even equations thrown around, for good measure.

But stripped of all the high-falutin’ language, the question was, “Where’s all the dough gonna come from?” After all, as we know from our history books, hyperinflation involves people hoisting bundles and bundles of high-denomination bills which aren’t worth a damn, and tossing them into the chimney—’cause the bundles of cash are cheaper than firewood. If the dollar were to crash, where would all these bundles of $100 bills come from?

The second question was, Why will commodities rise, while equities, real estate and other assets fall? In other words, if there is an old fashioned run on a currency—in this case, the dollar, the world’s reserve currency—why would people get out of the dollar into commodities only, rather than into equities and real estate and other assets?

In this post, I’m going to address both of these issues.

Apart from what happened with the Weimar Republic in the 1920’s, advanced Western economies have no experience with hyperinflation. (I actually think that the high inflation that struck the dollar in the 1970’s, and which was successfully choked off by Paul Volcker, was in fact an incipient bout of commodity-driven hyperinflation—but that’s for some other time.) Though there were plenty of hyperinflationary events in the XIX century and before, after the Weimar experience, the advanced economies learned their lesson—and learned it so well, in fact, that it’s been forgotten.

However, my personal history gives me a slight edge in this discussion: During the period 1970–’73, Chile experienced hyperinflation, brought about by the failed and corrupt policies of Salvador Allende and his Popular Unity Government. Though I was too young to experience it first hand, my family and some of my older friends have vivid memories of the Allende period—vivid memories that are actually closer to nightmares.

The causes of Chile’s hyperinflation forty years ago were vastly different from what I believe will cause American hyperinflation now. But a slight detour through this history is useful to our current predicament.

To begin: In 1970, Salvador Allende was elected president by roughly a third of the population. The other two-thirds voted for the centrist Christian Democrat candidate, or for the center-right candidate in roughly equal measure. Allende’s election was a fluke.

He wasn’t a centrist, no matter what the current hagiography might claim: Allende was a hard-core Socialist, who headed a Hard Left coalition called the Unidad Popular—the Popular Unity (UP, pronounced “oo-peh”). This coalition—Socialists, Communists, and assorted Left parties—took over the administration of the country, and quickly implemented several “reforms”, which were designed to “put Chile on the road to Socialism”.

He wasn’t a centrist, no matter what the current hagiography might claim: Allende was a hard-core Socialist, who headed a Hard Left coalition called the Unidad Popular—the Popular Unity (UP, pronounced “oo-peh”). This coalition—Socialists, Communists, and assorted Left parties—took over the administration of the country, and quickly implemented several “reforms”, which were designed to “put Chile on the road to Socialism”.

Land was expropriated—often by force—and given to the workers. Companies and mines were also nationalized, and also given to the workers. Of course, the farms, companies and mines which were stripped from their owners weren’t inefficient or ineptly run—on the contrary, Allende and his Unidad Popular thugs stole farms, companies and mines from precisely the “blood-thirsty Capitalists” who best treated their workers, and who were the most fair towards them.

Allende’s government also put UP-loyalists in management positions in those nationalized enterprises—a first step towards implementing a Leninist regime, whereby the UP would have “political control” over the means of production and distribution. From speeches and his actions, it’s clear that Allende wanted to implement a Maoist-Leninist regime, with himself as Supreme Leader.

One of the key policy initiative Allende carried out was wage and price controls. In order to appease and co-opt the workers, Allende’s regime simultaneously froze prices of basic goods and services, and augmented wages by decree.

At first, this measure worked like a charm: Workers had more money, but goods and services still had the same old low prices. So workers were happy with Allende: They went on a shopping spree—and rapidly emptied stores and warehouses of consumer goods and basic products. Allende and the UP Government then claimed it was right-wing, anti-Revolutionary “acaparadores”—hoarders—who were keeping consumer goods from the workers. Right.

