This doesn't make sense! If the economy is doing so well, why would central bankers need to artificially boost the markets and asset prices to bubble levels by more quantitative easing?

This doesn't make sense! If the economy is doing so well, why would central bankers need to artificially boost the markets and asset prices to bubble levels by more quantitative easing?

Interest rates are collapsing in the bond market, which is a sign that investors are very worried.

When discussing central planning, as manifested by the policies of the world's central banks, a recurring theme is the upcoming reversion to the mean: whether in economic data, in financial statistics, or, as Dylan Grice points out in his latest piece, in luck. While the mandate of every institution, whose existence depends on the perpetuation of the status quo, is to extend the amplitude of all such deviations from the trendline median, there is only so much that hope, myth and endless paper dilution can achieve. And alas for the US, whose 3.5% bond yields are, according to Grice, primarily due to "150% luck", the mean reversion is about to come crashing down with a vengeance after 30 years of rubber band stretching. The primary reason is that while the official percentage of interest expenditures as a portion of total government revenues is roughly 10% based on official propaganda data, the real number, factoring in gross interest expense, and assuming a reversion to the historic average debt yield of 5.8%, means that right now, the US government is already spending 30% of its revenues on gross interest payments! And what is worse, is that the chart has entered the parabolic phase. Once the convergence of theoretical and real rates happens, and all those who wonder who will buy US debt get their answer (which will happen once the 10 Year is trading at 6% or more), the inevitability of the US transition into the next phase of the "Weimar" experiment will become all too obvious. Because once the abovementioned percentage hits 50%, it is game over.

Below Grice lays out the framework for the disinflation delusion that has permeated the minds of all economists to the point where divergence from the mean is now taken as gospel:

What drove the disinflation of the last thirty years? Politicians would say it was because they granted their central banks independence. But the pioneering experiment here didn’t take place until ten years into the disinflation, when the Reserve Bank of New Zealand Act 1989 gave that central bank the sole mandate to pursue price stability. Macroeconomists would site breakthroughs in our understanding. Except there haven’t been any. Today’s hard money/soft money debate is identical to the Monetarist/Keynesian debate of the 1970s, the US bimetallism agitation of the late 19th century, and the Currency vs Banking School controversy in the UK during the 1840s.Ireland is probably the best example of an entity for which the cognitive dissonance between an imaginary desired universe and a violent snapback to reality has finally manifested itself after a 30 year absence:

Was it the de-unionisation of the workforce? The quiescence of oil markets since the two extreme shocks of the 70s? The dumping of cheap labour from Eastern Europe, China and India onto the global labour market? Technology enhanced productivity growth? Or maybe it was just because the CPI numbers are so heavily manipulated?

Maybe it was all of these things. Maybe it was none of these things … for the little that it’s worth, my theory is that no-one has an adequate theory, other than it being down to the usual combination of luck and judgment on the part of policymakers … or about 150% luck. The problem is luck mean-reverts. The mammoth fiscal challenges (see chart below) currently being shirked by the US political class suggest that mean-reversion is imminent.

Ireland provides a good illustration. Today it’s going through a real and wrenching depression - there is no other word for it and it is heartbreaking to watch – partly because the terms of its bailout are so onerous. And what may well be the seeds of a future popular backlash against the euro can be detected in the election of Fine Gael on a ticket of renegotiating the bailout terms, which currently require them to pay a 5.8% rate of interest.Unlike Ireland, the US still has the luxury of being able to stick its head deep in the sand of denial.

Look at the following chart showing two hundred years or so of US government borrowing costs. Two hundred years is a lengthy period of time. There have been economic booms and financial panics, localized wars and world wars, empires have risen and empires have fallen, technological change has made each successive generation’s world unrecognizable from that which preceded it. Yet government yields have remained broadly mean-reverting (and the US has been one of the best run economies over that time – other governments’ bond yields demonstrate an unpleasant historic skew towards large numbers). Coincidentally enough, the average rate of interest over that period has been around 5.8%, the rate which the new Irish government today says is ‘crippling.’And here is the math that nobody in D.C. will ever dare touch with a ten foot pole as it will confirm beyond a reasonable doubt that the US is now well on its way to monetizing its future (read: not winning)

In other words, Ireland is so indebted that it is struggling to pay a rate of interest posterity would barely yawn at. But Ireland isn’t the only one.Take the US government, for example, which currently pays around 10% of its revenues on interest payments. This doesn’t sound too bad. The problem is that those federal government interest payments are calculated net of the coupons paid into federally run programs (e.g. social security) as these are deemed ‘intragovernment transfers.’ Yet those coupons to social security are made to fund a real obligation to American citizens and as such, represent payments on a real liability. On a gross basis the US government pays out 15% of its revenues on interest payments, which makes for less comfortable reading. So the net numbers remain the most widely quoted.And where the figure gets downright ugly is if one assumes that in order to find buyers for the $4 trillion in debt over the next two years (once the Fed supposedly is out of the picture after June 30), rates revert to the mean. Which they will. What happens next is a cointoss on whether or not we enter a Weimar-style debt crunch.

