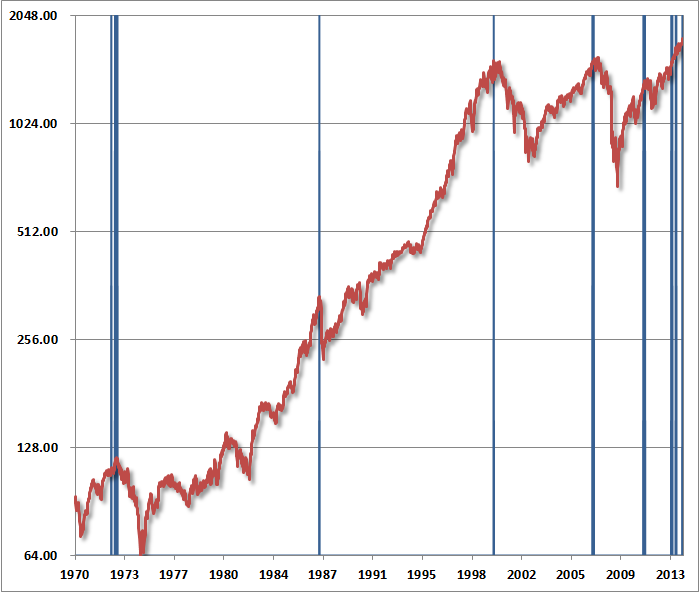

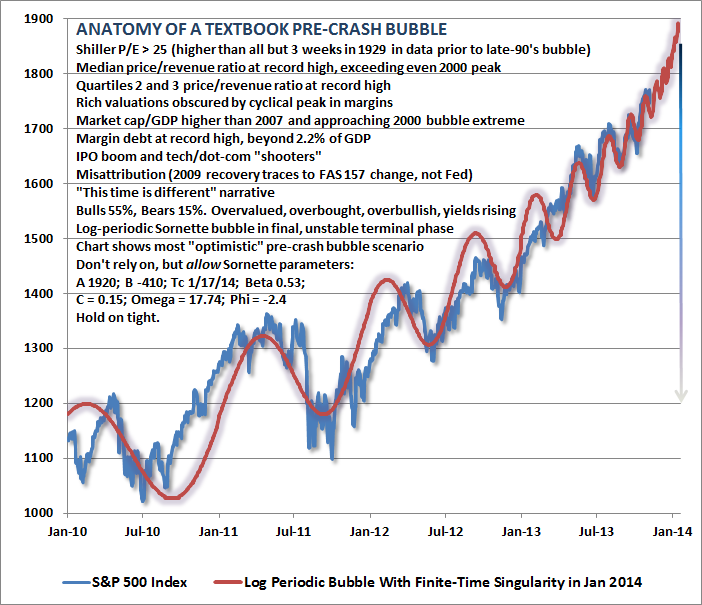

Stocks climb still higher into the Bubble Belt on promises by the new Fed QEeen, Calamity Janet Yellen, that she will continue the Fed's debt roulette indefinitely!

Stocks climb still higher into the Bubble Belt on promises by the new Fed QEeen, Calamity Janet Yellen, that she will continue the Fed's debt roulette indefinitely!

from Zero Hedge:

While chart analogs provide optically pleasing (and often far too

shockingly correct) indications of the human herd tendencies towards

fear and greed, a glance through the headlines and reporting of prior

periods can provide just as much of a concerning 'analog' as any chart.

In this case, while these 3 pictures can paint a thousand words;

a thousand words may also paint the biggest picture of all. It seems,

socially and empirically, it is never different this time as these 1936 Wall Street Journal archives read only too well... from

devaluations lifting stocks to inflationary side-effects of money flow

and from short-covering, money-on-the-sidelines, Jobs, Europe,

low-volume ramps, BTFD, and profit-taking, to brokers advising stocks

for the long-run before a 40% decline.

Stocks look eerily similar...

Income inequality has ramped back to the same levels...

and Rates look awfully similar.... (h/t @Not_Jim_Cramer)

and that didn't end well... (War!)

But when we look at the headlines in the Wall Street Journal from mid

1936 to mid 1937 as the market topped out, dipped, was bought back

(orange oval), then collapsed 40% in 3 months, nothing ever changes...

Government Bailouts Repaid - Bullish Implications...

The Buying Is Not Speculation - Cash On The Sidelines...N.Y. Central Has Repaid All Government Loans

The Wall Street Journal, 978 words

Dec 1, 1936

WASHINGTON Numerous railroad developments here yesterday were climaxed by the announcement of RFC Chairman Jesse H. Jones that New York Central had repaid all of its government loans, totaling $16,858,950, most of which was not due until 1941.

Inflationary Side-Effects - Buy It All It's Going Up...It's Cash Bull Market With Little Inflation, Says Exchange Bulletin

The Wall Street Journal, 169 words

Dec 16, 1936

"This is eminently a cash market, and as such is relatively devoid of that major characteristic of speculative inflation, the use of borrowed money." says the December Bulletin of the N.Y. Stock Exchange.

As Goes The US So Goes The Rest Of The World...Wheat Prices Soar To 7-Year Highs On Heavy Buying Stimulated by Broad Advances in Foreign Pits

The Wall Street Journal, 1497 words

Dec 19, 1936

CHICAGO An avalanche of buying, encouraged by buoyancy in foreign markets, particularly in Winnipeg, swept wheat prices to the highest levels since December, 1929, Friday.

But... 3 days before...

The Wall Street Journal, 1027 words

Dec 16, 1936

As commodity prices continued to advance yesterday to the accompaniment of increasing public speculation in futures markets, signs of a feeling of caution appeared from widely separated centers.

Global Economy To Lift Stocks...London Trade Stimulated By Wall Street Strength; Averages at New Highs

The Wall Street Journal, 859 words

Nov 6, 1936

LONDON Overnight strength in Wall Street considerably stimulated the stock market yesterday. Dealers again arrived earlier than usual in anticipation of activity in international issues and found large buying orders in these stocks awaiting execution.

Devaluation Always A Winner... (Market Prices Prove Economy Likes It)London, New York Stock Transactions Largest in Months - British Brokers Stand in Queues to Fill Orders Activity Ascribed to World Efforts to Revive Trade

The Wall Street Journal, 956 words

Oct 8, 1936

Growing realization that the determined international effort now being made to sweep away trade barriers will be followed by improved business conditions throughout the world brought a rush of business to the security markets in New York and London yesterday such as not been seen for months.

Equity Valuations Irrelevant...Wall Street Weighs Devaluation Effects On U.S. Markets; Sees Little Likelihood of Dumping

The Wall Street Journal, 1759 words

Sep 28, 1936

Rising security and commodity markets Saturday gave ample indication of the financial district's "bullish" interpretation of the U.S. Anglo-French monetary agreement.

Markets Cheerful Over Devaluation; Morgenthau Not Afraid of Dumping

Selective Buying Here and Abroad Motors and Other Shares Held To Benefit From Improved World Trade Are Strong Commodities Less Responsive International Markets

The Wall Street Journal, 1726 words

Sep 29, 1936

A note of cautious optimism was sounded by leading stock exchanges of the world which were open for business yesterday.

Europe Ever The Optimist Even In The Face Of Dismal Reality...Earnings Yield of 15 Stocks 4.8%, Compared with 9.4% Ten Years Ago

The Wall Street Journal, 1280 words

Aug 7, 1936

Industrial earning power is valued nearly twice as highly in the current stock market as it was ten years ago.

Short Covering As Ever...France Optimistic Despite Continuing European Tension - Growing Franco-English Cooperation Inspires Confidence

The Wall Street Journal, 652 words

Dec 5, 1936

Despite the unabated international tension and sudden menace of a constitutional crisis in Great Britain, the continuance of quarrels between Right and Left wings of the Popular Front, and the persistent antagonism between employers and labor, the general feeling in France is rather optimistic than pessimistic.

Government Spending Cuts Cause Concern...Active Short Covering Sweeps Grain Prices To New High Levels - Chases Bears

The Wall Street Journal, 1345 words

Dec 2, 1936

New highs for the season were recorded in wheat, corn, rye and oats Tuesday. Spot red winter wheat advanced to the highest level since February, 1929. The sharp upturn, which boosted December corn almost 5 cents, and December wheat about 3 cents, was due principally to short covering by those made uneasy over the sale of an unusually large quantity of spot wheat out of local store, and by generous snowfall over the grain belt. Early in the session the market ruled easy on reports of rain and snow, and predictions for continued unsettled weather.

States And Taxes...Sabotaging Federal Economy

The Wall Street Journal, 412 words

Dec 5, 1936

Even the modest beginning which is attempted by WPA officials to reduce cost of government by cutting down the relief roles is encountering strong opposition. It is perhaps only natural that the workers themselves should object, although their methods of protesting through "sitdown" strikes, not to mention the violence which has manifested itself, may be open to question. But much more ...

The Foreign Money Will Save Us...Sales Tax Repeal May Unbalance Kentucky Finances

The Wall Street Journal, 1002 words

Jan 14, 1936

LOUISVILLE, Ky.--Repeal of Kentucky's 3% sales tax, effective the moment Governor Albert B. Chandler signs it, probably Wednesday will deprive the state of $3,500,000 of revenue budgeted to the expiration of the biennium ending June 30, 1936 and the counties of $1,750,000.

Money On The Sidelines...Financial Centers Expect Greater Foreign Interest in Our Securities As Congress Delays Alien Tax Boost - Foreign Interest Here

The Wall Street Journal, 765 words

Aug 6, 1937

Some resumption of foreign interest...

Jobs And Europe never far from fear...The Wall Street Journal, 590 words

Jul 1, 1937

While the Street remains in a cautious frame of mind, there are undoubtedly more possible buyers than sellers around, and it would not take a lot of encouragement to get these gentlemen aboard. Feeling in brokerage circles is that stocks are more likely to advance on any break in the unpleasant headlines these days than to decline far on a continuation of current uncertainties.

Buy The F##king Dip...The Wall Street Journal, 683 words

Jun 29, 1937

Certainly the market was more active on the downside, which surprised a lot of traders who had expected otherwise. The labor and foreign situations remain the main factors in the picture, and brokers feel that these have not changed one whit for the better thus far.

Rallies had Real Volume Then - No Low Volume Ramps...The Wall Street Journal, 508 words

Aug 24, 1937

A rather depressed feeling is extant in Wall Street as small volume and lower prices continue. Yet there are not many bears in the Street so far as the long pull is concerned. Traders still are stubborn in their theory that stocks are reactionary at the moment from lack of interest rather than any important liquidation. This is the period of the year when business takes a final breathing spell before the more active Fall and some think the stock market is doing likewise and that better days are ahead.

And At The Top... Brokers Suggest Stocks For The Long-Run (based on 'expectations')The Wall Street Journal, 564 words

Aug 16, 1937

If Saturday's volume was any indication, revived interest in the stock market is here in the opinion of the Street. Furthermore the scope of trading Friday and Saturday indicated a broadening interest which included medium priced as well as low priced issues on contrast to the extended period wherein so-called "quality" stocks held sway in a limited market with small volume.

See - it really is never different this time. It merely appears so since - as Kyle Bass so eloquently noted, the brevity of financial memory is about two years...The Wall Street Journal, 665 words

Aug 7, 1937

Profit taking for the week-end brought prices down in yesterday's market, but the undertone remained steady and brokers said there was nothing important in the character of the selling. Many houses were advising the purchase of favored issues on any further reactions. Metal shares ended the day with advances in many cases. There was impressive buying reported in the copper issues largely for long pull purposes.

The Wall Street Journal, 649 words

Aug 10, 1937

While volume left much to be desired, the expectation of stronger and more active markets continued to pervade Wall Street. Moreover, the general business picture is regarded as more pleasing than at any time since the so-called Summer "lull" came into force. Incidentally, the seasonal letdown thus far has not proved to be as extensive as many predicted and expected. Brokers say that many clients are away and that there are others who will be replacing their sold-out long positions in coming weeks.

This man is the most brilliant mind in economics today. God bless him!

Investors who believe that history has lessons to

teach should take our present concerns with significant weight, but

should also recognize that tendencies that repeatedly prove reliable

over complete market cycles are sometimes defied over portions of those

cycles. Meanwhile, investors who are convinced that this time is

different can ignore what follows. The primary reason not to listen to a

word of it is that similar concerns, particularly since late-2011,

have been followed by yet further market gains. If one places full

weight on this recent period, and no weight on history, it follows that

stocks can only advance forever.

Three cheers for John Mauldin. He's asking the questions that Congress should be asking! I love this man!

The Fed's Dilemma

Conveniently, Ray Dalio and his team at Bridgewater penned an

essay this week highlighting the Fed's dilemma. I offer a few key

paragraphs and a chart or two as a setup to my list of questions.

Turning right to their very prescient comments:

In the old days central banks moved interest rates to run

monetary policy. By watching the flows, we could see how lowering

interest rates stimulated the economy by 1) reducing debt service

burdens which improved cash flows and spending, 2) making it easier to

buy items marked on credit because the monthly payments declined, which

raised demand (initially for interest rate sensitive items like durable

goods and housing) and 3) producing a positive wealth effect because the

lower interest rate would raise the present value of most investment

assets (and we saw how raising interest rates has had the opposite

effect).

All that changed when interest rates hit 0%; "printing money"

(QE) replaced interest-rate changes. Because central banks can only buy

financial assets, quantitative easing drove up the prices of financial

assets and did not have as broad of an effect on the economy. The Fed's

ability to stimulate the economy became increasingly reliant on those

who experience the increased wealth trickling it down to spending and

incomes, which happened in decreasing degrees (for logical reasons,

given who owned the assets and their decreasing marginal propensities to

consume). As shown in the charts below, the marginal effects of wealth

increases on economic activity have been declining significantly. The

Fed's dilemma is that its policy is creating a financial market bubble

that is large relative to the pickup in the economy that it is

producing. If it were targeting asset prices, it would tighten monetary

policy to curtail the emerging bubble, whereas if it were

targeting economic conditions, it would have a slight easing bias. In

other words, 1) the Fed is faced with a difficult choice, and 2) it is

losing its effectiveness."

(In the following charts HH stands for "Household.")

We expect this limit to worsen. As the Fed pushes asset prices

higher and prospective asset returns lower, and cash yields can't

decline, the spread between the prospective returns of risky assets and

those of safe assets (i.e. risk premia) will shrink at the same time as

the riskiness of risky assets will not decline, changing the

reward-to-risk ratio in a way that will make it more difficult to push

asset prices higher and create a wealth effect. Said differently, at

higher prices and lower expected returns the compensation for taking

risk will be too small to get investors to bid prices up and drive

prospective returns down further. If that were to happen, it would

become difficult for the Fed to produce much more of a wealth effect. If

that were the case at the same time as the trickling down of the wealth

effect to spending continues to diminish, which seems likely, the Fed's

power to affect the economy would be greatly reduced.

What Would Yellen Do?

With that as a setup, let's turn to our hypothetical hearing.

(Insert a picture of your favorite senator here.) With the hope that we

will get a glimpse of what a Janet Yellen chairmanship of the Fed will

actually look like, let's think about what we would like to know:

Vice-Chairman Yellen, thank you for agreeing to attend this

hearing. We have already interviewed you extensively for your present

position, so I believe that most members of the committee and Senate

already believe that you are qualified to be chairperson. Therefore I

would like to use this opportunity to learn a little more about the

thinking that goes on with regard to Federal Reserve monetary policy. In

the spirit of the transparency that has been a hallmark of the Bernanke

Federal Reserve, I would like you to shed a little light on the

thinking and philosophy that will guide the Federal Reserve under the

chairmanship of Janet Yellen. Here are a few questions that I believe we

would all like answers to.