Popular Delusions

Memo to Central Banks: You’re debasing more than our currency

By Dylan Grice, Societe Generale

At its most fundamental level, economic activity is no more

than an exchange between strangers. It depends, therefore, on a degree

of trust between strangers. Since money is the agent of exchange, it is

the agent of trust. Debasing money therefore debases trust. History is

replete with Great Disorders in which social cohesion has been

undermined by currency debasements. The multi-decade credit inflation

can now be seen to have had similarly corrosive effects. Yet central

banks continue down the same route. The writing is on the wall. Further

debasement of money will cause further debasement of society. I fear a

Great Disorder.

I am more worried than I have ever been about the clouds

gathering today (which may be the most wonderful contrary indicator you

could hope for...). I hope they pass without breaking, but I fear the

defining feature of coming decades will be a Great Disorder of the sort

which has defined past epochs and scarred whole generations.

“Next to language, money is the most important medium through which modern societies communicate” writes Bernd Widdig in his masterful analysis of Germany’s inflation crisis

“Culture and Inflation in Weimar Germany.”

His may be an abstract observation, but it has the commendable merit of

being true … all economic activity requires the cooperation of

strangers and therefore, a degree of trust between cooperating

strangers. Since money is the agent of such mutual trust, debasing money

implies debasing the trust upon which social cohesion rests.

So I keep wondering to myself, do our money-printing central banks and their cheerleaders understand the

full

consequences of the monetary debasement they continue to engineer?

Inflation of the CPI might be a consequence both seen and measurable. A

broad inflation of asset prices might be a consequence seen, though not

measurable. But what about the consequences that are unseen but

unmeasurable – and are all the more destructive for it? I feel queasy

about the enthusiasm with which our wise economists play games with

something about which we have such a poor understanding.

If you take a look around you, any artefact you see will only

be there thanks to the cooperative behaviour of lots of people you don’t

know. You will probably never know them, nor they you. The screen you

watch on your terminal, the content you read, the orders which make the

prices flicker … the coffee you drink, the cup you hold, the bin you

throw it in afterwards … all your clothes, all your accessories, all

the buildings you’ve been in, all the cars … you get the idea.

Without exception

everything you own, everything you want to own, everything you need,

and everything you think you need embodies the different skills and

talents of a mind-boggling number of complete strangers. In a very real

sense we constantly trust in strangers to a degree, as strangers trust

us. Such cooperative activity is to everyone’s great benefit and I find

it is a marvellous thing to behold.

The value strangers put on each other’s contributions manifests

itself in prices, and prices require money. So it is through money that

we express the extent of our appreciation for the many different

talents embedded in each thing we consume, and through money that our

skills are in turn valued by others. Money, in other words, is the agent

of this anonymous exchange, and therefore money is also the agent of

the hidden trust on which it depends. Thus, as Bernd Widdig reflects in

his book (which I urge you all to read), money …

“… is more than simply a tool for economic exchange; its

different qualities shape the way modern people think, how they make

sense of their reality, how they communicate, and ultimately how they

find their place and identity in a modern environment.”

Debasing money might be expected to have effects beyond the

merely financial domain. Of course, there are many ways to debase money.

Coin can be clipped, paper money can be printed, credit can be created

on the basis of demand deposits which aren’t there ... the effects are

ultimately the same though: the implied trust that money communicates

through society is eroded.

To see how, consider the example of money printing by

authorities. We know that such an exercise raises revenues since the

authorities now have a very real increase in purchasing power. But we

also know that revenue cannot be raised by one party without another

party paying. So who pays?

If the authorities raise taxes explicitly and openly, voters

know exactly why they have less spending power. They also know how much

less spending power they have. But if the authorities instead raise

money by simply printing it, they raise the revenue by stealth. No one

knows upon whom the burden falls. People notice only that they can’t

afford the things they used to be able to afford, or they can’t afford

the things which everyone else can afford. They know that something is

wrong, but they just don’t know what, why, or who is to blame. So

inevitably they look for someone to blame.