Suppose the US government had to pay the 5.8% yield it has paid on average over the last two hundred years? The share of revenues spent on gross interest payments would be a staggering 30% (see chart above). If it had to pay the 6.9% it’s paid on average since WW2, those gross interest payments would account for 37% of revenues. So it’s not difficult to see the potential for a dangerously self-reinforcing spiral of higher yields straining public finances, hurting confidence in the US governments’ ability to repay without inflating, leading to higher yields, etc.Lastly, Grice makes it all too clear why we are now all screwed, and no matter how many Bernanke dog and pony shows we have, the final outcome is not a matter of if but when.

America’s political class might arrest the trend which threatens their government’s solvency (chart below). They might find a palatable solution to the healthcare system’s chronic underfunding. They might defy Churchill’s quip, and skip straight to doing the right thing. But if they don’t, such a spiral becomes a question of when and not if. And what would the Fed do then? Bernanke says the Fed “will not allow inflation to get above low and stable levels.” He says it has learned the lessons of the 1970s. He’s read the books. He can recite the theory. Yet a lifetime reading books about the Great Depression (and writing a few) didn’t help him spot the greatest credit inflation since that catastrophe any more than reading “The Ten Habits of Highly Successful People” would make him successful. It’s the doing that counts. So before lending to the US government for 3.5% over ten years, bear in mind that when it comes to a real inflation fight, not one of the Fed economists you’re betting on has ever been in one.Our advice to the good doctor and his minions (not to mention all readers), is instead of reading multitudes of history books on the depression, on Japan, or on midget tossing (for those from the SEC), is to read one book. Just one. Link here.

from Bloomberg:

Barack Obama may lose the advantage of low borrowing costs as the U.S. Treasury Department says what it pays to service the national debt is poised to triple amid record budget deficits.

Interest expense will rise to 3.1 percent of gross domestic product by 2016, from 1.3 percent in 2010 with the government forecast to run cumulative deficits of more than $4 trillion through the end of 2015, according to page 23 of a 24-page presentation made to a 13-member committee of bond dealers and investors that meet quarterly with Treasury officials.

While some of the lowest borrowing costs on record have helped the economy recover from its worst financial crisis since the Great Depression, bond yields are now rising as growth resumes. Net interest expense will triple to an all-time high of $554 billion in 2015 from $185 billion in 2010, according to the Obama administration’s adjusted 2011 budget.

“It’s a slow train wreck coming and we all know it’s going to happen,” said Bret Barker, an interest-rate analyst at Los Angeles-based TCW Group Inc., which manages about $115 billion in assets. “It’s just a question of whether we want to deal with it. There are huge structural changes that have to go on with this economy.”

The amount of marketable U.S. government debt outstanding has risen to $8.96 trillion from $5.8 trillion at the end of 2008, according to the Treasury Department. Debt-service costs will climb to 82 percent of the $757 billion shortfall projected for 2016 from about 12 percent in last year’s deficit, according to the budget projections.

The famous quote attributed to John Maynard Keynes - "the market can remain irrational longer than you can remain solvent" - is a favorite of speculators here. Actually, I very much agree with this observation, provided that it is correctly understood. Solvency is always a function of debt, and it's extremely important for investors to recognize that when you take investment positions by borrowing on margin, you'd better use stop-losses, because the debt obligation stays intact even if the investment values decline.

This printing money is going to lead to huge trouble. It’s going to lead to higher interest rates. It’s going to lead to more inflation and at some point there is going to be a train wreck in the currency and the bond market." Market commentator and money manager Bill Fleckenstein

fantastic from Zero Hedge:

Rich Bernstein who while at BofA used to be one of the few (mostly) objective voices, today got into a heated discussion with Rick Santelli over yield curves and what they portend. In a nutshell, Bernstein's argument was that a steep yield curve is good for the economy, and the only thing that investors have to watch out for is an inversion. Yet what Bernstein knows all too well, is that in a time of -7% Taylor implied rates, QE 1, Lite, 2, 3, 4, 5, LSAPs, no rate hikes for the next 3 years, and all other possible gizmos thrown out to keep the front end at zero (as they can not be negative for now), to claim that the yield curve in a time of central planning, is indicative of anything is beyond childish. A flat curve, let alone an inverted curve is impossible as this point: all the Fed has to do is announce it will be explaining its Bill purchases and watch the sub 1 Year yields plunge to zero. Yet the long-end of the curve in a time of Fed intervention is entirely a function of the view on how well the Fed can handle its central planning role: after all, the last thing the Fed wants is a 30 year mortgage that is 5%+ as that destroys net worth far faster than the S&P hitting the magic Laszlo number of 2,830 or whatever it was that Birinyi pulled out of his ruler. As such, Santelli's warning that a steep curve during POMO times is just as much as indication of stagflation as growth, is spot on.