Meanwhile, private companies—forced to raise worker wages while maintaining their same price structures—quickly went bankrupt: So then, of course, they were taken over by the Allende government, “in the name of the people”. Key industries were put on the State dole, as it were, and made to continue their operations at a loss, so as to satisfy internal demand. If there was a cash shortfall, the Allende government would simply print more escudos and give them to the now State-controlled companies, which would then pay the workers.

This is how hyperinflation started in Chile. Workers had plenty of cash in hand—but it was useless, because there were no goods to buy.

Meanwhile, private companies—forced to raise worker wages while maintaining their same price structures—quickly went bankrupt: So then, of course, they were taken over by the Allende government, “in the name of the people”. Key industries were put on the State dole, as it were, and made to continue their operations at a loss, so as to satisfy internal demand. If there was a cash shortfall, the Allende government would simply print more escudos and give them to the now State-controlled companies, which would then pay the workers.

This is how hyperinflation started in Chile. Workers had plenty of cash in hand—but it was useless, because there were no goods to buy.

So Allende’s government quickly instituted the Juntas de Abastecimiento y Control de Precios (“Unions of Supply and Price Controls”, known as JAP). These were locally formed boards, composed of loyal Party members, who decided who in a given neighborhood received consumer products, and who did not. Naturally, other UP-loyalists had preference—these Allende backers received ration cards, with which to buy consumer goods and basic staples.

Of course, those people perceived as “unfriendly” to Allende and the UP Government either received insufficient rations for their families, or no rations at all, if they were vocally opposed to the Allende regime and its policies.

Very quickly, a black market in goods and staples arose. At first, these black markets accepted escudos. But with each passing month, more and more escudos were printed into circulation by the Allende government, until by late ’72, black marketeers were no longer accepting escudos. Their mantra became, “Sólo dólares”: Only dollars.

Hyperinflation had arrived in Chile.

Very quickly, a black market in goods and staples arose. At first, these black markets accepted escudos. But with each passing month, more and more escudos were printed into circulation by the Allende government, until by late ’72, black marketeers were no longer accepting escudos. Their mantra became, “Sólo dólares”: Only dollars.

Hyperinflation had arrived in Chile.

(Most Chileans, myself included, find ourselves both amused and irritated, whenever Americans self-righteously claim that Nixon ruined Chile’s economy, and thereby derailed Allende’s “Socialist dream”. Yes, according to Kissinger’s memoirs, Nixon did in fact tell the CIA that he wanted Chile’s economy to “scream”—but Allende did such a bang-up job of destroying Chile’s economy all on his own that, by the time Richard Helms got around to implementing his pissant little plots against the Chilean economy, there was not much left to ruin.)

One of the effects of Chile’s hyperinflation was the collapse in asset prices.

This would seem counterintuitive. After all, if the prices of consumer goods and basic staples are rising in a hyperinflationary environment, then asset prices should rise as well—right? Equities should rise in price—since more money is chasing after the same number of stock. Real estate prices should rise also—and for the same reason. Right?

Actually, wrong—and for a simple reason: Once basic necessities are unmet, and remain unmet for a sustained period of time, any asset will be willingly and instantly sacrificed, in order to meet that basic need.

To put it in simple terms: If you were dying of thirst in the middle of the desert, would you give up your family heirloom diamonds, in exchange for a gallon of water? The answer is obvious—yes. You would sacrifice anything and everyting—instantly—in order to meet your basic needs, or those of your family.

So as the situation in Chile deteriorated in ’72 and into ’73, the stock market collapsed, the housing market collapsed—everything collapsed, as people either cashed out of their assets in order to buy basic goods and staples on the black market, or cashed out so as to leave the country altogether. No asset class was safe, from this sell-off—it was across-the-board, and total.

Now let’s return to the possibility of hyperinflation in the United States:

If there were a sudden collapse in the Treasury bond market, I argued that sellers would take their cash and put them into commodities. My reasoning was, they would seek a sure store of value. If Treasury bonds ceased to be that store of value, then people would invest in the next best thing, which would be commodities, especially precious and industrial metals, as well as oil—in other words, non-perishable commodities.