The dynamic is similar to that found in the well-worn plot line

in which a group of strangers are initially brought together in happier

circumstances, such as a cruise, a long train journey or a weekend

away. In the beginning, spirits are high. The strangers exchange jokes

and get to know one another as the journey begins. Then some crime is

committed. They know it must be one of them, but they don’t know who. A

great suspicion ensues. All trust between them is broken down and the

infighting begins....

So it is with monetary debasement, as Keynes understood deeply

(so deeply, in fact, that it’s ironic so many of today’s crude

Keynesians support QE so enthusiastically). In 1921 he said:

“By a continuing process of inflation, Governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily;

and, while the process impoverishes many, it actually enriches some ….

Those to whom the system brings windfalls …. become “profiteers” who are

the object of the hatred … the process of wealth-getting degenerates

into a gamble and a lottery .. Lenin was certainly right. There is no

subtler, no surer means of overturning the existing basis of society

than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.”

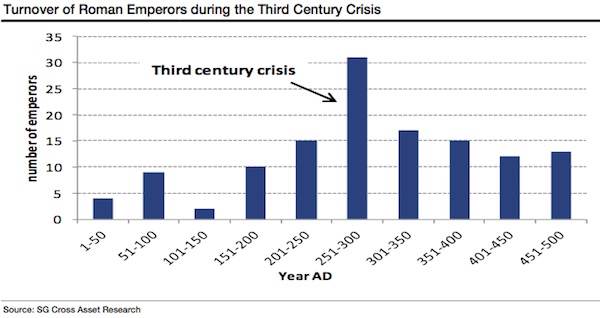

History is replete with Great Disorders in which currency

debasement has coincided with social infighting and scapegoating. I have

written in the past about the Roman inflation of the Third Century AD.

The following chart shows the rapid turnover of emperors during what is

known as the Third Century Crisis. As trade declined, crops failed and

the military suffered what must have seemed like constant defeat, it

wasn’t difficult for a successful or even popular general to convince

the rest of the empire that he’d make a better fist of governing.

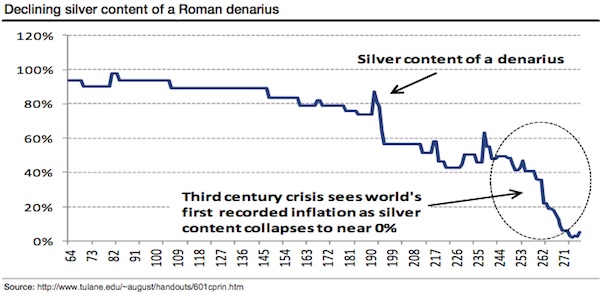

But this political turnover was accompanied by what may be

history’s first recorded instance of systematic currency debasement.

With the empire no longer expanding and barbarians being forced

westwards by the migrations of the Steppe peoples, Rome’s borders were

under threat. But the money required to fund defence wasn’t there.

Successive emperors therefore reached the same conclusions that kings,

princes, tyrants and democratically elected governments would later

reach down the ages when faced with a perceived “shortage of money”:

they created more by debasing the existing stock. In the second half of

the third century, the silver content of a denarius had shrunk to zero.

Copper coins disappeared altogether.

This debasement of currency also coincided with a debasement of

society. Factions grew more suspicious of one another. Communities

fragmented. And one part of the community bore the brunt of the fears:

Christians. While Rome had always welcomed new religions and Gods,

incorporating new foreign deities as their empire grew, Christians were

altogether different. They rejected Rome’s gods. They refused to pray to

them. They said that only their God was deserving of worship. The rest

of the Romans concluded that this obstinacy must be a source of great

anger for their own ancient Roman gods, and supposed that those gods

must now be exacting their own great punishment in return.

