Showing posts with label Open Market Operations. Show all posts

Showing posts with label Open Market Operations. Show all posts

Thursday, November 11, 2010

Thursday, September 30, 2010

The Fed's Endless Wall Street Bailout

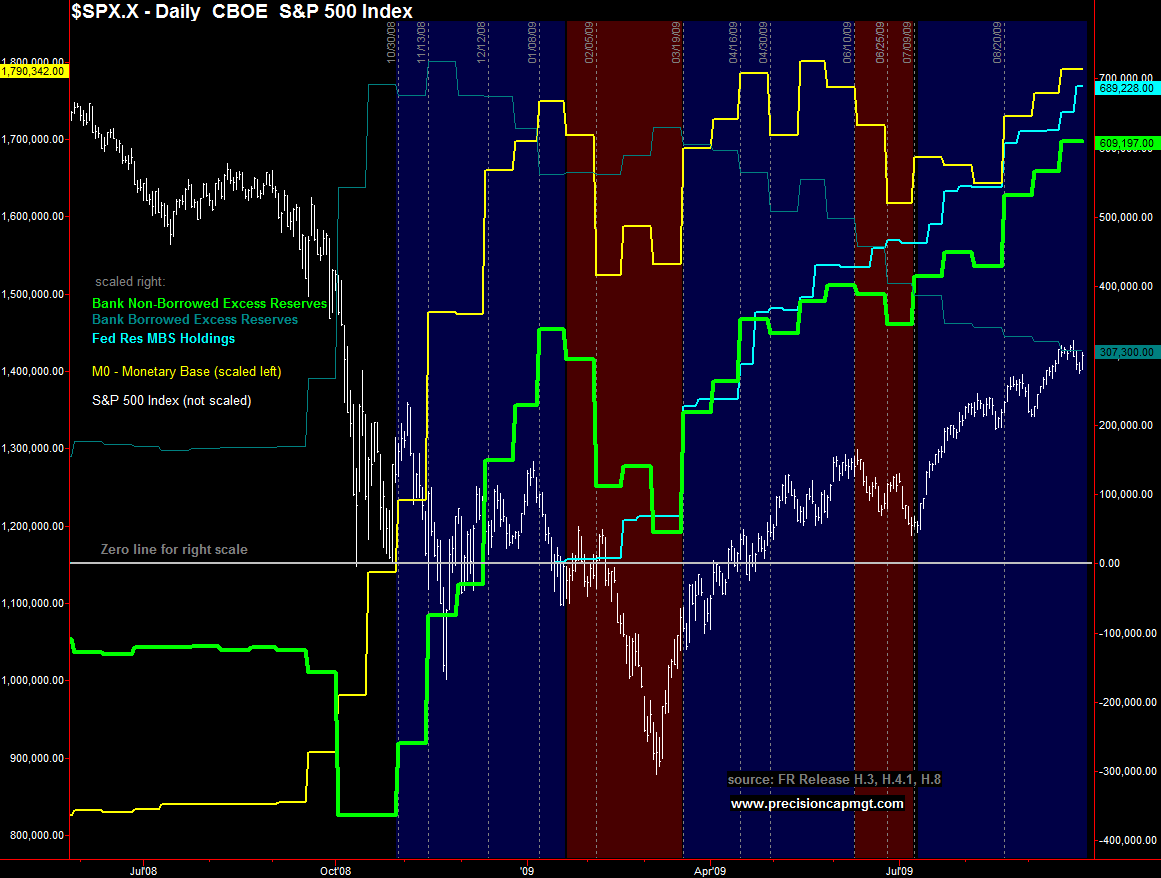

Since the Fed can inject "liquidity" into the financial markets, but can't determine with precision where those funds end up, I suspect that at least some of the Fed's money-printing is finding its way into commodity markets as well. In other words, the Fed's clumsy hand is fueling another commodity bubble! The below document was dated August 2009, and this is only an excerpt of the Executive Summary.

from Precision Capital Management:

The theory for which we have the greatest supporting evidence of manipulation surrounds the fact that the Federal Reserve Bank of New York (FRNY) began conducting permanent open market operations (POMO) on March 25, 2009 and has conducted 42 to date. Thanks to Thanassis Stathopoulos and Billy O’Nair for alerting us to the POMO Effect discovery and the development of associated trading edges. These auctions are conducted from about 10:30 am to 11:00 am on pre-announced days. In such auctions, the FRNY permanently purchases Treasury securities from selected dealers, with the total purchase amount for a day ranging from about $1.5 B to $7.5 B. These days are highly correlated with strong paint-the-tape closes, with the theory being that the large institutions that receive the capital injections are able to leverage this money by 100 to 500 times and then use it to ramp equities.

Monday, September 27, 2010

Fed Admits to Manipulating Broad Financial Markets

Clearly, this includes commodities!

It is no secret that the Federal Reserve, and its now semi-daily interventions in market liquidity via ever increasing Permanent Open Market Operations (aka POMOs, next on deck - Wednesday and Friday for a total of about $7-8 billion), is rather hell bent on creating the impression that the economy is alive and well courtesy of a ramping stock market (when the causal relationship is always the other way around, but who cares). A reader got so disgusted by the POMO ramp game, he sent in an angry letter to Brian Sack's henchmen. Here is the Fed's response.

Dear Mr. (removed to maintain privacy):So if "the Federal Reserve's monetary policy actions are not aimed at correcting or influencing any particular market" is it safe to assume that actions are aimed at "correcting and influencing" all markets in general? Well, the Fed is already rampaging in USTs, Agency securities and FX, would it be too naive to assume equities are for some reason excluded...

Thank you for your recent correspondence in which you expressed your concerns about the Federal Reserve's influence on the stock market.

The Federal Reserve monitors all sectors of the economy, so that we can be prepared when crises arise. It is within this context that the Chairman is often called by Congress to offer his views on many issues that may or may not be directly related to monetary policy. I want to assure you that the Federal Reserve's monetary policy actions are not aimed at correcting or influencing any particular market. As you know, the goal of monetary policy is to foster conditions conducive to sustaining sound, noninflationary economic growth over time and policymakers must make decisions that provide the greatest benefit overall.

Again, thank you for writing.

Sincerely,

JPD

Board Staff

Sunday, August 22, 2010

How the Fed Props Up the Stock Market Through Permanent Open Market Operations

The Financial Times recently reported on the Fed’s latest exit strategy to eventually contain the inflation zombie:

During the crisis, the Fed created roughly $800bn of additional bank reserves to finance asset purchases and loans. This total is likely to rise in the coming months as the central bank completes its asset purchases and the Treasury unwinds financing it provided to the Fed. Fed officials think they could raise interest rates even with this excess supply of reserves by offering to pay banks to deposit their surplus funds with it rather than lend them out. However, they also want to use reverse repos in tandem to soak up some of the excess reserves. Policymakers call this a “belt and braces approach”. [The latter, clearly a nod to the great Gekko.]

Tyler Durden touched on this last Thursday, and we will expand upon it here as it is particularly relevant to our ongoing theory that it is the proceeds from permanent open market operations (POMOs) and their close cousins that are driving equities. Though this may be received wisdom to Zero Hedge readers, the Fed has done us the favor of providing additional evidence through the FT story. A bit of background, as we are new contributors to this forum:

Tyler Durden touched on this last Thursday, and we will expand upon it here as it is particularly relevant to our ongoing theory that it is the proceeds from permanent open market operations (POMOs) and their close cousins that are driving equities. Though this may be received wisdom to Zero Hedge readers, the Fed has done us the favor of providing additional evidence through the FT story. A bit of background, as we are new contributors to this forum:Money Supply: Based on our previous research on the effects of swings in M2 non-seasonally adjusted money supply (M2) on the stock market, we were a bit surprised in July 09 by the resiliency of the rally, which continued in the face of such a dramatic contraction in M2. The dismal Durable Goods report from last Friday confirms that the capital goods sector is still under significant pressure as a result of a lack of money in the general economy. With banks not lending to normal businesses and consumer credit contracting equally as violently, what is the basis for this rally and from where does the never-ending flow of equities juice flow?

