Free checking, a banking mainstay of the last decade, could soon go the way of free toasters for new account holders. Banks are already moving to make up the revenue they will lose on lower overdraft and debit card transaction charges by raising fees on other services.

Banks like Wells Fargo, Regions Financial of Alabama and Fifth Third of Ohio, for instance, recently began charging new customers a monthly maintenance fee of $2 to $15 a month — as much as $180 a year — on the most basic accounts. Even TCF Financial of Minnesota, whose marketing mantra championed “totally free checking,” started imposing fees this year in anticipation of the new rules.

To be sure, in many cases customers can escape the new checking account charges by maintaining a minimum balance or by using other banking services, like direct deposit for paychecks and signing up for a debit card.

Still, with checking account fees spreading, Bank of America rolled out a fee-free, bare-bones account on Wednesday, the eve of the Senate vote. The catch? To avoid any charges, customers must forgo using tellers at their local branch, use only Bank of America cash machines, and opt to receive only online statements.

Friday, July 16, 2010

Thanks, Congress, for Higher Bank Fees!

Insights on Contango

from EconomPic blog:

FT Alphaville with a great post "Is ‘cash for commodity’ the biggest trade in town?" explaining why commodity curves are in contango (demand from passive indexers) and the benefit to producers (a cheap source of financing). I have been sitting on the below post explaining how this translates into an investment in a passive commodity strategy (hint... not good) so I thought the time was right to finally post it.

Wikipedia explains roll yield, so I don't have to:

The roll yield is the yield that a futures investor captures when their futures contract converges (or rolls up) to the spot price in a backwardated futures market. The spot price can stay constant, but the investor will still earn returns from buying discounted futures contracts, which continuously roll up to the constant spot price.Said another way, backwardation means the futures price is below the current spot price (i.e. the curve is downward sloping), thus the investor gaining exposure via futures will outperform the underlying spot market (all else equal). Contango means the exact opposite situation (this was explained recently regarding the VIX ETN VXX in the EconomPic post When ETNs Attack). In addition, as explained by FT Alphaville, this negative drag is the "subsidized financing" received by commodity producers "selling" their commodities in the futures market.

Note that in case of a market in contango, the roll yield is negative - since the price of the futures contract trades higher than the spot price, and rolls down to converge towards the spot price.

How much of an impact does this have? Let's take a look at the impact via the excess roll yield of the S&P GSCI Commodity Index futures vs. spot.

As can be seen above, the futures market has consistently underperformed the spot market since mid-2004. By how much?

A lot...

A Few Key Trading Principles

I own Mark Douglas' book. Great book!

from CrossHairs Trader blog;

What you are about to read has the ability to change your stock trading results for the better. No. I am not going to share with you some kind of “secret” indicator or some guru’s prediction. What I am going to share with you is how to properly approach the trading game where rules and the proper mind-set can help propel the average trader to above average ranks. I am enlisting the help of Mark Douglas, who I believe has written the one of the best books on the psychology of successful trading. In his book, Trading In the Zone, Douglas discusses how a trader can begin to eliminate the emotional risk of trading via a probabilistic mind-set. A probabilistic mind-set is essential to understanding the market because the market is “always communicating in probabilities.” In other words, the market does not speak Chinese, English, Russian, or bullish or bearish…it speaks probability. If we plan on living in China we need to learn Chinese, if Russia then Russian. If we plan on making a living in the market then we need to learn the language of probability. A probabilistic mind-set consists of internalizing the following fundamental truths:

1. Anything can happen. Or as I like to say, anything can happen…and often does. Usually the market does the exact opposite of what we think it should do and when we begin to doubt the market it does exactly what we once thought it should do. Get it?

2. You don’t need to know what is going to happen next in order to make money. Trading is not about being right in our arrogant predictions, it is about making money. We are never going to be able to predict what will happen next either in the market or in life so let’s just get over it once and for all.

3. There is a random distribution between wins and losses for any given set of variables that define an edge. Trading is like tossing a coin: we can five wins in a row or five losses; we could win one lose one. Wins and losses are random so do not bet the farm or the crops.

4. An edge is nothing more than an indication of a higher probability of one thing happening over another. Call it what we will but if we have a system, a methodology, a strategy, an edge for locating a trade then we have found an indication of a high probability circumstance that has been historically proven to repeat itself over and over again and will probably do so in the future.

5. Every moment in the market is unique. No matter how many times we have traded an edge the outcome can be different this time and no matter how perfectly matched this pattern is with the last one, this one is truly unique if for no other reason than in this market the participants are not the same as in the last one. The market is too diverse and too fluid to be put in a box, wrapped up and sold to the next consumer.

If we learn the language of the stock market we can understand how to make money. Until then it may just be all Greek to us!

U.S. Debt Sinking the Dollar

from Ambrose Evans-Pritchard:

The euro rocketed to a two-month high of $1.29 and sterling jumped two cents to almost $1.54 after the Fed confessed that the US economy may not recover for five or six years. Far from winding down emergency stimulus, the bank may need a fresh blast of bond purchases or quantitative easing.

The euro rocketed to a two-month high of $1.29 and sterling jumped two cents to almost $1.54 after the Fed confessed that the US economy may not recover for five or six years. Far from winding down emergency stimulus, the bank may need a fresh blast of bond purchases or quantitative easing.

Usually the dollar serves as a safe haven whenever the world takes fright, and there was plenty of sobering news from China and other quarters on Thursday. Not this time. The US itself has become the problem.

"The worm is turning," said David Bloom, currency chief at HSBC. "We're in a world of rotating sovereign crises. The market seems to become obsessed with one idea at a time, then violently swings towards another. People thought the euro would break-up. Now we're moving into a new phase because we're hearing alarm bells of a US double dip."

Mr Bloom said a deep change is under way in investor psychology as funds and central banks respond to the blizzard of shocking US data and again focus on the fragility of an economy where public debt is surging towards 100pc of GDP, not helped by the malaise enveloping the Obama White House. "The Europeans have aired their dirty debt in public and taken some measures to address it, whilst the US has not," he said.

The Fed minutes warned of "significant downside risks" and a possible slide into deflation, an admission that zero interest rates, $1.75 trillion of QE, and a fiscal deficit above 10pc of GDP have so far failed to lift the economy out of a structural slump.

"The Committee would need to consider whether further policy stimulus might become appropriate if the outlook were to worsen appreciably," it said. The economy might not regain its "longer-run path" until 2016.

"The Fed is throwing in the towel," said Gabriel Stein, of Lombard Street Research. "They are preparing to start QE again. This was predictable because the M3 broad money supply has been contracting for months."

The Fed minutes amount to a policy thunderbolt, evidence of how quickly the recovery has lost steam. Just weeks ago the Fed was mapping out withdrawal of stimulus.

Goldman Sachs said it expects the euro to rise to $1.35 by the end of the year. The yen will appreciate to ¥83, through the pain barrier for most of Japan's big exporters. The new twist is that SAFE, China's $2.4 trillion fund, has begun buying record amounts of Japanese bonds, a shift in reserve allocation away from the dollar.

The signs of a deep and sudden slowdown in the US are becoming ever clearer as the "sugar rush" from the Obama fiscal stimulus wears off and the inventory boost fades. California, Illinois and other states are cutting spending, tightening US fiscal policy by 0.8pc of GDP.

Thursday's plunge in the Philadelphia Fed's July index of new manufacturing orders to –4.3 suggests that the economy may have buckled abruptly, as it did in mid-2008. The Economic Cycle Research Institute's ECRI leading indicator has tumbled, reaching –8.3pc last week. This points to a sharp slowdown or recession within three months.

While US port data looked buoyant in June, the details were troubling. Outbound traffic from Long Beach fell from 139,000 containers in May to 116,000 in June. Shipments from Los Angeles fell from 161,000 to 155,000. This drop in exports is worsening the US trade deficit, eroding the dollar.

The US workforce has shrunk by a 1m over the past two months as discouraged jobless give up the hunt. Retail sales have fallen for the past two months. New homes sales crashed to 300,000 in May after tax credits ran out, the lowest since records began in 1963. Mortgage applications have fallen by 42pc to 13-year low since April. Paul Dales at Capital Economics said the "shadow inventory" of unsold properties has risen to 7.8m. "The double dip in housing has begun," he said.