So the Romans turned on their Christians with a great violence

which lasted throughout the period of the currency debasement but peaked

with Diocletian’s edict of 303 AD. The edict decreed, among other

things, that Christian meeting places be destroyed, Christians holding

office be stripped of that office, Christian freedmen be made slaves

once more and all scriptures be destroyed. Diocletian’s earlier edict,

of 301 AD, sought to regulate prices and set out punishments for

‘profiteers’ whose prices deviated from those set out in the edict.

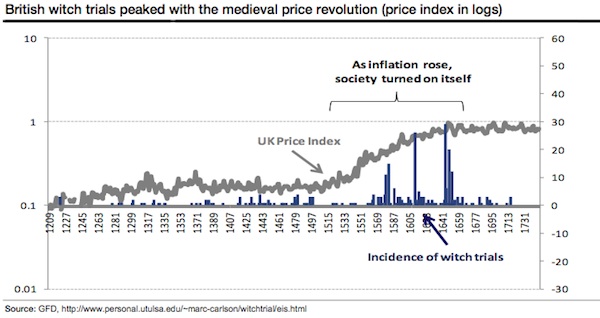

A similar dynamic seems evident during Europe’s medieval

inflations, only now, the confused and vain effort to make sense of the

enveloping turmoil saw the blame focus on suspected witches. The

following chart shows the UK price index over the period with the

incidence of witchcraft trials. Note the peak in trials coinciding with

the peak of the price revolution.

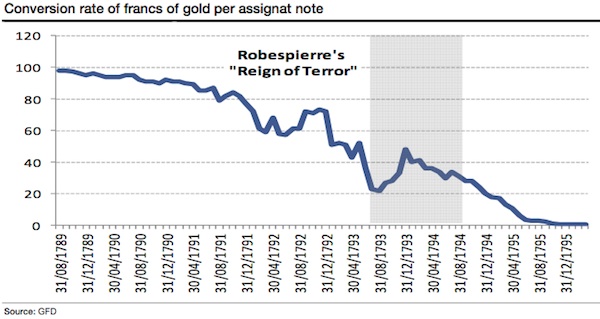

Were the same dynamics at work during the French Revolution of

1789? The narrative of Madame Guillotine and her bloody role is well

known. However, the execution of royalty by the Paris Commune didn’t

begin until 1792, and the Reign of Terror in which Robespierre’s

Orwellian sounding “Committee of Public Safety” slaughtered 17,000

nobles and counter-revolutionaries didn’t start until well into 1793. In

the words of guillotined revolutionary Georges Danton, this is when the

French revolution “ate itself”. But the coincidence of these events to

the monetary debasement is striking.

The political violence was justified in part by blaming nobles

and counter-revolutionaries for galloping inflation in food prices. It

saw ‘speculators’ banned from trading gold, and prices for firewood,

coal and grain became subject to strict controls. According to Andrew

Dickson White, author of “Fiat Money Inflation in France”, (echoing

Keynes’ remark that

“wealth-getting degenerates into a gamble and a lottery”) “economic calculation gave way to feverish speculation across the country.”

However, the most tragic of all the inflations in my opinion,

and certainly the starkest example of a society turning on itself was

the German hyperinflation. Its causes are well known. Morally and

financially bankrupt by the First World War, the reparation demands of

the Allies (which Keynes argued vociferously against) followed by the

French occupation of the Ruhr served to humiliate a once-mighty nation,

already on its knees.

And it really was on its knees. Germany simply had no way to

pay. The revolution following the flight of the Kaiser was incomplete.

Concern was widespread that Germany would follow the path blazed by

Moscow’s Bolsheviks only a year earlier. A

de facto civil war

was being fought on the streets of major cities between extremist mobs

of the left and right. Six million veterans newly demobilized,

demoralized, dazed and without work were unable to support their

families ... the great political need was to pay off the “internal

debts” of pensions, life insurance and welfare support in any way

possible. The risk of printing whatever was required was well

understood. Bernhard Dernberg, vice chancellor in 1919, found himself

overwhelmed with promises to pay for the war disabled, food subsidies,

unemployment insurance, etc., but everyone knew where the money was

coming from:

“A decision of the National Assembly is made. On its basis,

Reich Treasury bills are printed and on the basis of the Reich Treasury

bills, notes are printed. That is our money. The result is that we have

a pure assignat economy.”