Bank Non-Borrowed Excess Reserves: The Fed statistic that most closely correlates with the 2009 equities run-up appears to be bank non-borrowed excess reserves (bank NBER), which is a component of the monetary base (M0). As explained by the Fed, bank NBER is simply total bank excess reserves minus bank borrowed excess reserves (bank BER). This resulted in bank NBER going negative throughout much of 2008 because banks acquired most of their excess reserves through participation in Fed lending programs. As the Fed has wound down these programs in 2009, bank BER has steadily declined and has been a drag on M0. Concurrently, though, bank NBER has advanced since late March 09 with only one brief material pause in June, and reflects those excess reserves that need not be repaid as part of any Fed lending program. The Fed purchases of MBS, Agency and Treasury securities netted $990 trillion since March 09. The distinction between borrowed and non-borrowed excess reserves is critical because the latter would be ideally suited for leveraging and lending out to hedge funds and the like to “invest” in the high beta stocks that have led the rally.

The primary conclusion is simple - the stock juice flows from steadily increasing Bank NBER, which is hidden to even astute observers that focus on only M0 or M2. Though we previously found no historical correlation between M0 (or its constituent components) and the stock market, we have witnessed an historically unprecedented set of circumstances. Now that the Fed has become the world’s largest hedge fund, we are prepared to accept unorthodox conclusions.

So why not inflate both equities and the general economy simultaneously? It was most likely a race against time. The administration and Fed needed to replace the incredible evaporation of wealth that occurred in late 2008/early 2009 to quell the voting and investing masses. They could not reflate the entire economy this quickly without jeopardizing their ability to borrow cheaply and restart the housing bubble. To keep long term yields low, they reflated the stock market only, with the hope that the general economy would eventually catch up in 2010 and be able to sustain the stock market gains. The problem with rising yields has not been solved, but was postponed.

As we noted in previous research, we are toward the end of a seasonal drain on M2. Once over the October hump, it should be easier for the holiday season to carry the market into March 2010, especially with the help of another $834 billion in MBS and Agency POMO into next March (not to mention the possible Treasury SFP wind-down effect to the tune of $114 to 185 billion). The Fed must be perfect, however, as any new panic will quickly feed on itself and likely lead to another mass exodus from equities. This is quite simply because currently, there is absolutely nothing else to back up this rally in the general economy if the Fed funny money cannot do its trick.

Back to Money Market Funds: If bank NBER is materially tied up in equities, then the Fed cannot drain from this source to mitigate inflation, or it risks the resulting cascade of sell orders that accompany the typical panic. According to the FT article:

The obvious counterparties for reverse repo deals are the Wall Street primary dealers. However, the Fed thinks they would only have balance sheet capacity to refinance about $100bn of assets. By contrast, the money-market funds have $2,500bn in assets, which means they could plausibly refinance as much as $500bn in Fed assets. Officials think there would be appetite on the part of the funds, which are under pressure [at gunpoint] from regulators and investors to stick to low-risk liquid investments.The Fed Helps Build Our Case: As of September 17 09, bank NBER had increased by $563 billion since the March 09 rally began. With M2 net flat during this period, the $563 billion has not made its way into the general economy by any stretch. Perhaps it is sitting idle; however, the Fed says only $100 billion would be available from primary dealers in the future? As the vast bulk of bank NBER is concentrated in primary dealers, this begs the obvious question of what will be tying up the remaining $463 billion (and we are not including the expected increases in bank NBER into next March, which could double this amount)? Given a conservative lending leverage ratio of 10 to 1, there is potentially $4.63 trillion already sloshing around. Even if we are much more conservative, given the roughly $2 trillion increase in the US stock market since Mar 09, it is not only easily conceivable, but probable, that a substantial portion was courtesy of the Fed ATM machine.

As Gekko closed his famous speech in Wall Street, “Greed – you mark my words – will save Teldar, and that other malfunctioning corporation, the U.S.A.” While we have focused here only on coercive greed, it will be interesting nonetheless to see how this works out.

Subscribe to:

Posts (Atom)