Some people argued this point with me. They argued many different approaches to the problem, but essentially, it all boiled down to the argument that commodities and precious metals have no intrinsic value.

Actually, I think they’re right. In a strict sense, only oxygen, food and water have intrinsic value to human beings—everything else is superfluous. Therefore the value of everything else is arbitrary.

Yet both gold and silver have, historically, been considered valuable. Setting aside a theoretical or mathematical construct that would justify the value of gold and silver, look at it from a practical standpoint: If I went to a farmer with five ounces of silver, would he give me a sack of grain? Probably. If I offered him an ounce of gold for two or three pigs, would he give them to me? Again, probably.

Where there is a human society, there is a need to exchange. Where there is a need to exchange, a medium of exchange will soon appear. Gold and silver (and copper and brass and other metals) have served that purpose for literally millennia, but then they were replaced by paper.

Right now, there are two forms of paper currency: Actual dollars, and Treasury bonds. One is a medium of exchange, the other a store of value.

If Treasuries—the store of value—were to collapse in price, and the Fed—as I predict—tried everything in its power to at least initially prop up their prices, would those sellers who managed to get out of Treasuries in time then turn around and invest in even dodgier bits of paper, like stocks? Or REIT’s? Or even precious metal ETF’s?

No they would not: They would get out of Treasuries—supposedly the “safest” investment there is—and get into something even safer—something even more tangible: Actual commodities. Not ETF’s, not even futures (or anything else that entails counterparty risk)—sellers of Treasuries would get into actual, hard commodities. Because if suddenly even the safest of all investment vehicles is now unsafe, do you really want to get behind the wheel of an even more unsafe vehicle, like stocks or corporate bonds or ETF’s? I mean, c’mon: If Treasuries crash, what else might crash?

That’s why people in a Treasury panic would buy commodities. This ballooning of non-perishable commodities would be as a means to store value. Because that’s what people do in a panic—they batten down the hatches, and go into what’s safest. When the stock markets tanked in the Fall of ’08, where did all that sellers’ cash go? To Treasuries—because it was then considered the safest store of value. Commodities suffered in comparison—gold took a bit of a hit, as did the other precious metals—but Treasuries ballooned as the equities markets tanked.

But if Treasuries—the ultimate store of value—now tanked? If the last sure-thing in paper-based stores of value took a hit, where would people go to both store value, and have ready access to that value?

Commodities. And this rush to commodities, I argued, would trigger hyperinflation.

Now, I said I would answer two questions—one was why commodities would outpace all other asset classes in a Treasury panic and subsequent hyperinflation. The other question was, “Where’s all the dough to feed my fireplace gonna come from, in a hyperinflationary event?”

The first wave of dollars in a hyperinflationary event will come from people’s savings accounts.

If Treasuries tank, and the markets all barrel into commodities, then prices will rise for regular consumers—this should not be a controversial inference. What would consumers do, with suddenly much higher gas prices, and soon much higher food prices? Simple: They’ll bust open their piggy banks, whatsoever those piggy banks might happen to be: 401(k)s, whatever equities they might have, etc.

But if the higher consumer prices continue—or become worse—what will happen to the 320 million American consumers? They’ll start buying more gas now, rather than wait around for tomorrow—and the market will react to this. How? Two way: Prices of commodities will rise even further—and asset prices will fall even lower.

Again, the man in the desert, the diamonds, and the water: If American consumers are getting hit at the gas station and the supermarket, they’ll start selling everything so as to buy gas, heating oil (most especially) and foodstuffs. The Treasury panic will thus be transfered to the average consumer—from Wall Street to Main Street by way of $15 a gallon gas prices, and $10 a gallon heating oil prices.

All other consumer prices would soon follow the leads of gas, heating oil and food.