Alcoa, CSX, Intel, and JP Morgan have reported good earnings, but they mostly did so in July 2008 just before their shares collapsed. Such earnings rarely catch turning points and can be a lagging indicator. Profits have been boosted in this cycle by cost-cutting, which is self-defeating for the economy as a whole.

The minutes confirm the Fed is split down the middle over QE. Fed watchers say the Board in Washington wants to be ready to launch another round of bond purchases if necessary, pushing the banks balance sheet from $2.4 trillion towards $5 trillion, but hawks at the regional banks are highly sceptical.

A study by the San Francisco Fed said the interest rates need to be –4.5pc to stabilise the economy under the Fed's "rule of thumb". Since this is impossible, massive QE needs to make up the difference.

Tim Congdon from International Monetary Research said the US authorities have botched policy response. "They are forcing banks to contract lending by raising their capital asset ratios. They have let M3 shrink by 1pc a month, as in the early 1930s. The solution is simple. The Fed must raise the level of deposits by purchasing bonds from the non-banking system as the Bank of England has done. They refuse to do it," he said.

"The worm is turning," said David Bloom, currency chief at HSBC. "We're in a world of rotating sovereign crises. The market seems to become obsessed with one idea at a time, then violently swings towards another. People thought the euro would break-up. Now we're moving into a new phase because we're hearing alarm bells of a US double dip."

Mr Bloom said a deep change is under way in investor psychology as funds and central banks respond to the blizzard of shocking US data and again focus on the fragility of an economy where public debt is surging towards 100pc of GDP, not helped by the malaise enveloping the Obama White House. "The Europeans have aired their dirty debt in public and taken some measures to address it, whilst the US has not," he said.

The Fed minutes warned of "significant downside risks" and a possible slide into deflation, an admission that zero interest rates, $1.75 trillion of QE, and a fiscal deficit above 10pc of GDP have so far failed to lift the economy out of a structural slump.

"The Committee would need to consider whether further policy stimulus might become appropriate if the outlook were to worsen appreciably," it said. The economy might not regain its "longer-run path" until 2016.

"The Fed is throwing in the towel," said Gabriel Stein, of Lombard Street Research. "They are preparing to start QE again. This was predictable because the M3 broad money supply has been contracting for months."

The Fed minutes amount to a policy thunderbolt, evidence of how quickly the recovery has lost steam. Just weeks ago the Fed was mapping out withdrawal of stimulus.

Goldman Sachs said it expects the euro to rise to $1.35 by the end of the year. The yen will appreciate to ¥83, through the pain barrier for most of Japan's big exporters. The new twist is that SAFE, China's $2.4 trillion fund, has begun buying record amounts of Japanese bonds, a shift in reserve allocation away from the dollar.

The signs of a deep and sudden slowdown in the US are becoming ever clearer as the "sugar rush" from the Obama fiscal stimulus wears off and the inventory boost fades. California, Illinois and other states are cutting spending, tightening US fiscal policy by 0.8pc of GDP.

Thursday's plunge in the Philadelphia Fed's July index of new manufacturing orders to –4.3 suggests that the economy may have buckled abruptly, as it did in mid-2008. The Economic Cycle Research Institute's ECRI leading indicator has tumbled, reaching –8.3pc last week. This points to a sharp slowdown or recession within three months.

While US port data looked buoyant in June, the details were troubling. Outbound traffic from Long Beach fell from 139,000 containers in May to 116,000 in June. Shipments from Los Angeles fell from 161,000 to 155,000. This drop in exports is worsening the US trade deficit, eroding the dollar.

The US workforce has shrunk by a 1m over the past two months as discouraged jobless give up the hunt. Retail sales have fallen for the past two months. New homes sales crashed to 300,000 in May after tax credits ran out, the lowest since records began in 1963. Mortgage applications have fallen by 42pc to 13-year low since April. Paul Dales at Capital Economics said the "shadow inventory" of unsold properties has risen to 7.8m. "The double dip in housing has begun," he said.

Alcoa, CSX, Intel, and JP Morgan have reported good earnings, but they mostly did so in July 2008 just before their shares collapsed. Such earnings rarely catch turning points and can be a lagging indicator. Profits have been boosted in this cycle by cost-cutting, which is self-defeating for the economy as a whole.

The minutes confirm the Fed is split down the middle over QE. Fed watchers say the Board in Washington wants to be ready to launch another round of bond purchases if necessary, pushing the banks balance sheet from $2.4 trillion towards $5 trillion, but hawks at the regional banks are highly sceptical.

A study by the San Francisco Fed said the interest rates need to be –4.5pc to stabilise the economy under the Fed's "rule of thumb". Since this is impossible, massive QE needs to make up the difference.

Tim Congdon from International Monetary Research said the US authorities have botched policy response. "They are forcing banks to contract lending by raising their capital asset ratios. They have let M3 shrink by 1pc a month, as in the early 1930s. The solution is simple. The Fed must raise the level of deposits by purchasing bonds from the non-banking system as the Bank of England has done. They refuse to do it," he said.

ECRI Plunges to -9.8%!

This is just a hair's breadth from calling for a new recession!

from Zero Hedge blog:

The ECRI Leading Economic Index just dropped to a fresh reading of 120.6 (flat from a previously revised 121.5 as the Columbia profs scramble to create at least a neutral inflection point): this is now a -9.8 drop, and based on empirical evidence presented previously by David Rosenberg, and also confirming all the macro economic data seen in the past two months, virtually assures that the US economy is now fully in a double dip recession scenario."It is one thing to slip to or fractionally below the zero line, but a -3.5% reading has only sent off two head-fakes in the past, while accurately foreshadowing seven recessions — with a three month lag. Keep your eye on the -10 threshold, for at that level, the economy has gone into recession … only 100% of the time (42 years of data)." We are there.

Complete collapse in the long-term chart:

Consumer Confidence Plunges

WASHINGTON (MarketWatch) -- U.S. consumer sentiment plummeted in early July, hitting the lowest level since August, according to media reports of a survey released Friday by Reuters and the University of Michigan. The UMich index fell to 66.5 in early July from 76 in late June. The June reading was the highest level in more than two years. The average level of the index is around 87. Economists surveyed by MarketWatch had expected a July reading of 74.3. A separate reading on consumer confidence also recently plunged, with consumers worried abut weak hiring and the economy.

Stock Go South In a Hurry As Consumer Confidence In Freefall!

Consumer Spending Slows

NEW YORK, July 16, 2010 /PRNewswire via COMTEX/ -- The Deloitte Consumer Spending Index (Index) declined in June for the second consecutive month, once again due to weakness in real wages and the housing market. The Index attempts to track consumer cash flow as an indicator of future consumer spending.

Treasuries Slow, China Reduces Holdings

WASHINGTON—Overall inflows into U.S. assets slowed in May, including from China, which cut its portfolio, Treasury Department data showed Friday.

China's holdings of Treasurys fell $32.5 billion to $867.7 billion, but maintained the top position among foreign countries.

Selling by China since late last year for four consecutive months raised some concerns that the largest creditor nation to the U.S. may be reducing its exposure to the dollar, but analysts said the move has partly reflected a portfolio rebalancing into longer-term U.S. securities. In the two months prior to May, China increased its holdings.

Signs of Exhaustion?

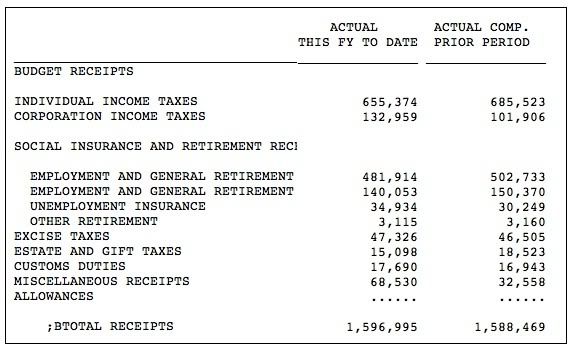

Federal Income Tax Recepts Still Falling

from Bizzy Blog:

It’s bad enough the federal government’s official budget deficit has topped $1 trillion for the second year in a row, according to the just-released June 2010 Monthly Treasury Statement. But, focusing only on receipts for the moment, a closer look makes it obvious that the situation is even worse than it appears. Don’t expect the establishment press to take any interest in the annoying but revealing details that follow.