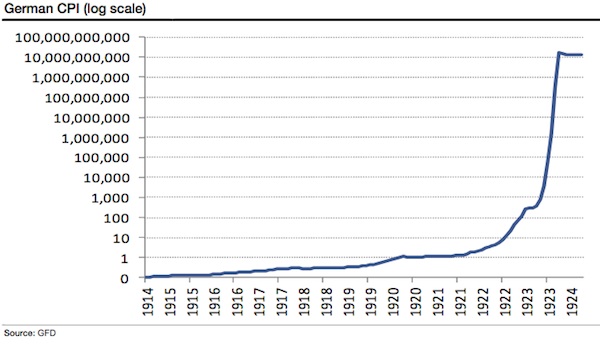

But print they did. Prices would rise by a factor of one

trillion. At the end of the war, Germany owed 154bn Reichmarks to its

creditors. By November 1923, that sum measured in 1914 purchasing power

was worth only 15 pfennigs.

It is difficult to comprehend the psychological trauma

inflicted by this episode. Inflation inverted the efficacy of correct

behaviour. It turned the ethics of thrift, frugality and notions such as

working hard today to bring benefit tomorrow completely on their heads.

Why work today when your rewards would mean nothing tomorrow? What use

thrift and saving? Why not just borrow in depreciating currency? Those

who had worked and saved all their lives, done everything correctly and

invested what they had been told was safe, were mercilessly punished for

their trust in established principles, and their inability to see the

danger coming. Those with no such faith who had seen the danger coming

had benefited handsomely.

Everything, in other words, was dependent on one’s ability to

speculate, recalling what Dickson White observed of the French

Revolution and Keynes reflections more generally. Erich Remarque is best

known for his anti-war novel

“All Quiet on the Western Front” but perhaps his best work was the “

The Black Obelisk”

set in the early Weimar period, and a penetrating meditation on the

upside-down world of inflation. The protagonist Georg poignantly

captures this speculative imperative when he sits down and lets out a

long sigh:

“Thank God that it’s Sunday tomorrow … there are no rates

of exchange for the dollar. Inflation stops for one day of the week.

That was surely not God’s intention when he created Sunday.”

Perhaps the most eloquent chronicler of the Weimar

hyperinflation was Elias Canetti, whose mother moved him from the

security of Zurich to Frankfurt in 1921 to take advantage of cheaper

living. Canetti never forgave her, and his life’s work shows what a

lasting impression the move from heaven to hell made:

“A man who has been accustomed to rely on (the monetary

value of the mark) cannot help feeling its degradation as his own. He

has identified himself with it for too long, and his confidence in it

has been like his confidence in himself … Whatever he is or was, like

the million he always wanted, he becomes nothing”

More tragic still was what German society became during the

inflation. Like other Axis countries on the wrong side of the War and

now in the grip of hyperinflation, Germany turned viciously on its Jews.

It blamed them for the surrounding evil as Romans had blamed

Christians, medieval Europeans had suspected witches, and French

revolutionaries had blamed the nobility during previous inflations. In

his classic “Crowds and Power”, Canetti attributed the horror of

National Socialism directly to a “morbid re-enaction impulse”.

“No one ever forgets a sudden depreciation of himself, for

it is too painful … The natural tendency afterwards is to find something

which is worth even less than oneself, which one can despise as one was

despised oneself. It is not enough to take over an old contempt and to

maintain it at the same level. What is wanted is a dynamic process of

humiliation Something must be treated in such a way that it becomes

worth less and less, as the unit of money did during the inflation. And

this process must be continued until its object is reduced to a state of

utter worthlessness. … In its treatment of the Jews, National Socialism

repeated the process of inflation with great precision. First they were

attacked as wicked and dangerous., as enemies; then, there not being

enough in Germany itself, those in the conquered territories were

gathered in; and finally they were treated literally as vermin, to be

destroyed with impunity by the million.