In the above bit of Chilean history, I described how the Allende government printed up escudos to make up for the shortfall in nationalized businesses that was produced by their policy of hiking wages, while at the same time fixing prices.

The first wave of dollars in a hyperinflationary event will come from people’s savings accounts.

If Treasuries tank, and the markets all barrel into commodities, then prices will rise for regular consumers—this should not be a controversial inference. What would consumers do, with suddenly much higher gas prices, and soon much higher food prices? Simple: They’ll bust open their piggy banks, whatsoever those piggy banks might happen to be: 401(k)s, whatever equities they might have, etc.

But if the higher consumer prices continue—or become worse—what will happen to the 320 million American consumers? They’ll start buying more gas now, rather than wait around for tomorrow—and the market will react to this. How? Two way: Prices of commodities will rise even further—and asset prices will fall even lower.

Again, the man in the desert, the diamonds, and the water: If American consumers are getting hit at the gas station and the supermarket, they’ll start selling everything so as to buy gas, heating oil (most especially) and foodstuffs. The Treasury panic will thus be transfered to the average consumer—from Wall Street to Main Street by way of $15 a gallon gas prices, and $10 a gallon heating oil prices.

All other consumer prices would soon follow the leads of gas, heating oil and food.

In the above bit of Chilean history, I described how the Allende government printed up escudos to make up for the shortfall in nationalized businesses that was produced by their policy of hiking wages, while at the same time fixing prices.

This is a completely different way to hyperinflation than the way I envision it for the American economy—but once the American economy gets there, the effects of hyperinflation will be exactly the same: People will try to get out of assets in order to get hold of commodities. To get all eccy about it, money velocity would approach infinity, as money supply remains (at first) fixed, yet in the panic over commodities, aggregate demand as measured by aggregate transactions goes vertical.

Would there be Federal government intervention of some sort? Most definitely—people would be screaming for it. Would food rationing be implemented? Probably, and probably by way of the current Food Stamps program. Troops on the streets, protecting gas stations and supermarkets? Curfews to prevent looting? Palliative dollar printing? Yes, yes, and very likely yes.

That last bit—palliative dollar-printing: That’s the key. When palliative dollar-printing happens, it will be the final stages of hyperinflation—it’s when sensible people ought to realize that the crisis is almost over, and that a new normal will soon appear. But this stage will be /really/ awful.

Palliative dollar printing will take place when the Federal government simply runs out of options. Smart economists will get on CNBC and argue that, “The velocity of money is destroying the economy—we must expand the currency base!” It’ll sound logical, but palliative money-printing will be a policy option born out of panic. The final policy option. It won’t be done for evil conspiratorial reasons—always remember Aphorism #6 (“Never ascribe to malice what can be explained by incompetence.”). It’ll be carried out because of fear and panic.

A whole boatload of fools in Washington, on seeing this terrible commodity-driven crisis unfold, with consumer prices shooting the moon, will scream for dollars to be printed—and their rationale will be perfectly reasonable, I can practically hear it now: “We've got to get cash into the hands of the average American citizen, so he or she can buy food and heating oil for their families! We can’t let Americans starve and freeze to death!”

Palliative money-printing will take place—hence the average American family will likely be using bundles of $100 bills to fire up the chimney that hyperinflationary winter.

Hoo-Ah.

That last bit—palliative dollar-printing: That’s the key. When palliative dollar-printing happens, it will be the final stages of hyperinflation—it’s when sensible people ought to realize that the crisis is almost over, and that a new normal will soon appear. But this stage will be /really/ awful.

Palliative dollar printing will take place when the Federal government simply runs out of options. Smart economists will get on CNBC and argue that, “The velocity of money is destroying the economy—we must expand the currency base!” It’ll sound logical, but palliative money-printing will be a policy option born out of panic. The final policy option. It won’t be done for evil conspiratorial reasons—always remember Aphorism #6 (“Never ascribe to malice what can be explained by incompetence.”). It’ll be carried out because of fear and panic.