Furthermore, to Bernstein's childish argument of "where is the stagflation" maybe he should take a look at commodity prices, unemployment levels and double dipping home prices, and the answer will suddenly become self evident. But either way, the point is that during central planning the shape of the curve does not matter at all, and certainly not to banks. The traditional argument that banks make more money on the long end breaks down when nobody is borrowing on the long-end, and with mortgage apps, both new and refi, plunging to fresh lows, that is precisely what is happening. But who cares about facts: all one has to do is roll one's eyes and smile flirtatiously at Becky Quick (making sure of course that Warren is nowhere to be found).

The video of the argument between the two is below:

Regardless, while Bernstein's objectivity is now sadly very much under question, if understandably so as his new business requires a bullish outlook no matter what, here is a primer on curves that was posted on Zero Hedge previously for all those who may have been confused by today's debate.

Posted on Zero Hedge in June 2010:

Why the Yield Curve May Not Predict the Next Recession, and What Might

The interest rates for more distant maturities are normally higher the further out in time. Why? First, because lenders fear a depreciating monetary unit: price inflation. To compensate themselves for this expected (normal) falling purchasing power, they demand a higher return. Second, the risk of default increases the longer the debt has to mature.

In unique circumstances for short periods of time, the yield curve inverts. An inverted yield occurs when the rate for 3-month debt is higher than the rates for longer terms of debt, all the way to 30-year bonds. The most significant rates are the 3-month rate and the 30-year rate.

The reasons why the yield curve rarely inverts are simple: there is always price inflation in the United States. The last time there was a year of deflation was 1955, and it was itself an anomaly. Second, there is no way to escape the risk of default. This risk is growing ever-higher because of the off-budget liabilities of the U.S. government: Social Security, Medicare, and ERISA (defaulting private insurance plans that are insured by the U.S. government).

What does an inverted yield curve indicate? This: the expected end of a period of high monetary inflation by the central bank, which had lowered short-term interest rates because of a greater supply of newly created funds to borrow.

This monetary inflation has misallocated capital: business expansion that was not justified by the actual supply of loanable capital (savings), but which businessmen thought was justified because of the artificially low rate of interest (central bank money). Now the truth becomes apparent in the debt markets. Businesses will have to cut back on their expansion because of rising short-term rates: a liquidity shortage. They will begin to sustain losses. The yield curve therefore inverts in advance.

On the demand side, borrowers now become so desperate for a loan that they are willing to pay more for a 90-day loan than a 30-year, locked in-loan.

On the supply side, lenders become so fearful about the short-term state of the economy -- a recession, which lowers interest rates as the economy sinks -- that they are willing to forego the inflation premium that they normally demand from borrowers. They lock in today's long-term rates by buying bonds, which in turn lowers the rate even further.

An inverted yield curve is therefore produced by fear: business borrowers' fears of not being able to finish their on-line capital construction projects and lenders' fears of a recession, with its falling interest rates and a falling stock market.

Our 'Daily Growth Index' represents the average 'growth' value of our 'Weighted Composite Index' over a trailing 91-day 'quarter', and it is intended to be a daily proxy for the 'demand' side of the economy's GDP. Over the last 60 days that index has been slowly dropping, and it has now surpassed a 2% year-over-year rate of contraction.

The downturn over the past week has emphasized the lack of a clearly formed bottom in this most recent episode of consumer 'demand' contraction. Compared with similar contraction events of 2006 and 2008, the current 2010 contraction is still tracking the mildest course, but unlike the other two it has now progressed over 140 days without an identifiable bottom.

As we have mentioned before, this pattern is unique and unlike the 'V' shaped recovery (or even the 'W' shaped double-dip) that many had expected. From our perspective the unique pattern is more interesting than the simple fact of an ongoing contraction event. At best the pattern suggests an extended but mild slowdown in the recovery process. But at worse the pattern may be the early signs of a structural change in the economy.

[I]t has instead, unfolded so far as a mild but persistent kind of

contraction, more like a 'walking pneumonia' that keeps things miserable for an

extended period of time.