Here is what Martin Crutsinger of the Associated Press wrote about federal collections in his Tuesday report on Uncle Sam’s current month and fiscal year deficit:

Through the first nine months of the current budget year, government revenues have totaled $1.6 trillion, up 0.5 percent from the same period a year ago.True enough, but look at the components:

Answer: Over $54 billion of it is from the Federal Reserve. As best I can tell, it represents dividends and interest on TARP lending and investments. This component of miscellaneous receipts is up by a factor of about 2.7 from fiscal 2009’s comparable year-to-date amount of $19.9 billion.

So the only reason receipts are up is that the Fed got into the direct lending and investment business. Tax collections that are indicators of the health of the overall economy are still down over last year, which was in turn down about 18% from the same period in fiscal 2008.

That’s not much comfort, is it?

Thursday, July 15, 2010

Foreclosures Reach New Record

July 15 (Reuters) - Banks repossessed a record number of U.S. homes in the second quarter, but slowed new foreclosure notices to manage distressed properties on the market, real estate data company RealtyTrac said on Thursday.

The root problems of job losses and wage cuts persist, making a sustained U.S. housing recovery elusive.

Banks took control of 269,962 properties in the second quarter, up 5 percent from the prior quarter and a 38 percent spike from the second quarter of last year, RealtyTrac said in its midyear 2010 foreclosure report.

Repossessions will likely top 1 million this year.

"The underlying conditions haven't improved," RealtyTrac senior vice president Rick Sharga said in an interview.

The housing market still grapples with "unemployment, economic displacement in general, and still sits on over 5 million seriously delinquent loans that in all likelihood will at some point go into foreclosure," he said.

In 2005, the last "normal" year in housing, Sharga said, about 530,000 households got a foreclosure notice and banks took over a comparatively minuscule 100,000 houses.

This year more than 3 million households are likely to get at least one foreclosure filing, which includes notice of default, scheduled auction and repossession, Irvine, California-based RealtyTrac forecasts.

In the first half of the year, foreclosure filings were made on 1.65 million properties. That was down 5 percent from the last half of 2009 but up 8 percent from the first half of last year.

One in every 78 households got at least one foreclosure filing in the first six months of this year.

Triple Dose of Bad Manufacturing News

WASHINGTON (MarketWatch) -- The manufacturing sector, which has been the strength of the U.S. economy, is slowing down, according to three separate reports released by the Federal Reserve on Thursday.

The timeliest data show further weakening in July after manufacturing output fell in June for the first time in a year. "Economic growth continues to soften into the third quarter," wrote Neil Dutta, an economist for Bank of America's Merrill Lynch.

U.S. stock markets were down about 0.8% after the Philadelphia Federal Reserve Bank said the Philly Fed manufacturing sentiment survey declined to 5.1 in July from 8 in June and 21.4 in May. The reading is above zero, which shows the sector is still expanding, but the breadth of that expansion has diminished.

Economists surveyed by MarketWatch were expecting a small gain in the Philly Fed to 10 in July. See our complete economic calendar.

The Empire state index from the New York Fed also fell to 5.1 in July from 19.6 in June, compared with expectations of a drop to 19.

"Today's U.S. reports revealed a remarkably weak round of July sentiment readings from both the New York and Philly Fed surveys that trumped the surprisingly firm round of industrial production figures for June, to leave a market focused on the slowing in the U.S. factory sector as we pass the mid-year mark," wrote analysts for Action Economics.

The details of the Philly Fed report were "particularly negative," wrote Steven Wieting, an economist for Citigroup Global Markets. The new-orders index fell to negative 4.3 from 9, its first negative reading in 12 months. The shipments index slowed to 4 from 14.2.

Finance Reform Bill Empowers Unions and Environmentalists, Advances Progressive Agenda, Hiring Quotas

The financial reform bill expected to clear Congress this week is chock-full of provisions that have little to do with the financial crisis but cater to the long-standing agendas of labor unions and other Democratic interest groups.

Principal among them is a measure to make it easier for unions, environmental groups and other activist organizations that hold shares to put their representatives on the boards of directors of every corporation in the United States.

The so-called "proxy access" provision, which activist groups say they will use to try to improve oversight of corporate financial practices, has provoked a backlash from the Business Roundtable, U.S. Chamber of Commerce and other major non-Wall Street business groups.

"This legislation includes provisions totally unrelated to the financial crisis which may disrupt Americas fragile economic recovery" and lead to increasing political battles in the boardrooms, said John J. Castellani, president of the roundtable.

Business groups are also rankled that the legislation would impose costly new burdens on airlines, utilities and other non-financial businesses that were victims rather than villains in the crisis, simply because they use financial derivatives to hedge their businesses against risks such as fluctuations in oil prices, interest rates and currencies.

Such hedging practices played no role in the crisis, though they helped many businesses weather the financial turbulence and recession that followed in the aftermath of the Wall Street storm.

Other provisions of the financial legislation, which goes before the full Senate on Thursday for a vote and likely passage, favor Democratic constituencies directly by requiring banks and federal agencies to hire and do more business with them.

The bill would create more than 20 "offices of minority and women inclusion" at the Treasury, Federal Reserve and other government agencies, to ensure they employ more women and minorities and grant more federal contracts to more women- and minority-owned businesses.

The agencies also would apply "fair employment tests" to the banks and other financial institutions they regulate, though their hiring and contracting practices had little or nothing to do with the 2008 financial crisis.

"The interjection of racial and gender preferences into America's financial sector deserves greater media exposure" before Congress debates and passes the massive 2,400-page bill, said Kevin Mooney, a contributing editor for Americans for Limited Government's daily newsletter.

The powerful new consumer protection agency that is the centerpiece of the reform bill also would provide substantial employment opportunities and funding for Democratic and social-activist groups such as the Association of Community Organizers for Reform Now (ACORN), critics say.

Rather than focus on the abuses in the mortgage-lending market that led to the crisis, the new consumer agency would have broad-ranging powers to regulate and punish virtually any company that has a financial relationship with consumers - even those that had nothing to do with the crisis, said Sen. Richard C. Shelby, Alabama Republican.

Mr. Shelby, the ranking member of the Senate Banking, Housing and Urban Affairs Committee, sought to craft a more tailored role for the agency in weeks of negotiation over the Senate bill.

"During our negotiations on the consumer bureaucracy, my Democrat friends were not focused on the mortgage market. Their sights were set on the rest of the economy," he said. "The new bureaucracy is an enormous reach across virtually every segment of our economy, and a massive expansion of government influence in our daily financial lives."

Sen. Bob Corker, a Tennessee Republican who also sought to help write a bipartisan Senate bill more narrowly focused on the problems that led to the crisis, said he fears that an activist director of the consumer agency could use agency power to direct loans to favored constituencies, regardless of whether the loans are sound or pose risks to the banking system.

"This may sound a little far-fetched, but you can have the wrong person in this position - there's no board, there's really no check and balance - that you can imagine could use this organization to try to create social justice in the financial system," he said.

Like the corporate boardroom provisions, many of the activities within the reach of the new consumer agency had "absolutely nothing - zero - to do with the financial crisis," Mr. Corker said. "But this has become a Christmas tree for those kinds of things, because people realize it's something that's going to pass."

Manufacturing Weakens

NEW YORK (MarketWatch) -- U.S. stocks slid sharply Thursday, derailing a seven-day climb for the Dow industrials, as economic data illustrated a slowing recovery. The reports dimmed enthusiasm over strong earnings from financial powerhouse J.P. Morgan Chase & Co.

After seven consecutive sessions of gains, the Dow Jones Industrial Average (DOW:DJIA) fell more than 120 points, and was lately off 91 points, or 0.9%, at 10,275.37. All but one of the Dow's 30 components tallied losses, with Bank of America Corp. (NYSE:BAC) the greatest laggard, off 3.1%..The S&P 500 Index (MARKET:SPX) fell 10.32 points, or 1%, with financials weighing the most among its 10 industry groups, followed by the technology sector.

The Nasdaq Composite Index (NASDAQ:COMP) shed 22.59 points, or 1%, to 2,227.23.

On the New York Mercantile Exchange, gold futures rose modestly, up 80 cents to $1,207.80 an ounce, while crude-oil futures slid below $76 a barrel.

For every stock rising, more than four were falling on the New York Stock Exchange, where 222 million shares had traded as of 11:05 a.m. Eastern.

Regional manufacturing indexes in New York and Philadelphia fell in July, while a government report pointed to mild growth in industrial output across the country.

"Manufacturing has been the bright spot in this recovery but now it needs more clarity on end demand growth which is just not there," Peter Boockvar, equity strategist at Miller Tabak, wrote in an email.

Separately, the government reported initial claims for jobless benefits declined last week, but analysts attributed the drop largely to seasonal factors.

The first of the largest U.S. banks to report, J.P. Morgan said it earned $4.8 billion in the second quarter, which was better than Wall Street anticipated. CEO Jamie Dimon downplayed optimism, calling returns in the bank's consumer-lending business "unacceptable." See more on $1.5 billion cut in J.P. Morgan's loan loss reserves.

Philly Manufacturing Survey Sends Stocks Into Tailspin Despite Improved Jobless Claims

I must say I was shocked when initial jobless claims fell by the most in months, but stocks dropped. This was the likely cause. It looks like we may be putting in a bottom, however. The recent rally is looking a bit soggy now. We've also bounced lower off the 200-day moving average.

NEW YORK (MarketWatch) -- U.S. stocks furthered their fall on Thursday after another weak manufacturing report, this one from the Philadelphia region. The Dow Jones Industrial Average /quotes/comstock/10w!i:dji/delayed (DJIA 10,260, -107.09, -1.03%) fell 72.88 points to 10,293.84. The S&P 500 Index /quotes/comstock/21z!i1:in\x (SPX 1,083, -11.74, -1.07%) shed 8.71 points to 1,086.46. The Nasdaq Composite /quotes/comstock/10y!i:comp (COMP 2,225, -25.32, -1.13%) dropped 17.39 points to 2,232.45.

Wednesday, July 14, 2010

Another Sign of Debt Deflation

from LA TImes:

Battered by unemployment and tighter lending standards, the credit scores of millions of Americans are sinking to new lows.

About 25.5% of consumers — or 43.4 million people — had credit scores below 600 in April, according to FICO Inc. Historically, only about 15% of consumers — or 25.5 million — have had scores below that level, FICO said.

Those in the middle of the spectrum have also declined. Moderate credit scores, between 650 and 699, fell to 11.9% from a historical average of 15%.

Consumers with low credit scores will have increased difficulty obtaining credit cards and other loans, said Christian deRitis, director of credit analytics at Moody's Analytics.

"Until the labor market turns around, people will remain unable to pay bills," DeRitis said. "Lowered consumption will only add extra friction to the economy."

The calculation for FICO scores considers two factors: how consistently bills are paid and how much available credit is in use. Slow or delinquent payments and high amounts of debt result in lowered scores.

Hoisington 2Q Review, Forward Outlook

wSent out by John Mauldin. Hoisington Investment Management Company (www.hoisingtonmgt.com) is a registered investment advisor specializing in fixed income portfolios for large institutional clients. Located in Austin, Texas, the firm has over $4-billion under management, composed of corporate and public funds, foundations, endowments, Taft-Hartley funds, and insurance companies.

Has the Recession Really Ended?

Real GDP has improved for four consecutive quarters (2nd qtr. est.), albeit at a substandard pace following the steep decline in economic activity of the previous year and a half. An impressive recovery in business sales and industrial production has occurred. The responsibility for dating contractions and expansions in the U.S. economy rests with the cycle dating committee of the National Bureau of Economic Research (NBER). Thus far, the NBER has been unwilling to proclaim an end to the recession that started in late 2007. This may partially reflect the fact that the ratio of people employed to our total population has fallen from 62.7% in December 2007 to 58.5% today. Although the recent low in this measure was 58.2%, touched just a couple of months ago, our present level is no higher than it was in 1983. This measure is a proximate indication of our country's overall standard of living and interestingly over the last twenty years has declined as the U.S. economy has become more indebted (Chart 1). Although the four coincident indicators that the NBER utilizes in judging recession troughs have turned positive, two of them (income less transfer payments and employment) have only marginally shifted upwards and are subject to significant revisions. Thus, history may come to judge that the NBER was very wise to hold off making this end of recession call. Four major considerations suggest that the past several quarters may be nothing more than an interlude in a more sustained economic downturn, with further negative quarters still ahead. Such an outcome will suppress inflation further and quite possibly lead to deflation.

Four Major Impediments to Economic Normalcy

Deficit SpendingFirst, deficit spending is not conducive to sustained economic growth. Substantial scientific research from both U.S. and foreign countries indicates that the government expenditure multiplier is considerably less than one and quite possibly close to zero. This means that if an economy starts with real GDP of $14.3 trillion (i.e. the level for 2009), and it is shocked by a surge in deficit spending, such as has been the case in the U.S., GDP will grow, but the economy will then eventually return to essentially where it began. However, the deficit spending shock leaves the economy in a more precarious overall condition because the same sized economy must now support a higher level of debt. Additionally, the private sector's share, which was 79.4% in 2009, will be reduced in favor of a larger governmental share, which was 20.6% in 2009.

This situation is graphically illustrated in Chart 2. The U.S. economy is depicted in a pie chart that expands initially (arrow A, Chart 2) in response to the deficit spending but then as resources are transferred from the private to the government sector, the economy ends where it started (arrow B, Chart 2). However, the government share of economic activity will be greater than the 20.6% share where it started (arrow C, Chart 2). The Office of Management and Budget (OMB) projects that the ratio of government debt to GDP will jump from 53% currently to 77.2% in 2020 (Chart 3). Based on this substantially elevated level of debt, the government share of total GDP could exceed 25% of GDP within five years followed by even higher levels thereafter, a dramatic difference from the share in 2009. The government share of GDP has been moving higher since the 2001 recession as the Government/Debt to GDP ratio has advanced (Chart 2). At the same time that the government share of GDP has risen, the private sector share of GDP has fallen. This period of extreme underperformance of the private sector since 2001 combined with higher relative levels of government debt constitutes a clear sign that the U.S. is following the path toward economic stagnation and a lower standard of living.

Going forward, the diminished private sector must generate the resources (i.e. the funds) to service and/ or repay the increased level of debt. If the private sector is not successful in generating the additional resources needed, the government sector must either go deeper into debt or impose additional taxes on the already stressed private sector. Considerable evidence suggests that this self-defeating process has already resulted in transfers of resources from the private sector to the government sector (Chart 4). In the past four quarters, total debt has dropped by a record $789 billion even though federal debt has surged by an outsized $1.45 trillion. The reconciling factor was a record $2.235 trillion contraction in private debt outstanding.

Higher Taxes

Second, the other side of fiscal policy – taxes – also poses another major obstacle to a return to sustained economic growth. The scientific work indicates that the government tax multiplier has a negative impact on economic growth. Academicians estimate that the drag on the overall economy from a $1 increase in taxes is between $1 to $3 over time. Thus the multiplier is -1 to -3. According to the administration's figures, the sunsetting tax cuts of 2001 and 2003 will result in a $1.5 trillion increase in taxes over the ten year period beginning in January 2011. Some have estimated that the health care reform legislation will raise taxes another $0.5 trillion, while adding to the budget deficit at the same time. Using a mid-range tax multiplier of -2, the contractionary force on the U.S. economy over the upcoming ten years would be $4 trillion, or approximately an average of $400 billion a year. This amount happens to be almost as much as the entire gain in GDP in the past four quarters. Clearly, a very vulnerable economy will not be able to absorb such higher taxes easily and the response may well be a renewed business contraction.

Massive Over-Indebtedness

Third, the U.S. economy remains extremely over-indebted. In the first quarter, the total debt to GDP ratio was 357%, 100 percentage points higher than in 1998. The best scholarly work indicates that the process of over indulging on debt ends badly – economic deterioration, systematic risk and in the normative case deflation. The private sector has deleveraged slightly either due to conditions imposed by the capital markets or their own choice. Nevertheless, the private sector remains massively over-leveraged.

Another aspect of the debt problem must be considered. The debt was used to acquire a large number of things that are no longer needed in the sense that they are not viable in view of current economic circumstances. Accordingly, the very reasonable risk is that individual private sector borrowers will not have the resources to make timely payments for debt service and amortization. The high debt ratio reflects vast amounts of unused factory capacity, office space, warehouses, retail space, and other facilities.

The seen and shadow supply of vacant homes is not only large, but also probably unknowable. After two costly home buyer tax credits, the housing industry is no healthier now than it was before the additional deficit spending was incurred. The homebuyer tax credit produced the same outcome as the cash for clunkers program, which added to the deficit without providing a sustained lift to vehicle sales. These individual programs, regardless of whether one thinks they were meritorious or not, are still constrained by the very great likelihood that the government expenditure multiplier is close to zero.

This long list of excess capacity serves to undermine the demand for labor. The U.S. must work through this redundant capital stock before longer working hours will be made available to the existing work force. Even more time will be needed before longer working hours lead to increasing demand for new hires.

It is estimated that 125,000 new hires per month are required to provide jobs for our growing labor force. If the economy is to re-employ the 8 million plus individuals thrown out of work over the past year and a half, another 240,000 new jobs per month will be required. If we are to reach full employment status over the next three years our monthly payroll gains should be about 365,000 per month. This prospect seems quite unlikely.

An Impotent Fed

Fourth, monetary policy is not working in spite of the widespread contention that the Fed is wildly printing money. The line of reasoning by many observers is that the Fed's actions will soon lead to faster economic activity but with rapid inflation. The rationale seems to rely on the work of Nobel Laureate Milton Friedman, the world's leading researcher on money and its role in the determination of economic activity, inflation, interest rates and employment. Friedman's transition mechanism from money to either inflation or deflation appears to be poorly understood by those who assume that increases in the Federal Reserve's balance sheet are tantamount to inflation. To understand the fallacy of these arguments, first consider what constitutes money.

Money and Its Functions

Money can mean different things to different people and therefore defies a simple, rigid definition. But, Friedman and other leading scholars generally do agree that money, by definition, should be widely, if not completely, acceptable in exchange for all goods and services or paying off debts. Thus, money is valued because it can, with ease, be passed on to others without dispute that proper value is received. To understand Friedman's interpretation of money and its role, it is best to read Monetary Statistics of the United States: Estimates, Sources, Methods, (Columbia University Press for the National Bureau of Economic Research (NBER), 1970).Money has three principal functions: a medium of exchange, a unit of account or standard of value and a store of value. First, money can be a tangible item, such as a dollar bill, that is accepted as payment for other tangible items or for services rendered. In this way, it serves as a medium of exchange in transactions. When an asset serves as a medium of exchange, it is completely liquid, as when the dollar bill is exchanged, without delays, for a hamburger.

Second, money can also serve as a unit of account or standard of value, in that it can be fashioned to define very precisely the value of particular goods or services. For example, U.S. gross domestic product (GDP) is reported in dollars, just as firms report their sales and profits.

Third, money can serve as a store for future use. According to Friedman, money, in this capacity, serves as "a temporary abode of purchasing power." You may store your wealth in a variety of places. Although gold coins were once used, gold is so illiquid that it is not even considered to be a form of near money--though it is still widely thought of as a store of value. Since its price can fluctuate widely and unpredictably, it no longer serves well as a medium of exchange or as a unit of account. Also, storage, insurance and conversion costs for gold may arise.

The Monetary Base is Not Money

The monetary base, bank reserves plus currency, does not fulfill these functions and hence does not constitute money. To paraphrase Friedman and Schwartz, the base, which is also known as highpowered money (currency in the hands of the public and assets of banks held in the form of vault cash or deposits at Federal Reserve Banks) cannot meet these criteria. The nonbank public – nonfinancial corporations, state and local governments and households - cannot use deposits at the Federal Reserve Bank to effectuate transactions. Moreover, currency is not sufficiently broad to be considered a temporary abode of purchasing power. For Friedman, high-powered money can be properly regarded as assets of some individuals and liabilities of none. So, let us be clear on this subject. In 2008, when the fed purchased all manner of securities, to the tune of about $1.2 trillion, the fed was not "printing money". Bank deposits at the fed exploded to the upside, the monetary base rose from $800 billion to $2.1 trillion, yet no money was "printed". Deposits did not rise, loans were not made, income was not lifted, and output did not surge. The fed could further "quantative ease" and purchase another $1 trillion in securities and lift the monetary base by a similar amount yet money would still not be "printed". It is obvious the fed authorities would like to see money, income, and output rise, but they cannot control private sector borrowing. If banks were forced to recognize bad loans and get the depreciated assets into stronger more liquid hands, it could be debated on how much reserves should be in the banking system. Until that cleansing process is completed it will be a slow grind to cure the one factor which makes the fed "impotent" and unable to "print money"....overindebtedness.Friedman and Schwartz give very specific definitions of money, definitions that are consistent with the way that M1 and M2 are currently tabulated by the Board of Governors of the Federal Reserve. The Federal Reserve calls the stock of money represented mainly by currency and checkable deposits M1.

M1 is the narrowest measure of the money supply, including only money that can be spent directly. Broader measures of money include not only all of the spendable balances in M1 but certain additional assets termed near monies. Near monies cannot be spent as readily as currency or checking account money but they can be turned into spendable balances with very little effort or cost. Near monies include what is in savings accounts and money-market mutual funds. The broader category of money that embraces all of these other assets is called M2. M2 is M1 plus relatively liquid consumer time deposits and time deposits owned by corporations, savings and other accounts at the depository institutions, and shares of money market mutual funds held by individuals. Thus, M2 is: M1 plus very liquid near monies.

Money can encompass even more than M2, including such big-ticket savings instruments as certificates of deposit whose worth exceeds $100,000 plus certain additional money-market funds and Eurodollars. The Fed no longer publishes this broader measure of money, which was called M3. M3 was M2 plus relatively less liquid consumer and corporate time deposits, savings accounts and other such accounts at depository institutions, and money market mutual fund shares held by institutions. A working definition for M3 was: M2 plus relatively less liquid near monies. Thus, the Fed, following the standards set by Friedman and Schwartz, has established money definitions that fulfill its three functions: unit of account, transaction mechanism and a store of value. The monetary base, however, does not achieve these functions and therefore is not considered money.

Excess Money equals Inflation;

Insufficient Money equals Deflation

Building on the fallacious assumption that the monetary base constitutes money, some authors have seized on Friedman's quote that "inflation is always and everywhere a monetary phenomenon." These articles imply incorrectly that Friedman said that any increase in the quantity of money causes inflation, a proposition made even worse since Friedman actually rejected such a simple concept. According to Friedman, the inflation/deflation outcomes hinged on whether money increases are excessive or insufficient. Early in his essay entitled The Optimum Quantity of Money Friedman wrote: "The real quantity of money has important effects on the efficiency of operation of the economic mechanism ... Yet only recently has much thought been given to what the optimum quantity of money is, and more important, to how the community can be induced to hold that quantity of money. ... it turns out to be intimately related to a number of topics ...(1) the optimum behavior of the price level; the (2) the optimum rate of interest; and (3) the optimum stock of capital; and (4) the optimum structure of capital."

As this passage reveals, for Friedman, an optimum quantity of money exists. Moreover, due to repeated Federal Reserve policy error, the nominal quantity of money has intermittently fluctuated wildly, forcing the nonbank sector to realign spending with the optimum level of desired money balances. By such policy actions, the Fed accentuated the volatility of the business cycle, which is why Friedman often advocated the FOMC be replaced by a monetary rule (i.e. with money growth fixed within a narrow band).

The evidence unambiguously indicates that current growth in the quantity of money is exhibiting a strongly deficient trend. In the latest twelve months, M2 has inched ahead by just 1.7%, the slowest pace in fifteen years, less than one-third the average annual gain in M2 of the past 110 years. Although the Fed no longer calculates M3, economist John Williams does, with his numbers registering the most severe contraction since the end of World War II. Hence, Friedman's monetary analysis is consistent with deflation not inflation.

Prelude to Deflation?

With the GDP deflator up less than 1% in the past four quarters and the core CPI in a similar range, the trend in inflation remains down. The risk, if not the probability, is that deflation lies ahead. Under a neutral velocity assumption, nominal GDP might be expected to improve a mere 1.7% in the next four quarters, the same as the previous four quarter rise in M2 (Chart 5). If this were split between inflation and growth, this would result in sub 1% numbers for both real GDP and inflation. Velocity (V2), however, is more likely to fall. V2 is mean reverting, a bad sign since it has been above the mean since the early 1980s. Moreover, velocity historically has declined when the private nonbank sector is deleveraging, as is the case currently. This condition is partially the result of the heavier government absorption of the pool of available credit. Also, there is a reduced incentive to take risks in an environment of substantially higher taxes. Thus, inflation and real GDP could both post surprisingly meager readings.Long term Treasury bond and zero coupon bonds will perform well in this environment. Collapsing inflationary expectations (or should we say rising deflationary expectations) will drive the bond yields lower; perhaps even into the range of prior historical lows. In this environment, holdings of long Treasury paper will serve not only as a safe haven but an asset whose value will appreciate significantly.

Van R. Hoisington

Lacy H. Hunt, Ph.D.

Finance Reform Bill Will Send Terrible Ripples Through Ag Community

This is what happens when politicians run amok!

Far from Wall Street, President Barack Obama's financial regulatory overhaul, which may pass Congress as early as Thursday, will leave tracks across the wide-open landscape of American industry.

Designed to fix problems that helped cause the financial crisis, the bill will touch storefront check cashiers, city governments, small manufacturers, home buyers and credit bureaus, attesting to the sweeping nature of the legislation, the broadest revamp of finance rules since the 1930s.

Here in Nebraska farm country, those in the business of bringing beef from hoof to mouth are anxious, specifically about the bill's provisions that tighten rules governing derivatives. Some worry the coming curbs will make it riskier and pricier to do business. Others hope the changes bring competition that will redound to their benefit.

"Out here we like to cuss the large banking institutions because of the mortgage mess, but we also know that without them some of these markets don't work," says Mike Hoelscher, energy program manager for AgWest Commodities LLC, a Holdrege, Neb., brokerage that provides derivatives services to the farming industry.

During the financial crisis, they became notorious as American International Group Inc. and others were gutted by bad bets on derivatives linked to bad mortgages.

President Obama and other proponents say the financial overhaul will prevent the kind of reckless lending and borrowing that sank the financial system and left taxpayers with the check. They say non-financial companies are worrying unduly about the derivatives portion of the legislation. The Senate is expected to approve the financial regulatory overhaul on Thursday, sending it to the president.

The full impact won't be known for years, but in Nebraska nerves are already on edge.

Executives at Five Points Bank in Hastings think the new rules on mortgage lending will make the home-loan business less profitable. "When they create a new regulator, it really scares us," says Nate Gengenbach, vice president of commercial and agricultural lending.

Advance America Cash Advance Centers Inc. thinks the new Bureau of Consumer Financial Protection will take aim at the payday-loan business, though it's not clear what steps the agency will take. Advance America's storefront at the Skagway Mall in Grand Island charges an effective 460.08% annualized interest rate on a two-week $425 loan.

But it's the derivatives portion—the part of the bill aimed directly at Wall Street—that might end up touching most lives in rural America.

The new law requires most derivatives transactions be standardized, traded on exchanges, just like corporate stocks, and funneled through clearinghouses to protect against default.

Faced with intense lobbying, Congress partially exempted businesses that use derivatives for commercial purposes. So, farmers and co-ops probably won't face new collateral requirements, for instance—although there remains a dispute over that section of the bill. Those that trade derivatives on regulated exchanges, such as the Chicago Board of Trade, are less likely to see immediate impacts than those conducting private over-the-counter deals, which will face federal regulation for the first time. The goal is to make such deals transparent.

The question for these farmers is whether such rules will make hedging more expensive. Some say new requirements on big players will create higher costs for small players, including the cash dealers will have to put aside to enter into private derivatives transactions. Some brokers think restrictions on big-money banks and investors will drain the amount of money available to the everyday deals farmers favor.

Others predict the opposite effect, pushing money from the private market to the exchanges and creating more competition that will benefit farmers.

Uncertainty reigns in Giltner, a town of 400 residents 80 miles west of Lincoln. At first glimpse, Giltner's landscape seems featureless, a fading horizon of corn and soybeans. But its details are more subtle, including wildflowers and shaded creeks. Everywhere galvanized-steel sprinkler systems crawl across farm fields like giant stick insects.

Mr. Kreutz, an outgoing 36-year-old with a sandy crewcut and sunburned neck, gave up a career in finance and took over the 2,800-acre family farm after his father's death. As he works his fields, he checks the crop futures prices on his smart phone.

Here's how Mr. Kreutz does it: Say in early summer he sees that the price for a Chicago Board of Trade futures contract on corn for delivery later in the year is $3.56 a bushel. If he likes the price, and wants to lock it in, he calls AgWest and sells a futures contract for 5,000 bushels. The futures contract is a derivative in which the price for corn is set now for exchange in the future, though no kernels will change hands. Instead, when the contract nears expiration, Mr. Kreutz and the buyer of his contract will settle—in effect—by check.

By fall, when Mr. Kreutz is ready to deliver his crop to the local co-op, the market price might have fallen by 50 cents. He'll sell his actual corn for that lower amount. But he'll make up the difference through his financial hedge. (Mr. Kreutz buys a new futures contract at the lower price to make good on his earlier promise, making up the 50 cents.) In all, he'll have hit the price target he locked in earlier in the year, minus brokerage fees.

If the price rises during the summer, as it did during the food crisis two years ago, Mr. Kreutz has to pony up extra cash for his broker—a margin call—to maintain his positions. He recoups that by selling his actual corn at a higher price, but has to take a loss to meet the futures contract he signed earlier in the year, missing out on a windfall but ultimately meeting his target price.

Mr. Kreutz does this type of operation dozens of times a year, hedging about 70% of his 345,000-bushel corn harvest.

Such deals ripple through the local economy. When Mr. Kreutz gets a margin call from his broker, he turns to his banker, Mr. Gengenbach, for a loan to cover it. Mr. Gengenbach estimates that one quarter of his farm clients use derivatives.

"Somebody like Jim has a lot of money in his crop out here," says the 37-year-old Mr. Gengenbach. "If he can't protect that, it's not good for us."

Mr. Kreutz's brokerage, AgWest, thinks the new finance law will hurt both firm and farm. If big investors and dealers have to keep more cash on hand, there will be less liquidity in the market and therefore the cost of derivatives will increase, Mr. Hoelscher, the broker said.

A few minutes from the Kreutz family farm are the corrals of Jon Reeson's feedlot. Mr. Reeson, 43, is married to Mr. Kreutz's sister Jane. His feedlot holds as many as 1,500 steer, mostly Black Angus, which grow from 600-lb. calves into 1,300 pounders ready for slaughter.

Mr. Reeson uses derivatives to hedge both the price he pays for feed and the price he gets for selling his steer.

In April, he called AgWest and locked in a price with a futures contract for $95 per hundredweight of cattle. Since then the market price has dropped to $90. If the price stays there until October, he'll have made the right call, earning a higher price than if he'd relied on the market alone. If the price spikes higher, though, he'll miss out on potential gains.

Mr. Reeson is willing to live with that possibility in exchange for locking in a profit or a narrowed loss. Derivatives hedging helped him survive the recession of 2008-2009, when cash-strapped diners avoided steak and the price of beef plunged.

He's watching the new legislation warily and can't yet tell if it will hurt or help.

When his cattle have reached full weight, Mr. Reeson puts them on Roger and Barb Wilson's trucks for the trip to the slaughterhouse. The Wilsons have seven semi tractors and 16 trailers, and one of their biggest costs is diesel fuel to keep the fleet on the road.

In 2004, Cooperative Producers Inc., his local co-op, offered Mr. Wilson a price-protection plan for 10,000 gallons of diesel at about $2.50 a gallon, with 90 days to use it.

CPI had a choice. It could take its chances and hope the price of fuel would drop before Mr. Wilson took delivery on his full order, a windfall for the co-op. If diesel prices jumped, though, the coop would take a bath. "That falls under speculation," says Gary Brandt, CPI's vice president of energy. "But that's not what cooperatives do. That's what Goldman Sachs does."

Instead, CPI hedged on the New York Mercantile Exchange, buying a futures contract on heating oil, a close market substitute for diesel fuel. The co-op goes a step further and hedges also the difference between the prices of fuel traded in New York and delivered in Nebraska.

For the 57-year-old Mr. Wilson, the pricing plan proved a mixed blessing. The first year, the pump price shot up by another 20 to 25 cents, meaning he was getting a good deal. The following year the pump price dropped about a quarter a gallon, but Mr. Wilson was obliged to pay the higher price. "It hurt to have to pay for that fuel," he recalls sourly. He quit the program after that.

The finance law's imminence has prompted CPI's Mr. Brandt to warn his sales team and customers that the co-op may have to end its maximum-price fuel contracts. He's worried too that CPI might have to cut its fuel supplies if it can't hedge against price drops.

"We have to start making a game plan if they take away the ability for us to hedge that inventory," Mr. Brandt says.

The Wilsons deliver Mr. Reeson's steer to a low, cement-gray complex on the edge of Grand Island, Neb., where trucks arrive loaded with cattle, and others leave loaded with meat. Over the past year, Mr. Reeson has sold 1,125 steer to the packing plant, which is owned by JBS USA, a Greeley, Colo., unit of Brazilian-owned JBS SA.

JBS buys livestock two ways. Sometimes it pays cash for the following week's kill. Sometimes it buys further forward, agreeing in July, for instance, to a fixed price for steer delivered in December. JBS hedges on the derivatives market to make sure live cattle prices don't drop before it takes delivery.

The company also sells beef cuts forward to restaurant chains, promising delivery at set prices months ahead of time. JBS expects to have enough meat to fulfill the agreements. But if it runs short, it doesn't want to risk having to pay higher prices to buy meat to supply those restaurants.

So, it uses the derivatives market to play it safe. To do so, the company has to find a way to hedge different cuts of beef: Tenderloins might represent 1.5% of the total value of a steer. Strip loins might make up 3%. In a sense, JBS protects itself by reconstructing the steer through a derivatives trade on the Chicago Mercantile Exchange. "We try to put the carcass back together financially," says company spokesman Chandler Keys.

The company hedges electricity for its refrigerators and natural gas for its boilers. It hedges currencies to stabilize its income from overseas. It hedges fuel for its fleet of thousands of trucks.

Even executives at a big firm such as JBS haven't been able to nail down the precise impact of the legislation on their business, introducing an unaccustomed level of uncertainty into their operations. They aren't changing the way they use derivatives, yet, hoping instead that exemptions for commercial users will insulate them.

"To get food, particularly highly perishable food like meat and poultry, through to the consumer, you have to manage your risk," says Mr. Keys.

Derivatives Defined

from WSJ:

Derivatives are financial instruments whose value "derives" from something else, such as interest rates or heating-oil prices. The first derivatives were crop futures, which appeared in the U.S. at the end of the Civil War and became a standard facet of business for companies across America.

Retail Sales Decline Modestly, More Than Forecast

The weakness shows again! Two months in a row! Ouch!

Even this figure is probably inflated for three reasons:

- Sales tax revenues are still declining. If retail sales were improving, sales tax revenues should be rising. They're not!

- The survey is skewed toward businesses that have survived. What about all those businesses that didn't? The sales of other companies have parasitized those that have gone belly up. If those businesses had been counted, sales figures would have been considerably lower.

- States have increased their sales tax. If revenues are falling even in the face off higher rates, then retail sales are really improving, are they?

from WSJ:

U.S. retail sales tumbled a second straight time in June, falling more than expected in a sign consumer spending is slowing and draining steam from an economy saddled with high joblessness.

Sales decreased 0.5%, the Commerce Department said Wednesday. Economists surveyed by Dow Jones Newswires had forecast a 0.3% decline.

Tuesday, July 13, 2010

Fed "Trading Assets" May Be Cause of Recent Stock Market Bounce

It seems everyone is perplexed by the most recent irrational bout of July market action. Like clockwork, once July rolls in, the market surges, no questions asked. This year, the ramp is particularly blatant because as the attached chart demonstrates, bonds, which are a far more credible barometer of market (in)sanity, indicate the S&P is rich by at about 50 points. As this spread will most certainly converge eventually as we discussed previously, a short stock, short bond position would generate some much needed P&L in this world of deranged fractal algorithms. As to what may have caused the most recent bout of irrational exuberance, David Rosenberg has the most logical, and generic solution: excess liquidity and a short covering spree, and "nothing fundamental here."

From Breakfast with Dave

WHAT’S DRIVING THE MARKET?

We’ve been asked repeatedly how the stock market has managed to bounce off the nearby lows with such veracity. Especially with the ongoing weakness we have seen in the incoming U.S. economic data due to the fact that the retail investor still refuses to participate and is solely focused on income-generating strategies. The answer is that the market may have been on the receiving end of another few jolts of liquidity. M2 money supply has expanded $38.5 million in the past two weeks and the M1 money multiple has risen from 0.839 to 0.862.

When we go to the weekly data from the Fed, we see that “trading assets” on commercial bank balance sheets expanded to $325 billion in the past two weeks from $297 billion. And, when we go to the Commitment of Traders report, we see that there has been a big swing in the net speculation position on the S&P 500 “E-minis” on the Mercantile Exchange (futures and options) to a net long position of 28,172 contracts from 15,155 net shorts just two weeks ago. That’s a big part of the bounce-back — prop traders and short-coverings. Nothing fundamental here, as far as we can see.

JUST CALL IT A WHOLE LOT OF VOLATILITY

- Last week’s 5.4% increase was the best performance since mid-July 2009 (week of July 17th). But yet, prior to last week, the S&P 500 saw the largest decline (-5% during the week of July 2nd) in eight weeks, and it was down two-weeks to boot (July 2nd and June 25th weeks).

- Last week also saw three days of positive performance, a streak we last saw in mid-April of this year. However, prior to those three positive sessions, the S&P 500 was down five trading days in a row.

- Last week’s increase also comes in the heels of declines in June and May, which was the worst back-to-back decline since January and February 2009

- In Q2, we saw the worst quarter (-12%) since Q4 2008 and before that, Q3 2002. In fact, going back to 1946, a decline in the quarter of 12% or more is only a 1 in 20 event (we have only seen 12 quarters of 12%+ declines in the past 64 years).

- For the first half of the year, we have seen three up months (February, March, April) and three down months (January, May, June).

- The 80% increase in the stock market that we saw from March 2009 to April 2010 is the largest increase in such a short period of time since the period of May 1935 to April 1936.

Baltic Dry Index Continues Plunge to 33 Days

The CSX earnings surge can be easily explained now that the rail company has cornered the China-US transportation corridor (what's that, it's an ocean? that's ok - the president will enact a law changing that). Because goods transit sure isn't using the dry bulk shipping sector, where the Baltic Dry has plumbed to a fresh 14 month low, continuing its longest drop in 9 years, down for a 33rd sequential day to 1,790 from 1,840. Don't look for any record numbers out of the China Customs agency or the US trade deficit in the next month.

Gordon Long: Stage I Is Over, Tipping Point Is Here

Both came to an end at the same time: the administration’s policy to Extend & Pretend has run out of time as has the patience of the US electorate with the government’s Keynesian economic policy responses. Desperate last gasp attempts are to be fully expected, but any chance of success is rapidly diminishing.

