Overview

CME Group and Dow Jones Indexes have created a new currency index and corresponding futures contract.

Launched July 26, 2010, Dow Jones CME FX$INDEX futures offer targeted risk management against a basket of major world currencies, all in a single contract. The contract focuses on the most frequently traded CME FX futures: the Euro FX, Japanese yen, British pound, Swiss franc, Canadian dollar and Australian dollar contracts, all traded against the U.S. dollar. The basket is weighted to reflect world trade but also refined to allow more precise hedging.

The index is quoted in U.S. dollars per foreign currency unit, in an inverse relationship. When the U.S. dollar strengthens against the basket of currencies, the Dow Jones CME FX$INDEX goes down, reflecting the relatively lower values of the currencies in the basket. When the dollar weakens against the basket of currencies, the Dow Jones CME FX$INDEX goes up, reflecting the higher values of the currency basket.

Dow Jones CME FX$INDEX Futures Weights

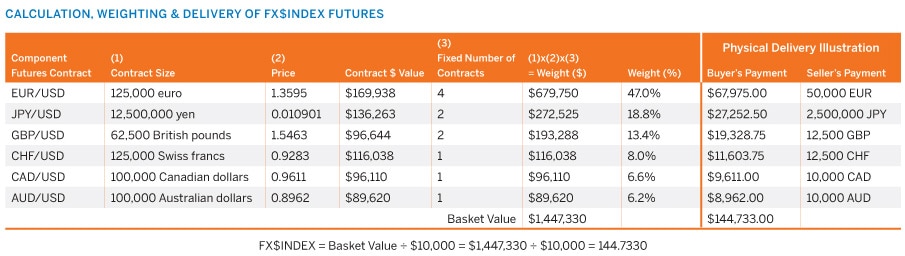

Specifically, 10 Dow Jones CME FX$INDEX futures reflect a basket of the following numbers of contracts:

4 EuroFX

2 Japanese yen

2 British pound

1 Swiss franc

1 Canadian dollar

1 Australian dollar

This Index is calculated as the basket value divided by $10,000. The numbers of contracts comprising the currency weights are fixed – they do not change.

A Well-Designed Index

Market participants have long shown interest in trading baskets of currencies against the U.S. dollar as a means of risk management. The U.S. dollar still remains the dominant currency for financial transactions, despite inroads by other currencies in recent decades, and this type of financial instrument can be a useful tool.

Other dollar index futures have been developed, usually based on factors such as competitiveness of U.S. goods on foreign markets. But these contracts lack the efficiency of the new Dow Jones CME FX$INDEX, as they were either pegged to a historic rather than a current marker, or needed to be hedged with odd numbers of futures contracts to balance or lay off risks.

Our new Dow Jones CME FX$INDEX is weighted by currency to reflect current economic realities as indicated by the Fed’s data on world trade. The futures contracts are designed to ensure that institutional traders, hedgers and market participants trading Dow Jones CME FX$INDEX futures can more precisely and conveniently lay-off risk against a basket of highly liquid CME FX futures contracts. Plus when integrated into a complete portfolio of CME FX futures and options, Dow Jones CME FX$INDEX futures allow for margin synergies with underlying products.

Benefits of Dow Jones CME FX$INDEX Futures

- More precise, convenient lay off of global FX market risk with a single index contract

- Access to over $100 billion in daily FX liquidity

- The safety and security of CME Clearing – more than 100 years without a default

- Transparent market pricing

- Electronic access around the world, around the clock on CME Globex

- Comprehensive portfolio management with CME FX Products

Physically delivered – “Hedgeable” Dow Jones CME FX$INDEX futures are satisfied through the physical delivery of 50,000 Euros; 2,500,000 Japanese yen; 12,500 British pounds; 12,500 Swiss francs; 10,000 Canadian dollars; and, 10,000 Australian dollars. The final settlement price is based on settlements in the six component currency futures. This provides institutional traders, hedgers and market participants with a more precise hedge than with previous U.S. dollar-based indexes, by matching 10 Dow Jones CME FX$INDEX futures vs. 4 EuroFX, 2 Japanese yen, 2 British pound, 1 Swiss franc, 1 Canadian dollar and 1 Australian dollar futures. Traders in “Hedgeable” Dow Jones CME FX$INDEX futures benefit from the liquidity of current CME FX futures, in turn offering a tighter market for our customers.

Enlarge