All this is very disturbing stuff, but testament to a

relationship between currency devaluation and social devaluation. Mine

is not a complete or in any way rigorous analysis, I know.

I emphasize that it’s not in any way meant as some sort of crude mapping on to today’s environment.

My point is to show that money operates in many social domains beyond

the financial, and that tying currency devaluation to social devaluation

might have some merit.

Consider some recent and less extreme currency inflations. The

1970s bear market in equities saw relatively mild inflation which was

also characterized by relatively mild but nevertheless real

factionalization of society. An ideological left vs right battle played

out between labour and capital, unions and non-unions and perhaps most

bizarrely, between

rock and disco.

As already stated, money implies a trust in the future. It implies that

today’s money can be used in the future. So in the era of punk, did the

Sex Pistols provide the most concise commentary of the malaise?

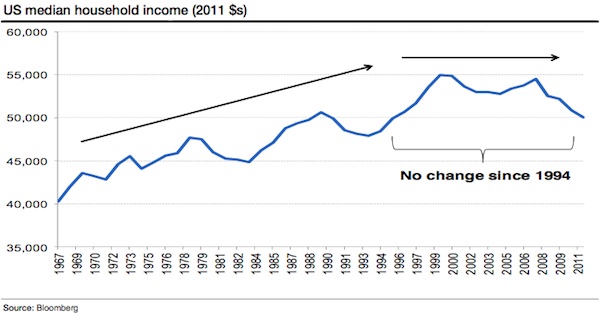

Which brings us to today. Despite the CPI inflation of the

1970s receding, our central banks have continued to play games with

money. We’ve since lived through what might be the largest credit

inflation in financial history, a credit hyperinflation. Where has it

left us? Median US household incomes have been

stagnant for the best part of twenty years (chart below)

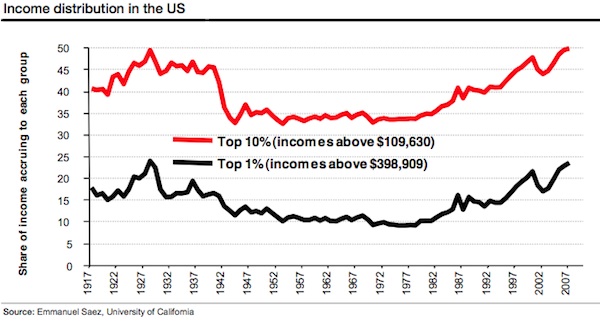

Yet inequality has surged. While a record number of Americans

are on food stamps, the top 1% of income earners are taking a larger

share of total income than since the peak of the 1920s credit inflation.

Moreover, the growth in that share has coincided almost exactly with

the more recent credit inflation.

These phenomena are inflation’s hallmarks. In the Keynes quote

above, he alludes to the “artificial and iniquitous redistribution of

wealth” inflation imposes on society without being specific. What

actually happens is that artificially created money redistributes wealth

towards those closest to it, to the detriment of those furthest away.

Richard Cantillon (writing decades before Adam Smith) was the

first to observe this effect (hence “Cantillon effect”). He showed how

those closest to the money source benefited unfairly at the expense of

others, by thinking through the effects in Spain and Portugal of the

influx of gold from the new world as follows:

“If the increase of actual money comes from mines of gold

or silver … the owner of these mines, the adventurers, the smelters,

refiners, and all the other workers will increase their expenditures in

proportion to their gains. . . . All this increase of expenditures in

meat, wine, wool, etc. diminishes of necessity the share of the other

inhabitants of the state who do not participate at first in the wealth

of the mines in question. The altercations of the market, or the demand

for meat, wine, wool, etc. being more intense than usual, will not fail

to raise their prices … Those then who will suffer from this dearness …

will be first of all the landowners, during the term of their leases,

then their domestic servants and all the workmen or fixed wage-earners

... All these must diminish their expenditure in proportion to the new

consumption …

(Quoted in Mark Thornton, “Cantillon on the Cause of the Business Cycle” Quarterly Journal of Austrian Economics Vol 9, No 3 [Fall 2006])

In other words, the beneficiaries of newly created money spend

that money and bid up the price of goods with their higher demand. Those

who suffer are those who have to pay newly higher prices but did not

benefit from the newly created money.

The credit inflation analog to the Cantillon effect has played

out perfectly in recent decades. Central banks provided cheap money to

banks, the cheap money artificially inflated asset prices, artificially

inflated asset prices made anyone connected to those assets rich as we

became a nation of speculators, those riches were achieved at everyone

else’s expense, and ‘everyone else’ has now realized what has happened

and is understandable enraged … as Keynes explained, “

Those to whom the system brings windfalls …. are the object of the hatred.

And now the social debasement is clear for all to see. The 99%

blame the 1%, the 1% blame the 47%, the private sector blames the public

sector, the public sector returns the sentiment … the young blame the

old, everyone blame the rich … yet few question the ideas behind

government or central banks ...

I’d feel a whole lot better if central banks stopped playing

games with money. But I can’t see that happening anytime soon. The ECB

has thrown the towel in, following the SNB last year in committing

effectively to print unlimited amounts of money for the greater good.

The BoE and the Fed have long since made a virtue of what was once

considered a necessity, with what was once the unconventional

conventional. As James Bullard told everyone a few weeks before the last

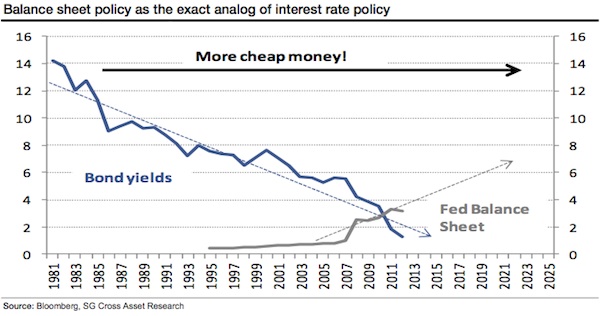

Fed meeting, lest there be any doubt:

"Markets have this idea that, there's QE1 and QE2, so QE3

must be the same as those previous ones. It's not that clear to me that

this is the way this is going … it would just be to do balance sheet

policy as the exact analogue of interest rate policy."

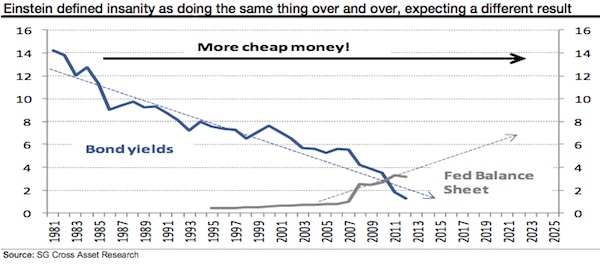

In other words, the central banks’ balance sheets are the new

policy tool. As interest rates embarked on a multi-year decline from the

1980s on, central bank balance sheets are set to embark on a multi-year

climb ...

So as Nobel Prize winning experts in economics

punch the air because inflation expectations have been rising since the policy was announced,

“It’s the whole point of the exercise” (Duh!) the BoE

admits that QE has mainly benefited the rich, but vows to continue anyway.

All I see is more of the same - more money debasement, more

unintended consequences and more social disorder. Since I worry that it

will be Great Disorder, I remain very bullish on safe havens. The next

few issues of Popular Delusions will outline some thoughts on what

exactly that means.