Whether an unimpressed and insufficiently loyal army general, a fleeing cabinet budget chief or G20 peers going the austerity route, all are non-confidence votes for the Obama administration’s present policies. A day after the courts slapped down President Obama’s six month gulf drilling moratorium, the markets were unpatriotically signaling a classic head and shoulders topping pattern. With an employment rebound still a non-starter, President Obama as expected was found to be asking for yet another $50B in unemployment extensions and state budget assistance to avoid teacher layoffs. However, the gig is up: the policy of Extend and Pretend has no time left on the shot clock nor for another round of unemployment benefit extensions. A congress that is now clearly frightened of what it sees looming in the fall midterm elections is running for cover on any further spending initiatives. The US electorate has been sending an unmistakable message in all elections nationwide.

The housing market is rolling over as fully expected and predicted by almost everyone except the White House and its lap-dog press corp. Noted analyst Meredith Whitney says a double dip in housing is a ‘no brainer’ with the government’s HAMP program clearly a bust as one third of participants are now dropping out. The leading economic indicator (ECRI) has abruptly turned lower, signaling the economy is slowing rapidly without the $1T per month stimulus addiction, which has kept the extend and pretend economy on life support.

The gulf oil spill that was initially stated as 1000 barrels per day has been revised upwards faster than the oil can reach the surface. It now appears to be north of 100,000 barrels per day. A 100 percent miss is about in line with the miss on how many jobs the American Recovery and Reinvestment Act of 2009 (ARRA) was going to create. Also, it appears the administration can’t even get its hands around the basics of administration management during any crisis event. Teleprompter politics doesn’t work when real problems must be resolved. There is no credibility left for Extend & Pretend nor for this president and his congressional majority.

In foreign policy the Chinese decided to ‘unpeg’ the Yuan from the US dollar, days prior to the G20 summit in Toronto, taking the wind out of the US administration’s attack plan. Congress had been expectantly raising the rhetoric levels and making the Chinese Yuan the culprit. The market sold off hard the day the Chinese made the announcement, which tells you all you need to know about this administration’s understanding and abilities to formulate effective foreign and domestic public policy.

White House policies are unmistakably in shambles. We are rudderless with terribly outdated Keynesian zealots at the helm as the storm continues to worsen. Stage I of Extend & Pretend is over – RIP!

REPORT CARD: AMERICAN RECOVERY & REINVESTMENT ACT OF 2009 (ARRA)

Before we can identify what needs to be done, what the administration is likely to do and how we can preserve and protect our wealth through it, we need to first determine where we are going wrong. Surprisingly, no one has assessed the results of the American Recovery & Reinvestment Act 2009 (ARRA) which was this administration’s cornerstone program to place the US back on the post financial crisis road to recovery. Let’s briefly review it.

EMPLOYMENT

The chart above was one of the central charts used in persuading the public that the ARRA was absolutely necessary. This chart assisted in convincing the public that something they would previously have never accepted was the required course of action. I tried to find this chart on the ARRA’s touted Recovery.gov web site and found that it has disappeared, including the links to the original discussion papers. Is it any wonder? It was like a school child telling his parents the dog ate his report card. Fortunately, I had a copy in my database.

Click to Enlarge

It isn’t just the failure to achieve the zero line in the second chart above that should be frightening. The failure to achieve the required 150K to 200K level which adds the new entrants from college, immigration, military personnel returning to civilian work force etc. indicates we are still in seriously rough waters. The falling Civilian Employment rate below is the correct way to assess the ARRA’s results.

GRADE FOR EMPLOYMENT: FAILURE E-

ECRI

As analyst David Rosenberg at Gluskin-Scheff reports:

“the ECRI index moved closer to fully discounting a recession. The spot index fell 0.6% in the June 25th week to 122.2 – the lowest level since the week of July 29th of last year when the S&P 500 was 975, so please, do not tell us that 1,000+ is still somehow a “cheap” level. The growth rate in the ECRI index dropped further, to -7.7% from -6.9% on June 18th and -5.8% on June 11th – this was the eighth week in a row of deterioration. It may end up being different this time, but never before has a -7.7% print sent off a “head fake”. In fact, the only two false signals occurred at levels that were not as negative as what we have on our hands today: the -4.5% print in 1998 after the LTCM debacle and -6.8% in the aftermath of the crash of ’87.”

GRADE FOR ECONOMIC REBOUND: MARGINAL D+

We can safely conclude either:

- 1- The administration completely under estimated the extent of the economic crisis, even though we were well into it when the ARRA was introduced.

- 2- The administration was unable to secure the actually required stimulus amount which was likely 4-5 times that approved.

- 3- The administration failed to implement the program in a timely manner.

- 4- The administration failed to diagnose the problem correctly and that in fact it is a structural problem versus a cyclical and liquidity problem, as they still insist it to be.

I personally believe it is all four of the above.

OVERALL GRADE: FAILED E

PUBLIC POLICY CHOICES

The recent G20 meeting in Toronto may very well have been a historical cusp. For the first time at a major summit the leaders refused en mass to follow US leadership. G20 leaders chose ‘austerity’, while the US firmly advocated ‘stimulus spending’.

The politically crafted joint release outlined ‘austerity, once the recovery was in place’. How this will be determined is conspicuously missing, and to me it says no agreement was reached.

Ironically, political pressures from a disgruntled electorate in the US indicates further stimulus spending is not likely to fly, while in Europe the austerity cuts are threatening the very fabric of the European social net which the public has begun rioting against. We have both conflicting approaches between G20 camps while in turn they have conflicts with their own electorate base. Maybe we should give Obama to the Europeans and we take Cameron or Merkel?

This is absolutely not the time for a failure to reach a fully agreed to and globally coordinated policy initiative that will arrest the current financial malaise. The lack of a clear understanding of what will work, what needs to be done and how it is to be done with an agreement amongst country leaders does not bode well for a successful outcome.

We must conclude that the first post-globalization crisis has been met with a resounding failure of coordination. Similarly, this was also the earmark of the political wrangling during the early stages of the 1930’s Great Depression.

ELECTORATE WON’T ACCEPT MORE SPENDING – AUSTERITY “IS IN”

Keynesianism has failed! Somewhat unknowingly there is a sense growing that these are not cyclical problems but rather are in fact structural problems - a belief that the financial crisis was not an unexpected event but rather a product of deeper and serious underlying strategic problems. President Obama and his Economic team remain in a shrinking camp of zealots who believe that further stimulus spending is still required. There is an overwhelming shift towards austerity which was evident by the recent G20 summit with one lone exception – the US.

When the Bank of International Settlements (BIS), ECB President Jean Claude Trichet and even former Democratic cabinet faithful Robert Reich come out publically strongly advocating austerity, you know opinion has changed. The last spike however had to have been when Mr. Bubbles himself, former Fed Chairman Alan Greenspan, wrote in a June 18th Wall Street Op-Ed piece.

“OUR ECONOMY CAN NOT AFFORD A MAJOR MISTAKE IN UNDERSTANDING THE CORROSIVE MOMENTUM OF THIS FISCAL CRISIS. OUR POLICY FOCUS THEREFORE MUST ERR SIGNIFICANTLY ON THE SIDE OF RESTRAINT.

Alan Greenspan, former Chairman , Federal Reserve

Wall Street Journal 06-18-10

As the primary architect of stimulus and easy money to fight everything that even remotely smelled of a slow down or problem from the 1997 Asian Crisis, Y2K, the Tech Bubble through to 911 it is an amazing turnaround and of significance from Alan Greenspan to go so publically on the record. For former followers of ‘Green-Speak’ it is unusually crystal clear!

Even CNBC recently had troubles corralling the lone voice of sanity amongst its cadre of empty headed parrots when Rick Santelli in an off CNBC private interview on an Eric King interview was heard saying:

On Spending Cuts: "Listeners, this is going to be the most important thing I am going to say: we need to maintain the focus on spending, the politicians in my lifetime always spend. If we end up spending way more than we can take in, in essence the deficit panel becomes a tax panel. We must stop spending before we talk about VAT taxes or taxing Americans more, we need to get spending under control. The ratings of congress are the lowest they have been in history”.

On Austerity: "Nobody wants that. But there is a silver lining - the UK have conditions in their economy worse than the US, but they came up with an austerity plan, and we see that their currency has been rewarded. The GDP has risen about 10% in a very short period of time."