When bond investors expect the economy to hum along at normal rates of growth without significant changes in inflation rates or available capital, the yield curve slopes gently upward. In the absence of economic disruptions, investors who risk their money for longer periods expect to get a bigger reward -- in the form of higher interest -- than those who risk their money for shorter time periods. Thus, as maturities lengthen, interest rates get progressively higher and the curve goes up.

When bond investors expect the economy to hum along at normal rates of growth without significant changes in inflation rates or available capital, the yield curve slopes gently upward. In the absence of economic disruptions, investors who risk their money for longer periods expect to get a bigger reward -- in the form of higher interest -- than those who risk their money for shorter time periods. Thus, as maturities lengthen, interest rates get progressively higher and the curve goes up. Typically the yield on 30-year Treasury bonds is three percentage points above the yield on three-month Treasury bills. When it gets wider than that -- and the slope of the yield curve increases sharply -- long-term bond holders are sending a message that they think the economy will improve quickly in the future.

Typically the yield on 30-year Treasury bonds is three percentage points above the yield on three-month Treasury bills. When it gets wider than that -- and the slope of the yield curve increases sharply -- long-term bond holders are sending a message that they think the economy will improve quickly in the future. In April, 1992, the spread between short- and long-term rates was five percentage points, indicating that bond investors were anticipating a strong economy in the future and had bid up long-term rates. They were right. As the GDP chart above shows, the economy was expanding at 3% a year by 1993. By October 1994, short-term interest rates (which slumped to 20-year lows right after the 1991 recession) had jumped two percentage points, flattening the curve into a more normal shape.

In April, 1992, the spread between short- and long-term rates was five percentage points, indicating that bond investors were anticipating a strong economy in the future and had bid up long-term rates. They were right. As the GDP chart above shows, the economy was expanding at 3% a year by 1993. By October 1994, short-term interest rates (which slumped to 20-year lows right after the 1991 recession) had jumped two percentage points, flattening the curve into a more normal shape. At first glance an inverted yield curve seems like a paradox. Why would long-term investors settle for lower yields while short-term investors take so much less risk?

At first glance an inverted yield curve seems like a paradox. Why would long-term investors settle for lower yields while short-term investors take so much less risk? As is usually the case, the collective market instinct was right. Check out the GDP chart above; it aptly demonstrates just how bad things got. Interest rates fell dramatically for the next five years as the economy tanked. Thirty year bond yields went from 14% to 7% while short-term rates, starting much higher at 15% fell to 5% or 6%. As for equities, the next year was brutal (see chart below). Long-term investors who bought at 10% definitely had the last laugh.

As is usually the case, the collective market instinct was right. Check out the GDP chart above; it aptly demonstrates just how bad things got. Interest rates fell dramatically for the next five years as the economy tanked. Thirty year bond yields went from 14% to 7% while short-term rates, starting much higher at 15% fell to 5% or 6%. As for equities, the next year was brutal (see chart below). Long-term investors who bought at 10% definitely had the last laugh. To become inverted, the yield curve must pass through a period where long-term yields are the same as short-term rates. When that happens the shape will appear to be flat or, more commonly, a little raised in the middle.

To become inverted, the yield curve must pass through a period where long-term yields are the same as short-term rates. When that happens the shape will appear to be flat or, more commonly, a little raised in the middle. That's what happened in 1989. Thirty-year bond yields were less than three-year yields for about five months. The curve then straightened out and began to look more normal at the beginning of 1990. False alarm? Not at all. A glance at the GDP chart above shows that the economy sagged in June and fell into recession in 1991.

That's what happened in 1989. Thirty-year bond yields were less than three-year yields for about five months. The curve then straightened out and began to look more normal at the beginning of 1990. False alarm? Not at all. A glance at the GDP chart above shows that the economy sagged in June and fell into recession in 1991.

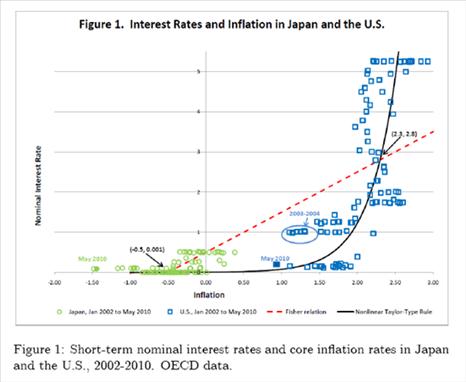

The benchmark 10-year Treasury yield will drop below 2% for the first time ever over the next 12 months as US economic growth loses traction, said David Rosenberg, a high profile economist and one of the biggest bond bulls on Wall Street.

The Federal Reserve is running the risk of replaying the disaster movie that led to the credit crisis by keeping monetary policy loose for too long, Stephen Roach, non-executive chairman at Morgan Stanley, told CNBC Tuesday.

by Bill Hester: